Worldwide Negative Ion Cyclotron Market: Strategic Outlook for 2026 — PW Consulting

PW Consulting today publishes a focused strategic briefing accompanying our full Worldwide Negative Ion Cyclotron Market report. This executive release synthesizes the report’s most actionable insights for decision-makers preparing capital, regulatory and partnership strategies in 2026. It highlights why the negative ion cyclotron space is entering a deliberate growth phase, how competitive dynamics will shape procurement and investment, and which practical tools in the full study will materially de‑risk project execution — while reserving the granular segment-level tables and transaction models for subscribers.

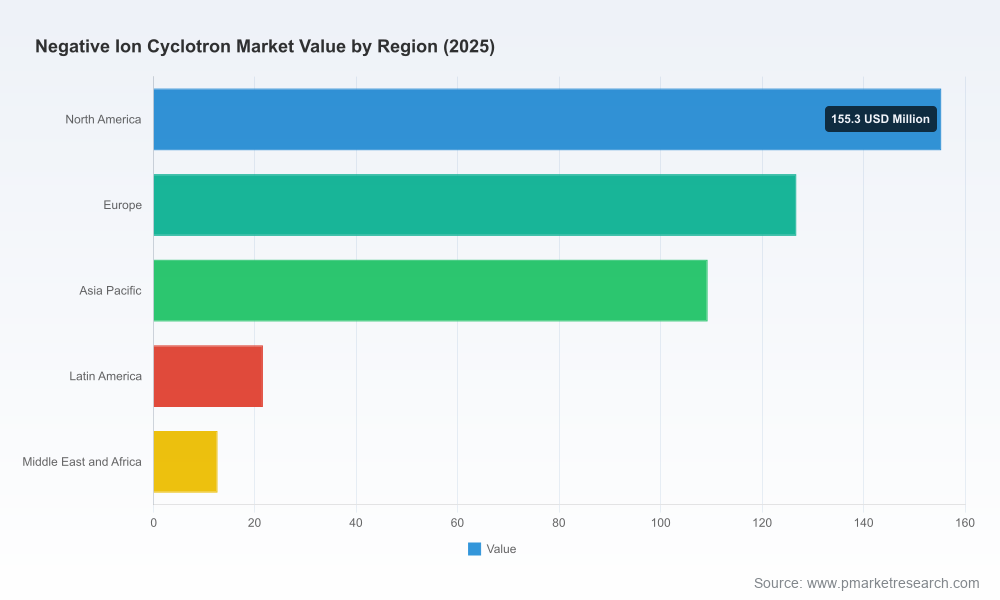

Worldwide Negative Ion Cyclotron Market

Executive snapshot

The global negative ion cyclotron market has expanded steadily through the early 2020s, moving from a low‑hundreds million base to an established mid‑hundreds million market by the 2025 base year. Our modelling projects durable expansion through the 2026–2032 forecast window at a compound annual growth rate of approximately 6.15%, reaching a materially larger market by the end of the period. The combination of medical isotope demand, investment in theranostics, and expanding PET infrastructure underpins a multi-year growth runway.

Worldwide Negative Ion Cyclotron Market

Why 2026 is a strategic inflection point

- Demand convergence: Growing clinical adoption of PET-based diagnostics and the rapid maturation of theranostic protocols are increasing demand for reliable on‑site isotope production. This drives both replacement cycles and greenfield facility projects.

- Concentrated supply base: A small set of incumbent OEMs dominate the market, creating predictable product roadmaps but also introducing supplier dependency and extended lead times for capacity additions.

- Regulatory and standardization pressure: Medical cyclotron facilities and equipment sit inside a dense compliance environment — from IAEA safety standards to EU MDR and ISO device requirements — increasing the importance of regulatory planning early in any procurement.

- Technology constraints and infrastructure demands: Key hardware limits — notably on negative H‑ ion source currents and high‑energy extraction — combined with significant RF and vacuum infrastructure requirements, raise capital intensity and operational risk for new installations.

- Export and dual‑use considerations: High‑energy systems face export licensing regimes in many jurisdictions, impacting cross‑border procurement and aftermarket supply chains.

What the PW Consulting report delivers — pragmatic, transaction‑ready content

Our goal is to translate market intelligence into executable choices. The full report is structured around practical decision points and includes:

Worldwide Negative Ion Cyclotron Market

- Transparent market sizing and scenario modelling with clear assumptions and sensitivity analyses to stress‑test investment cases under alternative demand and regulatory scenarios.

- Supplier benchmarking templates that evaluate OEMs on performance (energy bands and upgrade paths), service footprint, lead times and life‑cycle economics — enabling apples‑to‑apples commercial comparisons.

- Site feasibility and capital planning checklists covering facility design requirements (RF power, ultra‑high vacuum systems), utility provisioning, radiation protection layouts and commissioning milestones.

- Regulatory roadmap and compliance playbook aligned to IAEA SSG‑49 and major medical device frameworks (including MDR/ISO requirements), with task owners and timeline templates for approvals and validations.

- Operational readiness tools — including O&M budgeting frameworks, workforce competency matrices, and spare‑parts and consumables strategies to minimize downtime from ion source or RF failures.

- M&A and partnership scouting frameworks for acquirers and investors, including valuation drivers, integration checklists and a confidentiality‑screened shortlist of strategic targets suitable for bolt‑on acquisitions or JV structures.

- Risk matrices and mitigation plans covering supply chain disruption, export licensing delays, regulatory compliance shortfalls, and technology obsolescence.

Competitive landscape — incumbents, capabilities and recent moves

The negative ion cyclotron market is characterized by a handful of established suppliers offering product lines that span clinical PET isotope production through higher‑energy theranostic-capable systems. Key players profiled in the report include:

- Ion Beam Applications SA (IBA) (Louvain‑la‑Neuve, Belgium) — a leader with a broad Cyclone family of negative ion cyclotrons targeting both PET and therapeutic radioisotope production. IBA’s recent commercial activity underscores continued demand for higher‑energy systems for theranostic applications.

- Advanced Cyclotron Systems Inc. (ACSI) (Richmond, Canada) — focused on TR‑series cyclotrons optimized for multi‑isotope PET production and regional service expansion.

- GE Healthcare (Chicago, USA) — deploying PETtrace platform cyclotrons and leveraging its global service and clinical channel to offer integrated solutions for hospital networks.

- Sumitomo Heavy Industries (Tokyo, Japan) — supplying compact negative ion systems for clinical PET production, with deep engineering capability and long-term reliability records.

- TeamBest Global Companies (Sugar Land, USA) — positioned on affordability and rapid delivery cycles for standard clinical cyclotrons.

Recent installation and contract activity from several of these OEMs demonstrates active replacement and greenfield dynamics — with selected high‑energy orders and facility deliveries showing that demand is both regional and application‑driven. The market’s three‑ and five‑player concentration ratios indicate a materially consolidated supplier environment, and this concentration amplifies the strategic importance of supplier selection, service contracts and inventory strategies.

Key industry constraints that shape commercial choices

- Beam current limits: Commercial negative H‑ ion sources remain constrained by space‑charge and extraction physics, typically limiting reliable beam current ranges — a factor that directly affects throughput and isotope yield planning.

- Facility infrastructure: Stable negative ion acceleration requires substantial RF power and ultra‑high vacuum systems; insufficient specification at design stage is a common source of costly commissioning delays.

- Regulatory classification: In many major markets, cyclotron systems and the associated production facilities fall under medical device and radiological safety frameworks that require ISO‑aligned quality systems and premarket preparation.

- Export controls: Systems above certain energy thresholds are subject to licensing frameworks that can materially extend procurement timelines for cross‑border purchases.

Strategic implications by stakeholder

- Hospital operators & health systems: Prioritize long‑lead procurement and negotiate robust availability SLAs. Evaluate managed production or service‑contract models where capital or regulatory risk is a constraint.

- OEMs: Invest in modularity and service network expansion. Differentiation will increasingly hinge on upgradeability, shorter commissioning windows and bundled regulatory support.

- Investors & acquirers: Focus on targets with strong service footprints and complementary IP (e.g., targetry, radiochemistry) that can expand margins through vertical integration.

- Governments & regulators: Coordinate license pathways and export‑control guidance to avoid blocking clinical capacity expanders, and consider incentives to localize critical subsystems to reduce single‑source exposure.

Timing and priority roadmap for 2026 decisions

For teams planning procurement or capacity expansion in 2026, timing and sequencing matter. The full report provides a practical 12–18 month phased roadmap — high level steps are:

- Strategic needs assessment and scenario selection (use our sensitivity templates to model demand under alternative clinical adoption rates).

- Preliminary site and regulatory due diligence (early engagement with licensing bodies mitigates late-stage redesigns).

- Supplier shortlisting using our benchmarking criteria and issuing conditional POs tied to service and delivery SLAs.

- Final financing and procurement (consider hybrid models: capex purchase, lease or managed service to optimize balance-sheet usage).

- Commissioning, validation and operational ramp (align staffing, spare parts and QC workflows prior to first production runs).

Why PW Consulting’s advisory matters for 2026

Decisions in 2026 will lock in capacity and clinical capability for a decade. Our report equips leaders with the tools to: quantify demand risk, accelerate procurement without increasing contractual exposure, ensure regulatory readiness, and identify M&A and partnership targets that enhance resilience. Importantly, the study synthesizes technical constraints (from ion source physics to RF and vacuum engineering) with commercial realities (supplier concentration, export licensing), enabling a single integrated view that most engineering‑only or finance‑only studies omit.

Next steps — accessing the full intelligence

This briefing outlines the high‑level strategic thesis and the practical levers available to senior decision makers. The full Worldwide Negative Ion Cyclotron Market report contains the detailed regional and application splits, project‑level financial models, supplier scorecards and the step‑by‑step procurement playbooks that operational teams will use to execute projects. To obtain the full report, download access or request a tailored advisory workshop with our cyclotron practice team via the PW Consulting website.

For leaders evaluating procurements, partnerships or investments in 2026, the choice is simple: act early with disciplined supplier engagement and regulatory planning — or accept elongated lead times and higher execution risk. PW Consulting’s study is designed to make that early action precise and creditable.

For detailed analysis of this topic, please visit the official page:Worldwide Negative Ion Cyclotron Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com