Worldwide Headphones Without Mic Market — Strategic Outlook for 2026: Actionable Intelligence from PW Consulting

Executive Summary

PW Consulting’s new market study on the Worldwide Headphones Without Mic market (base year 2025; historical coverage 2020–2025; forecast 2026–2032) equips senior executives and strategic planners with the forward-looking intelligence required to make high‑stakes choices in 2026. The market expanded materially through the first half of the decade — rising from under USD 3.9 billion in 2020 to approximately USD 4.8 billion in 2025 — and our modelling projects continued growth at a steady compound annual growth rate (CAGR) of 4.25% through 2032. By 2032 the market is forecast to be in the neighborhood of mid‑single‑digit billions (USD), reflecting resilient demand in professional, audiophile and entertainment use cases even as wireless and integrated‑mic segments evolve.

Worldwide Headphones Without Mic Market

Why this report matters for 2026 decision-making

- Tactical timing: With a moderate, reliable growth trajectory, 2026 is a year for constructive investment—not speculative expansion. Our analysis pinpoints when to prioritize capacity upgrades, R&D reallocation, and go‑to‑market experiments versus when to adopt a wait‑and‑observe posture.

- Margin protection under cost pressure: Raw material inflation, labor cost drift and regulatory tightening are converging to compress supplier and OEM margins. The report translates these pressures into practical margin scenarios and mitigation levers executives can deploy immediately.

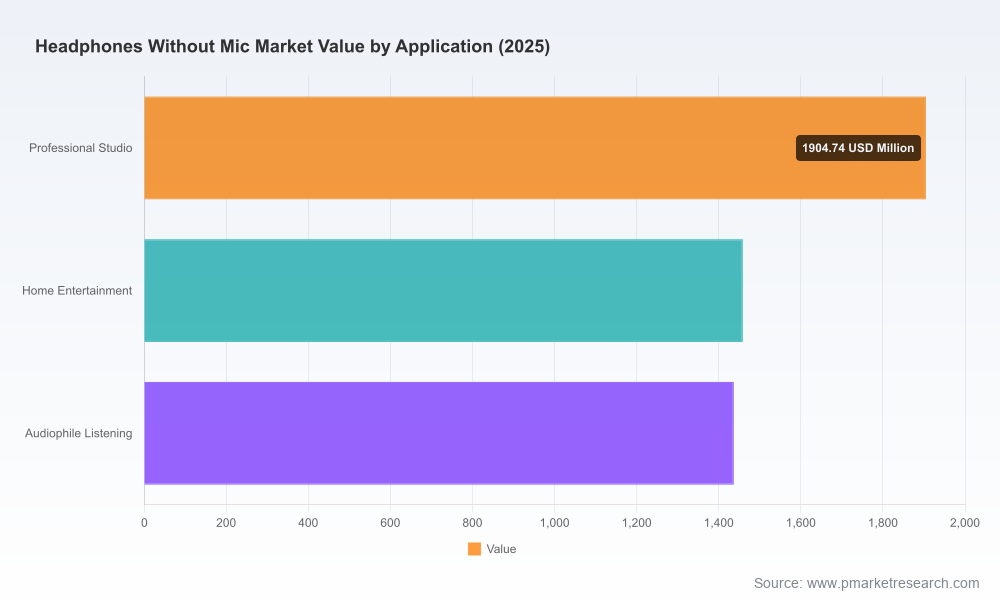

- Competitive differentiation: The non‑mic headphone category remains a domain of premium audio fidelity and pro/studio credibility. We map the competitive landscape to reveal where premiumization, niche manufacturing techniques (e.g., planar magnetic drivers), and craftsmanship deliver defensible pricing power.

What the report contains — practical, actionable components

- Market sizing and scenario forecasts: A transparent methodology that reconciles shipment, ASP and replacement cycles to produce a base case and two stress scenarios through 2032. The report provides top‑line market trajectories and sensitivity to key cost and demand drivers.

- Supply chain and cost‑stack analysis: End‑to‑end decomposition of driver costs, magnet and rare‑earth dependencies, cable assemblies and outsourced assembly labor. Each cost line is modelled with near‑term shocks and medium‑term normalization paths so procurement and finance teams can stress test margins.

- Regulatory and trade impact module: Forward‑looking analysis of RoHS updates, tariff regimes and trade friction — including practical compliance timelines and cost pass‑through scenarios for common trade flows.

- Channel and go‑to‑market playbooks: Playbooks tailored to premium retail, pro audio channel, direct‑to‑consumer and specialist distributors, with recommended promotional cadence, bundling strategies and SKU rationalization templates.

- Competitive benchmarking and opportunity map: A structured framework to assess brand equity, engineering differentiation and route‑to‑market effectiveness. The section includes a gap analysis across product attributes (e.g., driver type, tuning philosophy, materials) and highlights white‑space opportunities.

- M&A and partnership candidates: Scoring of acquisition targets and strategic partners using commercial, operational and cultural fit criteria for buyers seeking immediate scale or niche technology access.

- Implementation annexes: Procurement scorecards, sample RFP templates for driver suppliers, and an operational checklist to reduce lead time and manage high‑end driver constraints.

Market dynamics shaping near‑term strategy

Three clusters of forces will shape 2026 outcomes: (1) supply‑side cost pressure and component lead times, (2) regulatory and trade headwinds, and (3) evolving demand segmentation across professional, audiophile and home entertainment buyers. Executives who integrate these clusters into their 2026 planning horizon will secure margin resilience and selective share gains.

Worldwide Headphones Without Mic Market

Key supply‑side signals

- Raw material volatility: Prices for critical materials used in high‑performance drivers have moved upward materially, and rare‑earth processing bottlenecks have extended lead times for planar magnetic and other premium driver subcomponents. This increases the risk of shipment delays for premium SKUs and creates opportunities to renegotiate long‑term supply contracts or to vertically integrate specific driver subassemblies.

- Labour and cost dynamics: Wage inflation in established low‑cost assembly geographies has reduced the labor arbitrage that many OEMs relied on. Expect a higher overall cost floor per unit unless assembly productivity or automation investments are accelerated.

- Trade and tariff considerations: Remaining tariffs on certain import routes continue to distort landed cost calculations; procurement strategies that emphasize near‑shoring or tariff‑optimized bill‑of‑materials will materially alter cost competitiveness in 2026.

Regulatory landscape and compliance timing

Regulatory updates — especially in major markets — will affect product engineering, materials sourcing and labeling requirements. Firms that allocate engineering bandwidth to compliance early in 2026 will avoid costly rework and delayed product launches later in the year. Our report provides a compliance calendar and a prioritized list of component redesigns that yield the highest risk reduction per engineering hour.

Worldwide Headphones Without Mic Market

Competitive landscape — who matters and why

The category continues to be led by established pro‑audio and audiophile brands that combine engineering pedigree with channel credibility. These incumbents maintain strong mindshare among studio professionals and discerning listeners; at the same time, tactical new product introductions and incremental technological advances are reshaping product positioning.

- Sony Corporation (Tokyo): Maintains a dual strategy of heritage pro audio models and accessible hi‑fi offerings. Recent product upkeep and localized packaging improvements underline Sony’s intent to preserve studio credentialing in key markets.

- Sennheiser (Wedemark): Continues to invest in studio‑centric open‑back designs targeted at mixing and critical listening. Product introductions late in 2025 demonstrate an R&D focus on angled driver geometries and improving mixing accuracy.

- Audio‑Technica (Machida): Strengthens its professional lineup with both passive and USB hybrid strategy for studio applications, signaling a pragmatic overlap between legacy analog performance and modern DAW workflows.

- Beyerdynamic (Helicon) and AKG (Harman): Both brands continue to leverage Tesla‑type driver improvements and proven ergonomic platforms to keep professional buyers within their ecosystems.

- Boutique and high‑end specialists (Grado, Focal, Audeze): These players drive premium aspirational demand and technological differentiation — handcrafted materials, planar magnetic drivers and high‑resolution tuning — and will continue to set aspirational price points in the category.

While market concentration favors established names with strong channel ties, there remains measurable white space for entrants that combine disciplined cost management with differentiated acoustic IP. PW Consulting’s competitive index in the report benchmarks product families against engineering sophistication, service coverage and aftermarket economics.

Strategic implications and recommended 2026 actions

- Prioritize supply resilience over marginal SKU expansion. With driver lead times extended, ramping multiple new premium SKUs without secured supply contracts increases execution risk. Favor incremental product improvements with locked‑in supplier commitments.

- Rebalance portfolio towards aftercare and service offerings. Our pricing and margin models show that extended warranties, driver rebuild services and certification partnerships increase customer lifetime value without proportionally raising inventory risk.

- Implement a targeted compliance acceleration program. Firms that complete RoHS‑driven design changes early in 2026 will avoid the worst of the compliance cost curve and secure uninterrupted access to major EU channels.

- Optimize channel mix with data‑driven SKU rationalization. Use the playbooks in the report to align inventory to channel velocity and to reduce working capital tied to slow‑moving premium SKUs.

- Consider tactical near‑shoring for premium assembly. For select high‑margin SKUs, moving final assembly closer to core markets mitigates tariff volatility and shortens lead times, at an acceptable increase to unit labour cost.

What you will gain from the full report

This release is intentionally selective — it highlights strategic conclusions and operational playbooks while withholding the detailed segment‑level tables, region‑by‑region and application‑level financial splits that our clients rely upon for transaction execution and budget planning. The full report contains complete numerical appendices, scenario worksheets, supplier scorecards and a downloadable set of templates to operationalize the recommendations above.

Who should read this

- CEOs and CFOs of headphone OEMs and sound‑engineering brands—planning capital allocation and margin protection for 2026.

- Heads of procurement and supply chain—seeking negotiation triggers and lead‑time mitigation tactics for premium driver components.

- Product and engineering leaders—prioritizing compliance and feature trade‑offs under cost pressure.

- Private equity and M&A teams—evaluating bolt‑on opportunities and portfolio plays in a market with a moderate concentration of established incumbents.

Next steps

PW Consulting is offering a limited set of executive briefings in Q3 2026 to walk through bespoke implications for your business, including a tailored sensitivity analysis and supplier mitigation plan. For access to the full dataset, exhaustive segment tables and our implementation annexes, please visit the PW Consulting report page and request the Worldwide Headphones Without Mic Market report (base year 2025).

Closing perspective

The Worldwide Headphones Without Mic market is not a high‑growth breakout sector, but it is a durable, specialty market with clear pathways to profitable growth for disciplined players. In 2026, success will come to organizations that convert the macro signals we describe — material cost inflation, extended premium component lead times, targeted regulatory upgrades and evolving channel economics — into concrete operational actions. PW Consulting’s report furnishes the scenario analysis, procurement tools and competitive intelligence required to do exactly that, enabling leaders to move from reactive to proactive in a market where fidelity, credibility and supply reliability still govern long‑term brand value.

For detailed analysis of this topic, please visit the official page:Worldwide Headphones Without Mic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com