Worldwide Cold Ramming Paste (CRP) Market — Strategic Preview for 2026 Decision‑Making

PW Consulting’s latest market study on Worldwide Cold Ramming Paste (CRP) provides a concise, high‑resolution briefing designed to arm executive teams with the market intelligence needed to make decisive 2026 investment, procurement, and innovation choices. Our analysis synthesizes historic performance, supplier capabilities, regulatory pressure points, and forward scenarios. At a macro level, the CRP market grew from an estimated USD 385.4 million in 2020 to roughly USD 487.0 million in 2025 and is projected to continue expanding through the forecast window, reaching an anticipated market size above USD 640 million by 2032 under a baseline compound annual growth rate of approximately 4.0% (2026–2032). This trajectory masks material near‑term volatility and structural shifts that will shape supplier economics and buyer strategies in 2026.

Worldwide Cold Ramming Paste (CRP) Market

What this preview delivers

- Concise translation of large data sets into board‑level implications for capital allocation, sourcing, and product development.

- Practical diagnostics on supply‑side concentration and bargaining power dynamics, regulatory exposure, and feedstock risk.

- A pragmatic roadmap of near‑term actions (0–18 months) and strategic investments (18–36 months) that materially reduce operational and compliance risk while positioning for growth.

Report scope — actionable contents you can deploy in 2026

- Market sizing and trend analysis (historical 2020–2025, base year 2025, scenario forecasts 2026–2032) with upside/downside case workstreams for commodity shocks and regulatory accelerants.

- Supplier benchmarking and procurement playbook: vendor scorecards, negotiation levers, contract archetypes, and supplier risk heatmaps.

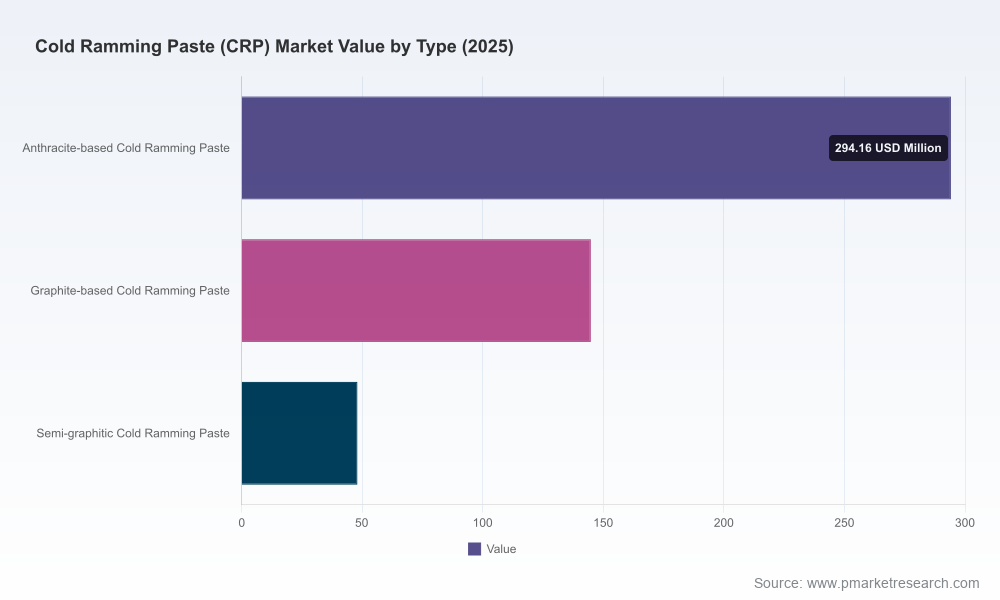

- Technology and product roadmaps: performance tradeoffs across anthracite, graphite and semi‑graphitic formulations and binder choices.

- Regulatory compliance matrix: PAH and VOC exposure pathways, mitigation levers, and timeline implications for regional permitting.

- Operational impact models for smelters and furnace operators: thermal performance, lining longevity, and maintenance scheduling tied to CRP selection.

- CapEx and OPEX implications: break‑even analyses for switching binders, retrofitting mixing facilities, and on‑site testing programs.

- M&A and partnership playbook: target profiles, valuation cushions, and integration challenges in a market where the top three and five firms command meaningful share of production capacity.

- Environmental & safety transition pathway: pilot protocols for low/zero‑PAH binders, supplier qualification checklists, and costed emissions/compliance scenarios.

- Sensitivity and scenario models for feedstock price swings, including anthracite and pitch availability, with recommended hedging strategies.

- Executive dashboards and procurement templates for immediate deployment by purchasing, sustainability, and operations teams.

Market dynamics and risk outlook

The CRP market is simultaneously mature and transitional. Core raw materials — calcined anthracite, artificial graphite, and binders historically dominated by coal tar pitch — underpin product performance, but they also expose the value chain to both supply shocks and tightening environmental controls. Industry practice has long relied on pitch formulations that deliver desired electrical and thermal properties; however, growing regulatory scrutiny over polycyclic aromatic hydrocarbons (PAHs) and other hazardous emissions is accelerating adoption of alternative binders (furan resins, lignin‑based formulations, and treated pitches) and reformulated recipes that target low or zero PAH content.

Worldwide Cold Ramming Paste (CRP) Market

This transition has three practical implications for 2026 decision‑makers. First, procurement teams will face a widening quality‑cost spectrum: legacy binders remain cost‑competitive but carry increasing compliance and reputational risk; eco‑friendly alternatives reduce regulatory exposure yet currently demand premium pricing and more rigorous qualification. Second, concentrated upstream supply for select feedstocks creates localized bottlenecks under stress events; our concentration metrics indicate a meaningful top‑tier presence (with the largest three and five producers accounting for substantial portions of installed capacity), so buyer diversification is no longer optional. Third, smelter and furnace operators must reconcile the short‑term operational risks of switching formulations (adhesion, density, resistivity) against medium‑term regulatory certainty and worker safety imperatives.

Worldwide Cold Ramming Paste (CRP) Market

Competitive landscape — who matters and why

The CRP competitive set is diverse, spanning global specialty materials firms, regional carbon producers, and engineered paste specialists. The market’s supply structure exhibits meaningful headroom for differentiation through formulation innovation, environmental credentials, and technical service capabilities.

- Elkem ASA (Oslo) — A premium supplier with established cathode ramming products for aluminum electrolysis and a vertically integrated footprint. Elkem’s Elseal portfolio and industrial manufacturing bases provide scale and strong application engineering support for large smelters seeking turnkey supply and technical collaboration.

- Maruti Electro Carbon (India) — A regional technology leader focusing on thermal stability and resistance in high‑temperature environments. Maruti’s emphasis on performance and local service makes it a rapid partner for aluminium industries in South and Southeast Asia.

- Henan Rongxing Carbon (Rongxing Group, China) — A longstanding carbon/machinery conglomerate with product breadth, including eco‑friendly variants. Rongxing’s cost competitiveness and production scale make it a key partner for high‑volume procurements where qualification cycles are acceptable.

- Bawtry Carbon (UK) — Niche specialist geared to cathode and sidewall applications; strength lies in product series optimized for specific cell geometries and demanding operating regimes.

- Ningxia Hongyuan Huida & Ningxia Coalician (China) — Two producers with an explicit focus on environmentally optimized pastes and proximity to anthracite sources; both are important suppliers for operators prioritizing lower PAH formulations.

- Luoyang Longxin, Shandong Robert, Wuhai Cowin — Regional manufacturers providing a spectrum of performance and price points; relevant for operators seeking flexible qualification and localized supply chains.

- Carbone Savoie (France) — Notable for purpose‑built zero/low PAH products validated at industrial sites; their eco‑product lines are among the most advanced commercially available alternatives for regulatory‑sensitive customers.

These suppliers exhibit distinct strategic postures: some compete on scale and logistics, others on formulation IP and environmental positioning, while a subset pursue close technical partnerships with smelters. For 2026 buyers, the selection calculus must weight supplier engineering support and sustainability credentials as highly as price.

Strategic playbook for 2026 — pragmatic moves that change risk profiles

- Reclassify supplier relationships: move key CRP vendors from transactional to strategic status if they offer low‑PAH product lines, co‑development capability, or local production near major smelting sites.

- Implement staged qualification programs for eco‑friendly binders: pilot at single‑cell or single‑furnace scale with a pre‑defined decision gate to scale adoption across assets.

- Embed regulatory hedging in procurement contracts: include clauses for supply continuity, binding substitution protocols, and co‑funded qualification trials for alternative formulations.

- Accelerate inventory resilience: build targeted buffer stock for critical feedstocks and CRP grades; combine with short‑term contractual flex to manage price spikes without overpaying long term.

- Prioritize capex for in‑house testing: modest investments in lab and trial kilns accelerate qualification and materially reduce time‑to‑adopt for new formulations.

- Explore strategic partnerships or bolt‑on acquisitions with specialist paste providers to secure IP and fast track transitions to lower‑PAH portfolios.

- Quantify total cost of ownership (TCO): merge product performance, maintenance intervals, downtime risk and compliance costs into purchasing decisions rather than relying on price/kg alone.

Why PW Consulting’s full report is essential for implementation

Our full market study goes beyond high‑level signals to provide operationally usable outputs: supplier scorecards, P&L impact models for binder swaps, regionally differentiated regulatory readiness timelines, and a prioritized list of supplier targets for strategic sourcing or M&A. The report’s scenario engine allows procurement and sustainability teams to stress‑test decisions against accelerated regulatory timelines, feedstock shocks, and demand swings from primary applications.

We deliberately present this preview as a strategic trailer — enough analytical depth to inform immediate executive conversations and to highlight the most material decisions facing 2026 boards, while reserving the precise segmentation matrices, supplier share tables, and downloadable procurement templates for the full report. Those proprietary elements convert insight into executable programs with measurable ROI.

Immediate next steps for leaders

- Schedule a 60‑minute briefing with PW Consulting to align your 2026 CRP strategy to corporate priorities (procurement, operations, sustainability).

- Commission an accelerated supplier qualification pilot for low/zero‑PAH formulations at a high‑impact site.

- Authorize a three‑month procurement review to redesign contracts with continuity and substitution clauses that reflect environmental transition risk.

Cold ramming paste sits at the intersection of commodity supply chains, industrial chemistry, and fast‑moving regulation. For organizations that act deliberately in 2026 — aligning procurement rigor with technical pilots and sustainability mandates — the coming years present an opportunity to convert compliance pressure into competitive advantage. PW Consulting’s full CRP market report provides the data, models, and playbooks to make that transition measurable and manageable. To access the complete intelligence package, including proprietary segment tables and operational templates, please visit our report page.

For detailed analysis of this topic, please visit the official page:Worldwide Cold Ramming Paste (CRP) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com