Global Direct Fed Microbial Market Forecast: Innovation and Sustainability Fuel Long-Term Growth

Health |

2026-07-10 11:24:56

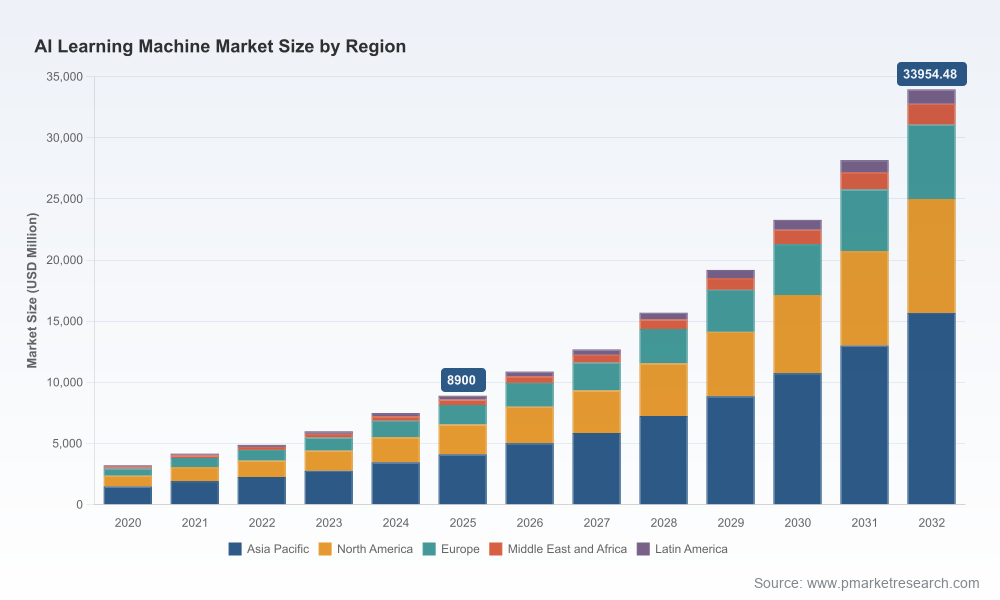

PW Consulting’s latest Worldwide AI Learning Machine Market report (base year 2025; forecast 2026–2032) arrives at a pivotal moment for education technology strategy. After a period of explosive expansion—reaching approximately USD 8.9 billion in 2025—the market is projected to sustain a high-growth trajectory (compound annual growth rate of 21.08% over the forecast window). Our modeled path sees the market moving beyond a mid‑double‑digit billion-dollar industry in 2026 and expanding toward an order-of-magnitude larger market by the early 2030s. For boards, product leaders and investors planning 2026 allocations, the implications are immediate: prioritize adaptive product architectures, content partnerships and regulatory-first go-to-market execution.

Worldwide AI Learning Machine Market

Actionable foresight, not just forecasts — We combine bottom‑up device economics, hardware-supply scenario analysis, and service monetization trajectories to translate headline growth into executable choices for 12–18 month budgets.

Worldwide AI Learning Machine Market

Tactical risk mapping — The market’s upside is balanced by systemic constraints (chip export controls, emergent AI safety standards, and shifting classroom policy). Our report maps those vectors to decision gates so teams can de‑risk major product and channel bets.

Worldwide AI Learning Machine Market

Competitive differentiation framework — As OEMs, platform players and content owners converge, the runway to meaningful scale hinges on integrated propositions. The report outlines high-probability partnership archetypes that drive faster adoption with K‑12 buyers and families.

Large and accelerating market base: From a near‑USD 9 billion industry in 2025, the market is forecast to advance sharply over 2026–2032 under multiple adoption scenarios. This momentum is not uniform; the winners will be those that simultaneously optimize hardware economics, content ROI and compliance workflows.

Moderate market concentration: The top three players do not monopolize the space—our concentration metrics indicate a market with room for category specialists and fast-moving challengers, yet with a clear tier of advantaged incumbents controlling more than a third of market value and a broader top-five influence approaching a majority share.

Regulation and policy will be co‑drivers of adoption: National AI safety standards and education ministry directives (including mandated AI literacy hours in some jurisdictions) are creating both guardrails and demand channels. Companies that embed regulatory compliance and auditability into product design will access institutional channels faster.

Proprietary market model: Annual market sizing (2020–2025 historicals and 2026–2032 forecasts), scenario matrices, and sensitivity tests focused on hardware cost curves and service ARPU assumptions.

Go‑to‑market playbooks: Concrete tactics for device makers, curriculum partners, and platform companies — pricing blueprints, bundling strategies, and retention levers tailored to consumer and institutional buying cycles.

Regulatory impact assessment: A line-by-line view of how emerging AI security standards and education policies alter certification timelines, content approval flows and liability exposure across jurisdictions.

Vendor scorecards: Strategic profiles and capability maps for leading incumbents, challenger OEMs and content integrators—evaluated across product roadmap, model ownership, content exclusivity and supply-chain resilience.

Investment and M&A playbook: Decision criteria for acquisitions that accelerate model ownership, content exclusivity, or assembly and distribution capacity—plus a prioritized list of target archetypes.

iFLYTEK — Platform and content integrator: iFLYTEK has moved from speech and cognition IP into vertically integrated learning machines, pairing proprietary cognitive large models with device form‑factors optimized for K‑12 tutoring. Recent developments include exclusive content tie‑ups with global studios and reported rapid revenue expansion within its smart education segment—signals of an incumbent leveraging scale in both model and content layers.

Yuanfudao (Xiaoyuan) — Hardware + emotional UX focus: Yuanfudao’s Xiaoyuan product family emphasizes an interactive “tablet + intelligent base” approach that adds physical companionship and diagnostic workflows. Its strategy centers on conversion through engagement and on‑device diagnostics fed by company-controlled models.

Zuoyebang and TAL Education Group — Educational channel specialists: These organizations convert deep curriculum expertise into hardware propositions, reinforcing brand trust among parents and institutions. Their strength lies in content-to-device integration and existing customer funnels.

BBK, Readboy, Xiaodu and others — Hardware incumbents and platform extensions: A spectrum of consumer-electronics and legacy educational device suppliers are upgrading to AI capabilities, prioritizing screen ergonomics, battery economics and curriculum‑sync software. They represent both distribution partners and potential acquisition targets for model-focused players.

Taken together, the competitive map shows differentiated paths to scale: model-first integrators leaning on content exclusivity; curriculum-first players converting trust into hardware; and hardware incumbents attempting to monetize installed bases via smarter software. Our report’s vendor scorecards reveal where each player’s asymmetry becomes a sustainable moat versus where it is transient—and where partnership or M&A makes strategic sense.

Standards & safety: Emerging security frameworks and generative AI safety requirements are raising the bar for verifiable content moderation, model provenance and data governance. Early compliance is now a go‑to‑market advantage, not merely a cost center.

Curriculum policy: Education ministry initiatives that mandate AI literacy and reduce unauthorized offline tutoring are expanding institutional demand for compliant at‑home learning tools. Vendors that can demonstrate curriculum alignment and audit trails will access procurement channels more swiftly.

Hardware supply constraints: Export controls on advanced semiconductors and equipment introduce plausible constraints on the highest‑performance edge compute options. Product roadmaps predicated on premium edge inference must include contingency architectures (hybrid edge/cloud inference, model quantization and partnerships for localized compute).

Content exclusivity as a conversion lever: Exclusive, age‑appropriate content (licensed animation, adaptive reading experiences and localized practice modules) materially increases device engagement and retention. Recent market moves demonstrate content partnerships are decisive switches in household purchase decisions.

Embed regulatory compliance into product roadmaps — treat auditability, content review pipelines and model safety as product features. This shortens procurement cycles with institutional buyers and reduces post‑launch friction.

Design modular computing stacks — prepare architectures that are resilient to chip supply shifts: model compression, split‑inference strategies and prioritized on‑device features can preserve UX under constrained hardware availability.

Prioritize rights to content that drives daily use — secure at least one exclusivity or co‑development relationship that aligns tightly with your target learning path. Content is the retention engine; devices without sticky content risk commoditization.

Balance model ownership with curated third‑party models — owning core tutoring models is valuable, but interoperability and curated third‑party integrations accelerate time‑to‑value, especially in multilingual contexts.

Use channel pilots to stress operational assumptions — run small institutional pilots that test device deployment, content management and parental UX before scaling. These pilots will surface operational costs that often dominate unit economics.

The public preview above highlights strategic lines of sight; the full report provides the detailed evidence and templates you need to act in 2026: a reproducible market model (with scenario toggles), granular vendor scoring, supply‑chain stress tests, and executable partnership playbooks. Importantly, the report contains the complete segment-level forecasts and regional analyses that are critical for territory planning—data we intentionally hold for the full report to preserve competitive clarity for clients.

If your 2026 investment planning hinges on device design choices, content licensing windows, or procurement channel timing, this report is designed to be the operational backbone of that decision. PW Consulting’s industry team stands ready to convert the report into bespoke strategy sessions, due diligence support and implementation roadmaps tailored to executives seeking to capture the next wave of AI‑enabled learning growth.

For access to the complete dataset, segment breakouts, and vendor scorecards, visit the official report page to request the full Worldwide AI Learning Machine Market report and associated advisory packages.

For detailed analysis of this topic, please visit the official page:Worldwide AI Learning Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com