Global Photonics Industry Trends and Innovation Outlook Through 2031

Other |

2026-03-16 13:03:44

As organizations prepare 2026 capital plans and operational roadmaps, Pw Consulting is releasing a concise strategic preview of our forthcoming Worldwide Materials Recovery Facility (MRF) Market report. Built on a detailed base year of 2025 and a seven‑year forecast horizon (2026–2032), the study quantifies a resilient market trajectory — with the global MRF market estimated at approximately USD 4,887 million in 2025 and projected to grow at a compound annual growth rate (CAGR) of 6.61% through 2032, reaching roughly USD 7,649 million by the end of the forecast period. This preview highlights the report’s decision‑grade insights while intentionally withholding the granular segment and regional line items to preserve the full analytical value of the primary research available in the full report.

Worldwide Materials Recovery Facility (MRF) Market

Timing: 2026 is a pivot year for MRF investors and operators. Regulatory drivers, raw‑material volatility and a rapid cadence of technology product cycles mean that capital allocation and retrofit decisions made now will materially affect throughput economics and revenue capture for the next decade.

Worldwide Materials Recovery Facility (MRF) Market

Market scale and growth: With a mid‑single digit to low‑double digit aggregate growth profile (CAGR 6.61%), MRF investments can deliver scalable returns when coupled with execution that captures technology productivity gains, feedstock quality improvement and selective geographic exposure.

Worldwide Materials Recovery Facility (MRF) Market

Competitive fragmentation: The market remains fragmented — the top three providers account for under one‑fifth of global share (CR3 ~18.45%), and the top five for less than 30% (CR5 ~27.8%). That structure leaves room for regional specialists, equipment innovators and integrators to win sizeable pockets of demand via targeted differentiation.

Forward‑looking investment models: Sensitivity models that link CAPEX, OPEX and feedstock quality scenarios to IRR and payback across a range of MRF typologies and throughput scales. These models are populated with base assumptions updated through 2025 and can be customized to client inputs.

Operational playbooks: Step‑by‑step guidance for plant retrofits, automation roadmaps, labour‑mix optimization, and contract structures for feedstock supply and offtake. Each playbook includes implementation milestones and KPI templates tailored to common governance models (municipal, private, public‑private partnership).

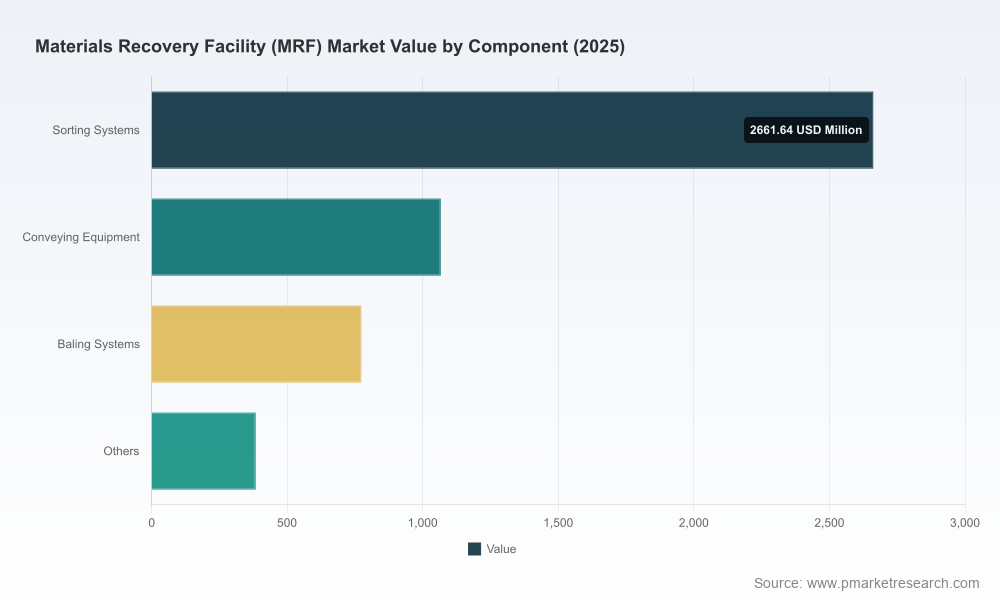

Technology assessment matrix: A vendor‑agnostic evaluation framework crossing optical sorting, ballistic separation, AI robotics, shredding and baling systems. The matrix scores each technology on recovery uplift, integration complexity, lifecycle costs and scalability.

Regulatory and policy scenario analysis: Structured scenarios that translate near‑term regulation shifts (collection mandates, import/export controls, subsidy windows) into demand pulses and capital timing implications for MRFs globally.

Commercial due diligence: Benchmarked supplier scorecards, contract pitfalls, and a short list of sourcing strategies that de‑risk deliveries and speed commissioning.

Executive decision checklist: A condensed board‑level pack that converts technical findings into capital authorization language and a 12‑month implementation calendar.

Regulatory acceleration: Several jurisdictions have tightened collection and processing mandates, raising minimum standards for separate collection and recycled content requirements. These rules are driving near‑term demand for both new MRF capacity and targeted upgrades to existing plants to meet stricter material quality thresholds.

Feedstock value volatility: Resin and commodity price swings since 2024 have altered revenue dynamics for recovered streams. Commodity price sensitivity increases the importance of automation and material quality control to avoid margin erosion during price downturns.

Labor and operating cost pressures: Wages and local operating costs have increased in key markets, pushing operators toward greater mechanization and hybrid labor models. Labor availability and wage inflation should be key assumptions in any 2026‑era business case.

Capital availability and public funding windows: Public grant programs and infrastructure stimuli remain important enablers for upgrade cycles. Timing of capital inflows and grant allocation criteria can accelerate retrofit projects and alter payback timelines.

Technology progress: Sensor‑based sorting and AI‑driven robotics are shifting recovery performance curves — increasing both the throughput accuracy and the economics of single‑stream operations when applied correctly.

The competitive texture of the MRF market is a mix of global systems integrators, specialized equipment manufacturers and agile regional engineering firms. The following firms are illustrative of the types of strategic behavior that matter for 2026 planning:

CP Group (Netherlands) — A turnkey provider that continues to expand capacity footprints via large single‑stream installations. Recent capacity additions and project wins indicate a focus on scale and integrated operations as a route to capture whole‑asset economics.

Tomra (Norway) — A technology leader in sensor‑based sorting whose product launches are directly improving plastic recovery rates and optical separation performance. Rapid product innovation from sensor vendors compresses the technology‑adoption cycle for forward‑looking operators.

Bulk Handling Systems (BHS) (United States) — Combining AI robotics with heavy engineering, BHS is positioning to serve high‑volume facilities in developed markets. Certification and standards alignment amplify buyer confidence in robotic automation for MRF environments.

Metso (Finland) — Supplies modular and heavy‑duty recycling plant equipment, with strengths in metals, paper and integrated crushing/screening, making it a common partner where mixed streams require robust pre‑processing.

Machinex (Canada), STADLER Anlagenbau (Austria), Van Dyk Recycling Solutions (Netherlands), and Eggersmann (Germany) — These regional specialists differentiate through customization, ballistic separation know‑how, and turnkey delivery models that cater to municipal and commercial clients with specific local requirements.

Recent vendor moves — new product introductions, capacity expansions and certification wins — show two related trends: (1) technology differentiation is accelerating, and (2) project delivery scale is increasingly important for long‑term service contracts. For buyers, this means procurement decisions must weigh short‑term performance gains against long‑term vendor stability and aftermarket support.

Risk — Feedstock pricing shocks: Even modest resin or commodity swings materially impact recovered‑material revenue streams. Scenario testing in our models shows that a conservative revenue sensitivity assumption materially alters acceptable payback windows.

Opportunity — Automation retrofit: Targeted investments in sensor upgrades and robotic pickers often pay back faster than full plant rebuilds, particularly when combined with improved upstream collection sorting that raises input quality.

Risk — Regulatory compliance timing: When collection mandates accelerate, late movers may face higher capex and forced fast‑track builds. Early engagement with regulators and access to grant windows mitigates this execution premium.

Opportunity — Strategic partnerships: Co‑development agreements between material processors, consumer packaging companies and technology vendors can secure supply and offtake terms that stabilize revenue assumptions for new MRF capacity.

Adopt a two‑track capital strategy: fast‑payback automation retrofits for existing facilities and selective greenfield investments in high‑growth corridors. Use our decision matrix to size investments against throughput uplift and incremental recovery yield.

Prioritize modularity: specify modular, upgradeable technologies to avoid asset obsolescence as sensor and AI performance improve. Contract structures should embed options for phased technology insertion.

De‑risk feedstock: secure mixed‑waste to separated‑stream conversion programs with collection partners, and lock short‑term offtake agreements for primary recovered commodities where possible.

Engage early with funders and regulators: align project timelines with funding windows and compliance deadlines to capture grants and avoid rush‑build premiums.

Benchmark vendors on lifecycle economics and service agreements: given the fragmented supplier landscape, due diligence must go beyond initial performance claims to include spare parts availability, remote diagnostics capabilities and long‑term upgrade roadmaps.

The report is underpinned by primary interviews, supplier scorecards, a bottom‑up facility build model and commodity pricing scenarios updated through 2025. While this preview shares headline market scale and trajectory (base year 2025, CAGR 6.61%, forecast to 2032), the detailed segmentation tables, region‑level forecasts and full vendor benchmarking are intentionally withheld here to preserve the tactical value of the primary research. These detailed datasets — including throughput‑by‑typology, component‑level capex and regional demand ladders — are available within the full report and companion data workbook.

Use this document to align leadership on the big‑picture implications for 2026: capitalize on automation and modularity, protect margin against feedstock volatility, and position to capture near‑term regulatory‑driven demand. For execution, obtain the full report to access the financial models, asset‑level cost build‑ups, and vendor scorecards that translate these high‑level recommendations into investable plans.

To secure the full Worldwide MRF Market report, detailed forecasts, and customizable decision tools for 2026 execution, please contact Pw Consulting or visit our report page for purchasing and licensing options. The full deliverable includes the datasets and templates that will allow your team to stress‑test any of the scenarios described above and to convert strategy into a 12‑month implementation plan.

For detailed analysis of this topic, please visit the official page:Worldwide Materials Recovery Facility (MRF) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com