PW Consulting Release: Strategic Preview — Worldwide Concrete Densification Polishing Material Market, 2026 Outlook

Executive snapshot

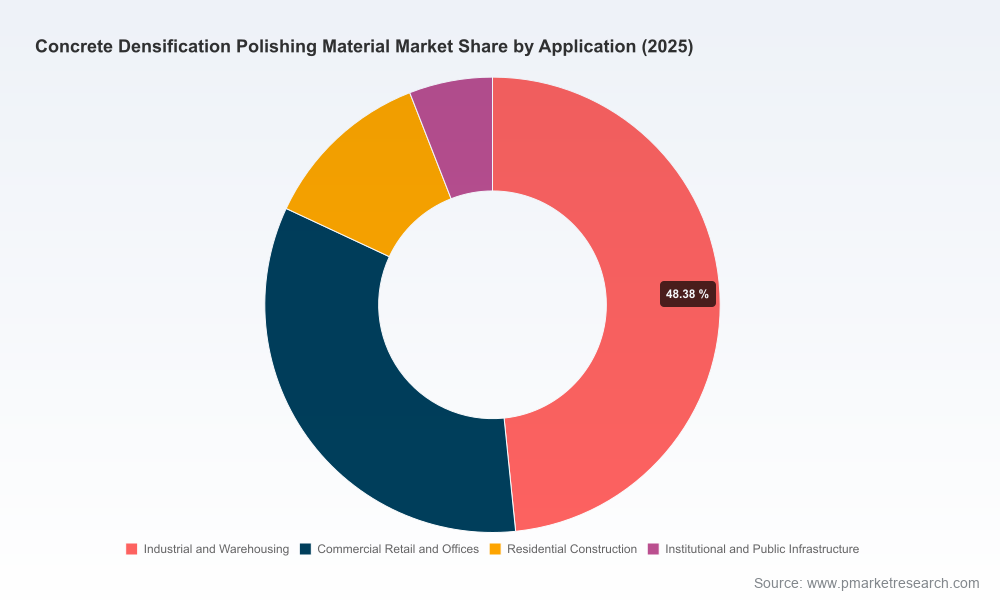

PW Consulting's new market study on Worldwide Concrete Densification Polishing Materials delivers a focused strategic resource for executives planning capital allocation, product development, supply-chain hedging, and commercial expansion in 2026. Building from a 2025 base year, our top-line modeling values the global market at approximately USD 985.4 Million in 2025 and anticipates a clear growth trajectory into 2026 and beyond — the report projects a compound annual growth rate (CAGR) of 6.15% across the 2026–2032 forecast window, with the market approaching roughly USD 1.50 Billion by 2032. These headline figures reflect structural demand for higher-durability, low-maintenance polished concrete across industrial, commercial, institutional and residential construction programs, and they frame the near-term strategic choices firms must make.

Worldwide Concrete Densification Polishing Material Market

Why 2026 is a decision point

The market enters 2026 at an inflection where raw-material dynamics, regulatory calibration around embodied carbon, and rapid product innovation combine to alter returns to incumbents and newcomers alike. Sodium-silicate based chemistries — the backbone for many densifier formulations — have shown pricing sensitivity to soda ash, energy, and logistics. In early 2026, spot pricing for sodium silicate varied across major sourcing geographies, reflecting a band of pricing that should inform procurement and inventory strategies. Concurrently, sustainability frameworks (notably new crediting approaches under building standards like LEED v5 and GWP optimization initiatives) are elevating Environmental Product Declarations (EPDs) from nice-to-have marketing assets to transaction-level requirements in many specification processes. PROSOCO’s January 2026 release of EPDs for multiple densifier SKUs underscores this shift and signals the competitive advantage for manufacturers that can supply third-party-validated life-cycle data.

Worldwide Concrete Densification Polishing Material Market

What the report delivers — practical intelligence for 2026 strategy

PW Consulting’s study is deliberately operational. Beyond top-line sizing and trend narratives, the full report contains:

Worldwide Concrete Densification Polishing Material Market

- Demand-side drivers and scenario-based forecasts calibrated to construction activity and sector-specific adoption curves;

- Raw-material sensitivity models that quantify margin exposure to sodium silicate, colloidal silica and upstream feedstock volatility;

- Supplier and channel mapping, including distribution footprints and contractor adoption barriers;

- Commercial playbooks for pricing strategy, specification capture, and installer training to accelerate uptake of premium densifier systems;

- Regulatory and sustainability trackers that translate EPDs and emerging green-building scoring into procurement levers and revenue opportunities;

- Vendor scorecards and a competitive heat map that evaluate technology differentiation, manufacturing scalability, geographic coverage, and customer support capabilities;

- Case studies and technical appendices for specification teams, floor owners, and institutional procurement officers.

Each module is designed for direct application: procurement managers get actionable hedging scenarios; product and R&D leaders receive prioritized innovation pathways; business development teams obtain playbooks to win specification and contractor loyalty.

Market structure and competitive dynamics — a snapshot

The densification polishing materials market remains notably fragmented. Our concentration metrics indicate that the top three suppliers account for a modest portion of market share (CR3 ~21.5%), while the top five reach roughly a third of the market (CR5 ~33.8%). This fragmentation creates both near-term pricing pressure and longer-term consolidation opportunity.

Key industry participants demonstrate diverse strategic postures:

- Curecrete Distribution leverages legacy technology and system-based offerings (notably the Ashford Formula and RetroPlate) to defend premium channels and global accounts.

- W. R. Meadows integrates densifier chemistries into broader flooring systems (LIQUI-HARD ULTRA, INDUROSHINE), using bundled solutions to lock in specification pathways for commercial and industrial projects.

- Sika’s global platform and broad chemical portfolio allow it to cross-sell densifiers into major architectural and industrial programs where single-source procurement is preferred.

- The Euclid Chemical Company, LATICRETE and PROSOCO differentiate via product breadth, contractor support, and increasingly via sustainability documentation — PROSOCO’s EPD rollout in early 2026 is a case in point.

- Specialist innovators (e.g., Adhesives Technology Corporation/Convergent with silica-free STRiON:Fortify, colloidal silica technologists such as Ecolab, and performance-focus players like Duraamen and Hyper Grinder) create technical disruption that forces incumbents to accelerate development or partnership strategies.

- Regional and niche suppliers (Xtreme Polishing Systems, Rio Floor and others) maintain local contractor loyalty through rapid service, competitive pricing, and tailored formulations for environment-specific needs.

For strategic leaders, the lesson is clear: scale and distribution matter, but product differentiation (technical performance, application efficiency, and certified sustainability credentials) will decide who captures the profitable growth pockets in 2026.

Actionable strategic implications for 2026

Executives using the PW Consulting report should consider the following prioritized actions:

- Secure raw-material exposure: implement procurement hedges and multi-sourcing for sodium silicate and colloidal silica; use the report’s sensitivity models to quantify margin levers and inventory thresholds.

- Invest in certification: accelerate EPD development and third-party validation where your product roadmap supports measurable GWP improvements; certification is becoming a transaction filter for large institutional customers.

- Differentiate via system-level solutions: bundle densifiers with polishing systems, coatings, and installer training to increase switching costs for contractors and owners.

- Pursue targeted M&A or partnership strategies: given a fragmented market, bolt-on acquisitions can rapidly expand geographic reach or add proprietary chemistries that reduce reliance on volatile feedstocks.

- Operationalize sustainability into pricing: translate validated life-cycle advantages into premium pricing or preferred-spec status in public and corporate procurement.

- Deploy a channel enablement program: invest in installer certification, digital specification tools and field trials to reduce adoption friction and proof performance in real-world settings.

Risks and mitigations emphasized in the study

The report identifies three clusters of near-term risk and outlines mitigation blueprints:

- Input-cost volatility — mitigate via long-term purchasing agreements, regional inventory nodes, and reformulation where feasible to reduce soda-ash sensitivity.

- Specification risk tied to sustainability — preempt by funding EPDs, aligning product development to lower-GWP chemistries (e.g., colloidal silica and advanced lithium formulations), and building data transparency into commercial proposals.

- Competitive displacement from novel technologies — monitor silica-free alternatives and invest selectively in trials or licensing to avoid being undercut by performance claims that change installer preferences.

How leaders should use the PW Consulting report in their 2026 planning cycle

Use the study as an operational playbook for three planning horizons:

- Immediate (0–6 months): update procurement terms and run raw-material stress tests against existing contracts; prioritize certification projects that unlock large accounts.

- Near-term (6–18 months): pilot system-level offerings with strategic contractor partners; institute channel training and digital specification tools; evaluate bolt-on acquisition targets identified in the vendor scorecards.

- Medium-term (18–36 months): scale validated low-carbon product lines, integrate sustainability into pricing, and pursue geographic expansion where the report’s demand overlays indicate the strongest ROI.

Each stage is supported by templates and scenario outputs in the full report so commercial teams can move from analysis to executable plans within weeks, not months.

Closing perspective

Concrete densification and polishing materials are at a strategic crossroads. Structural demand growth — quantified in our forecast and underpinned by durable occupancy trends and low-maintenance infrastructure priorities — creates a compelling growth runway. Yet margin upside will accrue to firms that manage raw-material exposures, secure sustainability credentials, and build system-level ties with contractors and owners. PW Consulting’s report gives decision-makers the actionable intelligence and playbooks needed to win in 2026 and beyond.

For the complete dataset, detailed regional and application splits, vendor scorecards, and the operational toolkits referenced in this release, please consult the full PW Consulting report and supporting appendices available on our report page.

For detailed analysis of this topic, please visit the official page:Worldwide Concrete Densification Polishing Material Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com