Europe Power Bank market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-14 09:23:21

PW Consulting’s latest market intelligence on the Worldwide Optoelectronic Safety Laser Scanner market positions 2026 as a pivot year for industrial safety architecture and mobile autonomy strategies. After a period of steady expansion through 2020–2025, the market has entered a new phase where product innovation (3D sensing, miniaturization, network integration), supply‑chain fragility, and evolving standards converge to reshape procurement, product roadmaps, and M&A calculus. Our report synthesizes quantitative market trajectories with practitioner‑grade operational guidance to help leaders convert uncertainty into competitive advantage.

Worldwide Optoelectronic Safety Laser Scanner Market

By the close of the 2025 base year the market reached a material scale, and our forecast shows sustained mid‑single‑digit to high‑single‑digit growth into the forecast horizon. The market is projected to grow at a compound annual growth rate (CAGR) of approximately 7.15% over the 2026–2032 period, reflecting both upgrade cycles in industrial automation and the increasing adoption of advanced safety perception on mobile platforms.

Worldwide Optoelectronic Safety Laser Scanner Market

For executives planning 2026 budgets, this profile matters for three reasons: first, capex and product investments made in 2026 will determine eligibility for fast‑growing segments (outdoor mobile, 3D safety); second, component lead times and cost volatility mean design‑wins hinge on supplier strategy executed this year; third, regulatory updates and certification pathways adopted now will accelerate time‑to‑market for next‑generation offerings.

Worldwide Optoelectronic Safety Laser Scanner Market

The market shows a clear concentration trend: the leading three vendors together command a majority share, and the top five capture roughly three quarters of the market. That concentration creates both defensive and offensive opportunities. Incumbents can leverage scale to integrate software and services, extend into systems safety lifecycles, and negotiate favorable component contracts. Challengers and OEMs must therefore focus on niche differentiation—size, integrated perception, certified outdoor operation—or partner with system integrators to bypass direct share battles.

Product innovation in 2024–2026 has accelerated along three vectors: dimensionality (2D → 3D), environmental hardening for outdoor mobile use, and integration with industrial networks and vision systems. Recent platform launches and updates illustrate the direction—compact ultra‑small scanners optimized for space sensitive AGVs/AMRs; certified 3D LiDARs aimed at outdoor collision avoidance; and scanners with integrated cameras and safety‑grade networking to simplify diagnostics and zone configuration.

For R&D and product teams, the immediate implications are clear: design cycles must prioritize modularity (sensor fusion readiness), certification roadmaps (safety PL/SIL compliance), and thermal / IP robustness for expanded use cases. Failure to account for these trajectories risks product obsolescence within two upgrade cycles.

Upstream concentration and geopolitics materially affect program risk. Compound semiconductor wafers and laser diode supply are dominated by a small set of suppliers; past export restrictions and capacity constraints have doubled lead times on critical substrates and pushed spot prices upward. Concurrent export controls and national self‑sufficiency policies have shifted procurement complexity from logistics teams to product strategy owners.

Standards and guidance updates are increasingly prescriptive. Revisions to positioning guidelines for protective devices require updated safety distance calculations and introduce supplements that explicitly address measurement error and mechanical wear. Compliance with established standards (IEC 61496, IEC 61508, ISO 13849) remains mandatory, and new certification pathways for 3D sensors are emerging.

Companies that actively engage in standards committees, publish compliance toolchains, and offer certified reference designs will accelerate adoption among safety‑conscious customers. Certification is not merely cost—it's a strategic sales enabler.

The competitive field blends global diversified automation leaders, specialist sensor manufacturers, and focused niche players. Recent initiatives exemplify the strategic playbook:

For buyers, the competitive landscape means procurement is no longer a purely technical comparison: it is a negotiation over lifecycle services, certification support, and supply‑chain resiliency.

PW Consulting’s full report is engineered for decision-makers who need executable outcomes rather than academic summaries. The deliverables include:

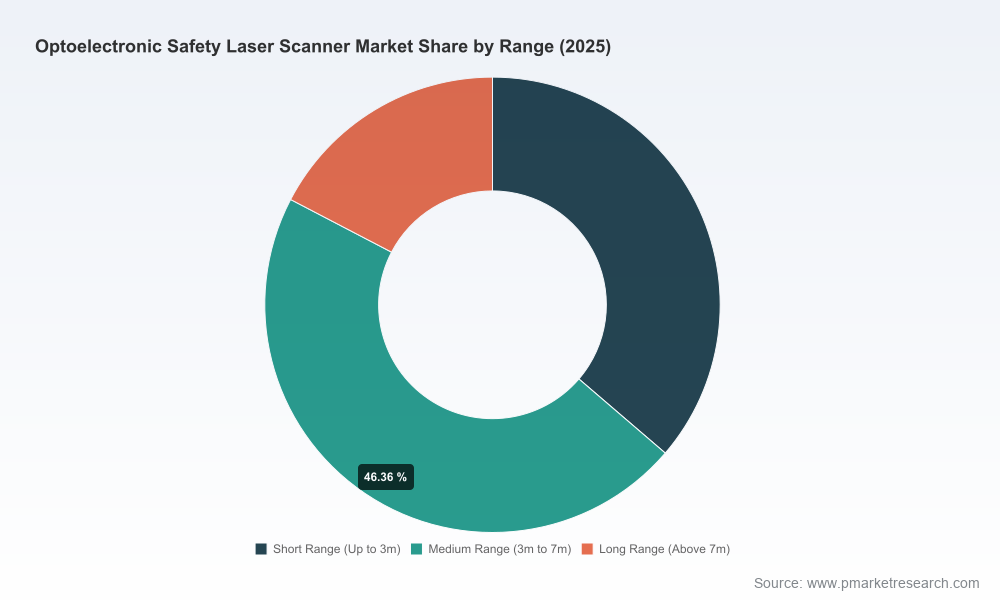

We intentionally avoid publishing granular segmentation figures in this release; the full intelligence pack contains the detailed breakdowns and modelling assumptions necessary to execute procurement, product and M&A decisions.

The optoelectronic safety laser scanner market is maturing rapidly. Growth is healthy and persistent, but the competitive and operational terrain is changing: component concentration and geopolitical frictions raise execution risks, while standards evolution and product innovation create pathways for differentiation. For executives planning resources or transactions in 2026, the immediate priority is to convert market momentum into defensible capabilities—through supplier strategy, certification investment, and service ecosystem design.

PW Consulting’s full report provides the tactical blueprints and scenario models that will be indispensable for teams making those calls this year. For organizations seeking to move from awareness to action, our analysis connects market theory to the operational levers that deliver revenue and reduce risk. Contact our research team or visit the published report page for the complete dataset, proprietary model files, and the consultant‑ready annexes that support implementation.

For detailed analysis of this topic, please visit the official page:Worldwide Optoelectronic Safety Laser Scanner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com