Product Protection Infrastructure – A Comprehensive Analysis of the Extended Warranty Landscape and Its Growing Importance

Other |

2026-07-15 09:26:46

As companies plan capital allocation, product roadmaps and go‑to‑market strategies for 2026, the sauna steam generator market presents a clear growth runway underpinned by steady demand in both residential and commercial wellness segments. PW Consulting’s new market study — covering the 2020–2025 historical window and a 2026–2032 forecast horizon — projects the global market to expand at a compound annual growth rate (CAGR) of 6.61%. The market size grew from approximately USD 512.5 Million in 2020 to USD 707.1 Million in 2025 and, under our base scenario, is modeled to approach USD 1.1 Billion by 2032. This briefing summarizes the report’s strategic value for 2026 decision-making and outlines the practical actions senior executives should consider now.

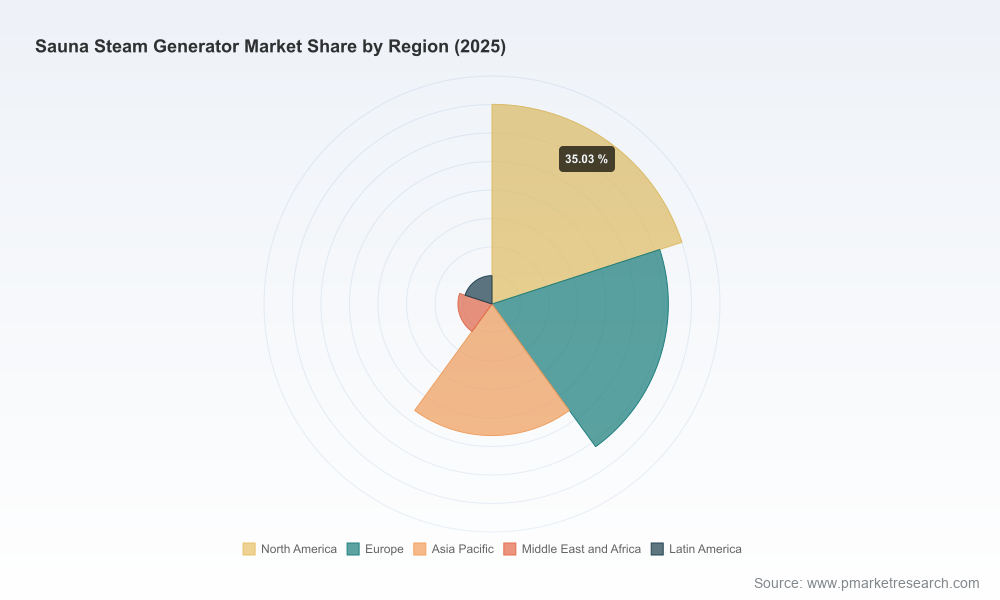

Worldwide Sauna Steam Generator Market

Growth with structure: The market is neither hyper-fragmented nor tightly consolidated. Leading vendors account for a meaningful share of shipments while a long tail of specialized manufacturers serves niche commercial and custom projects. PW Consulting’s concentration analysis shows the top three players control a material portion of sales, and the top five exert majority influence — a dynamic that creates room for scale-driven advantage yet preserves opportunities for focused innovators.

Worldwide Sauna Steam Generator Market

Regulation and technology driving product cycles: New efficiency and safety requirements are accelerating product refreshes and creating switching points for large buyers — a dynamic that favors suppliers who can demonstrate compliance and measurable operating savings.

Worldwide Sauna Steam Generator Market

Commercial demand tailwinds: The post‑pandemic rebound in wellness tourism and investment in hotel and spa retrofits is a durable commercial driver. Parallel consumer trends — home wellness upgrades and smart‑enabled luxury fittings — are supporting steady residential replacement and upgrade cycles.

Market sizing and validated forecasting (2020–2032): A transparent model calibrated to market shipments, vendor reporting and end‑market activity, expressed in USD Millions and inclusive of scenario ranges for conservative, base and accelerated demand.

Competitive benchmarking and capability maps: Profiles for incumbent suppliers — from legacy brands focused on North American and European markets to specialist OEMs serving commercial installers — including product portfolios, channel strategies, manufacturing footprints and recent innovations.

Regulatory and standards impact assessment: Quantified implications of emerging energy efficiency rules and certification requirements on product redesign costs, time‑to‑market and warranty economics.

Value‑chain cost builds and sensitivity analysis: Bottom‑up costing that isolates material, assembly, testing and certified installation labor inputs, with sensitivity runs for stainless steel price volatility, freight spikes and labor rate escalation.

Buyer playbooks and RFP templates: Ready‑to‑use commercial instruments for procurement teams evaluating vendor bids for both retrofit and new‑build projects.

M&A and partnership screeners: Criteria and shortlists for strategic acquisitions, minority investments and distribution partnerships, aligned to capability gaps identified in a firm’s product roadmap.

Service and aftermarket strategy toolkit: Guidance on warranty design, remote diagnostics adoption and spare‑parts logistics models to improve lifetime margins.

Our review synthesizes public filings, trade show disclosures and primary interviews to map competitive positioning. Several incumbent vendors define the market’s shape:

Steamist (Long Island City, NY): Deep breadth across residential and commercial portfolios; strength in scalable capacity ranges. Attractive to buyers seeking configurable systems for mixed‑use facilities.

Mr. Steam (Hauppauge, NY): Brand recognition in luxury residential and spa channels; accelerating adoption of app‑enabled controls and premium user experiences. Recent product launches underscore a push into connected wellness ecosystems.

Amerec (Woodinville, WA): Focus on reliability and commercial continuity. Product lines emphasize robust operation for mid‑sized installations.

TyloHelo (Hillerstorp, Sweden) and Harvia (Muurame, Finland): European heavyweights with integrated sauna ecosystems and distribution strength across institutional buyers. Their roadmaps reflect energy‑efficiency optimization consistent with tightening European standards.

KLAFS (Schwäbisch Gmünd, Germany) and Saunacore (Richmond Hill, ON): Niche specialists serving hotel and spa fit‑outs, where certification, custom engineering and stainless‑steel boiler expertise matter most.

Recent vendor activity matters. Examples from our research: Mr. Steam introduced a next‑generation Bluetooth‑enhanced model in early 2025, pointing to product differentiation via connectivity and user experience; TyloHelo showcased a new steam series at a major trade event in late 2024; Harvia refreshed its export catalog with energy‑efficient models in 2024. Collectively, these moves signal an industry shift: product innovation is now coupled to regulatory compliance and channel digitalization.

Raw materials and cost pass‑through: Stainless steel price pressure is observable — PW Consulting’s inputs show notable YoY increases that materially alter bill‑of‑materials for boilers and housings. Executives must model scenarios where steel, coatings and specialty components increase procurement costs and commoditize margins.

Regulatory tightening: In major markets, energy efficiency and safety standards are accelerating product obsolescence. For example, recent directives require commercial steam systems to meet elevated efficiency thresholds by 2026, which has consequences for legacy installed bases.

Labor and installation constraints: Certified technician shortages and higher hourly installation rates are inflating total installed cost in mature markets. Service network depth and training programs are now competitive differentiators.

Certification and liability: UL and equivalent local certifications are gating factors for commercial sales in regulated markets. Compliance delays can stall projects and erode contract credibility.

Demand variability tied to wellness tourism and hospitality investment cycles: While wellness tourism expanded meaningfully in recent years, projects can be lumpy and tied to capex timing in lodging and municipal wellness investments.

Prioritize energy‑efficiency upgrades in your product roadmap. Re‑engineer heating loops, insulation and controls to meet or exceed regional efficiency mandates — this reduces regulatory risk and creates a premium product tier.

Lock in raw‑material agreements and hedges for critical stainless steel inputs. Even modest price swings materially affect margins; multi‑year supplier deals or strategic inventory buys can be decisive.

Invest in certified service capacity. Train and certify installation partners, and consider outcome‑based contracts (e.g., guaranteed uptime) for large commercial customers to deepen account relationships.

Leverage connectivity as a value lever. App‑enabled controls, predictive maintenance and remote diagnostics shift revenue to high‑margin service streams and differentiate in residential luxury segments.

Use M&A selectively to acquire market access or niche engineering capabilities (e.g., stainless‑steel boiler fabrication, high‑efficiency controls). With the market moderately concentrated, targeted acquisitions can double down on channels or speed up compliance initiatives.

Product leaders: Use the report’s price‑to‑cost build to set target BOM costs and prioritize engineering sprints that yield the greatest efficiency gains per dollar.

Procurement teams: Apply our vendor scorecards and supplier risk matrix when negotiating fixed‑quantity contracts and to benchmark freight and lead‑time risks.

Commercial teams and integrators: Leverage RFP templates and buyer playbooks to convert hospitality and spa retrofit opportunities, particularly where energy rebates or modernization budgets are available.

Corporate development and private equity: Use the M&A screeners and concentration data to assess roll‑up potential, consolidation targets and geographic expansion opportunities.

In keeping with our “trailer” approach to market intelligence, this preview surfaces the strategic implications and core macro figures but intentionally withholds the full segmentation matrices and the granular regional/application revenue breakdowns that underpin our commercial models. These segment‑level tables and the underlying vendor share allocations are highly actionable — and are provided in full in the report package to licensed clients to support procurement, pricing and M&A diligence.

Request the full dataset and interactive model: Get access to the downloadable Excel model that powers our forecasts, including scenario toggles for raw material prices, labor rates and regulation timing.

Commission a rapid (6–8 week) strategic sprint: We can tailor the market model to your product lines, run cost optimization workshops and produce an execution roadmap aligned to your FY‑2026 priorities.

Engage for M&A due diligence or vendor selection: Our transaction teams combine technical steam system expertise with commercial diligence capabilities to accelerate deal timelines and reduce integration risk.

For senior leaders preparing 2026 budgets and product launches, the choices made now will determine who captures share as the market evolves under cost, regulatory and service pressures. PW Consulting’s Worldwide Sauna Steam Generator Market report translates market growth and structural shifts into concrete commercial options — from which products to prioritize to which partners to recruit. To obtain the full report, the interactive model, and vendor scorecards — including the detailed segmentation tables not published here — please visit our report page or contact our analyst team.

For detailed analysis of this topic, please visit the official page:Worldwide Sauna Steam Generator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com