Car Transport Service in Bangalore – Safe and Affordable Vehicle Relocation Solutions

Other |

2026-06-22 06:27:32

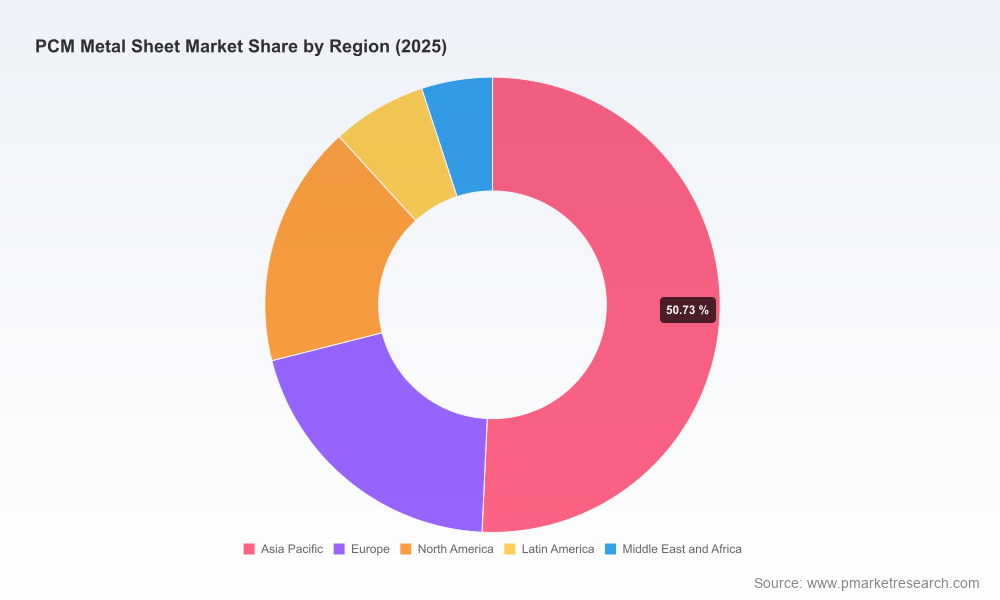

PW Consulting’s latest PCM (Pre‑Coated Metal) Metal Sheet Market study is designed as a decision-grade briefing for executives planning capital allocation, procurement strategy, product development, and M&A activity in 2026. The global market — measured on a USD Million revenue basis — reached approximately 4,850.5 Million in 2025 and PW Consulting forecasts steady expansion through the 2026‑2032 horizon at a compound annual growth rate (CAGR) of 5.15%. By the start of the forecast, the market is modeled at roughly 5,157.8 Million in 2026 and is projected to approach 6,893.7 Million by 2032 under the base scenario.

PCM Metal Sheet Market

This release functions as a strategic “trailer”: we surface the structural forces, competitive dynamics, and tactical playbooks that will determine winners and losers in 2026, while preserving the full granular segmentation, proprietary supplier scoring, and interactive modeling for subscribers to the full report.

PCM Metal Sheet Market

Market trajectory: After a recovery period in the early 2020s, the PCM market has entered a phase of steady, mid‑single‑digit growth driven by appliance replacement cycles, urban construction activity in select markets, and a modest premiumization trend where durable, high‑value coatings command higher margins.

PCM Metal Sheet Market

Consolidation signal: The market concentration is material. Top producers capture a meaningful share of industry shipments, creating a landscape where commercial terms, quality consistency and logistic reliability are differentiators for large buyers.

Input cost pressure: Steel and coil pricing remain a key lever. Our monitoring shows a persistent premium for cold‑rolled coil (CRC) versus hot‑rolled coil (HRC), and recent mid‑cycle uplifts in HRC benchmarks are raising base metal cost floors — an immediate commercial pressure for 2026 procurement planning.

Actionable supply‑risk maps to prioritize dual‑sourcing and near‑shoring where it materially reduces lead time and rust‑risk exposure.

Cost pass‑through models that quantify margin impacts across plausible metal‑price scenarios and help validate indexation clauses in long‑form supplier contracts.

Product roadmaps linking coating technologies (UV, PVDF, film laminates, antimicrobial finishes) with total cost of ownership for appliance OEMs and building product manufacturers.

Commercial playbooks for negotiating quality warranties, colour‑match tolerances, freight and storage terms — with sample contractual language and scorecards to evaluate suppliers objectively.

Bottom‑up market model (2020–2025 historic; 2026–2032 forecast) with sensitivity testing across price, demand elasticity and substitution (aluminum vs steel substrates).

Supply chain heatmaps and lead‑time analysis by source region, logistics corridor and end‑use sector.

Technology and materials primer covering substrate options (cold‑rolled steel, electro‑galvanized, hot‑dip galvanized, aluminum) and typical zinc coating ranges used in PCM manufacturing, including implications for corrosion resistance and coating adhesion.

Commercial intelligence: supplier scorecards, CR analysis and a proprietary “PCM Reliability Index” built from factory audits, third‑party certification status and field performance claims.

Deal and capex guidance: an M&A screen with valuation markers, and recommended payback scenarios for coil‑centre investments or coating line upgrades.

Regulatory and sustainability annex: EPD considerations, RoHS/ISO compliance checkpoints and recommendations for integrating PCM metrics into corporate sustainability reporting.

Integrated mill‑coaters with global footprints remain advantaged: several incumbent steel majors and regional champions combine upstream steelmaking, coil processing and branded coating systems to offer long warranties and streamlined logistics. These players can flex capacity and protect quality through integrated control of substrate and coating steps.

Regional specialists and contract coaters are competing on agility and service: select suppliers are differentiating by rapid colour‑matching, short‑run custom colours and value‑added services such as embossing, coil slitting and local coil centre processing that reduce OEM inventory burdens.

Quality and lab‑verified performance are table stakes: suppliers that publish third‑party validation (salt spray, colour conformity, ISO 9001 and external EPDs) consistently win larger appliance and building customers. Recent industry disclosures underscore performance claims — for example, documented claims of zero rust incidents across high‑volume shipments and catalog refreshes that expand film‑coated options.

Global steel majors: focus on product warranties, branded prepainted alloys and long‑term agreements with major OEMs. They leverage scale and R&D for corrosion‑resistant chemistries and warranty programs.

East Asian champions: strong in high‑quality appliance grades and tight colour control; active in coating innovation such as antimicrobial surfaces and advanced film laminates.

Contract coaters and regional coil centres: winning business on service, short lead times and tailored logistics; these players are pivotal for manufacturers seeking to localize supply or avoid cross‑border freight volatility.

Input dynamics: US cold‑rolled coil maintains a discernible premium over hot‑rolled coil reflecting additional processing costs, and HRC benchmarks have recently moved higher month‑over‑month — a near‑term headwind for PCM margin if not hedged.

Coating choices and zinc specification materially change life‑cycle costs: zinc coating weights and substrate selection alter corrosion performance and warranty exposure — translating directly into price bands buyers should expect to pay for higher durability grades.

Pricing levers: indexation to metal price indices, quarterly repricing mechanisms, and quality‑based premia (colour stability, salt spray resistance) are the dominant commercial levers we recommend buying organizations prioritize in 2026 negotiations.

Certification expectation: customers and regulators expect ISO 9001 systems, third‑party testing (SGS, Intertek, BV) and increasing adoption of EPDs for coated products — a competitive requirement for suppliers targeting appliance OEMs and green building projects.

Material substitution and circularity: aluminum and higher‑recyclability coating formulations are gaining attention where weight or end‑of‑life considerations justify a premium; buyers must balance life‑cycle benefits against raw material cost differentials.

Secure short‑to‑medium term supply with indexed agreements: renegotiate contracts to include transparent metal‑index pass‑throughs, defined quality penalties and logistics SLAs tied to rust‑risk mitigation.

Run supplier scorecards and contingency plans: deploy the report’s supplier assessment templates to prioritize partners for critical SKUs and identify when to shift to local coil centres to reduce total landed cost.

Invest selectively in coating R&D or long‑term offtake with differentiated suppliers: where product premiumization is feasible (antimicrobial, high‑durability finishes), lock in supply and co‑develop performance claims.

Integrate cost‑scenario modelling into capital decisions: use the enclosed stress tests to validate payback for coil‑centre investments or vertical integration steps under varying metal‑price trajectories.

For executives evaluating supplier consolidation, capital projects, or product premiumization in 2026, the full PW Consulting PCM report provides: a transparent market model with downloadable scenario inputs; granular regional and end‑use segmentation; supplier scorecards with audit‑backed risk ratings; and template commercial terms calibrated to current metal pricing dynamics. These assets convert macro trends into executable tactics — from procurement playbooks to M&A screening checklists.

This preview highlights the strategic levers that matter as firms plan for 2026. Subscribers to the full report gain access to the detailed regional and application splits, price curves, supplier reliability matrices and the interactive forecast model that underpin the recommendations summarized here. To access the full dataset and PW Consulting’s executable playbooks, please visit our PCM Metal Sheet Market report page or contact our advisory team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:PCM Metal Sheet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com