Experts Predict Major Shift in Next-Generation Battery Technologies

Other |

2026-03-31 11:20:53

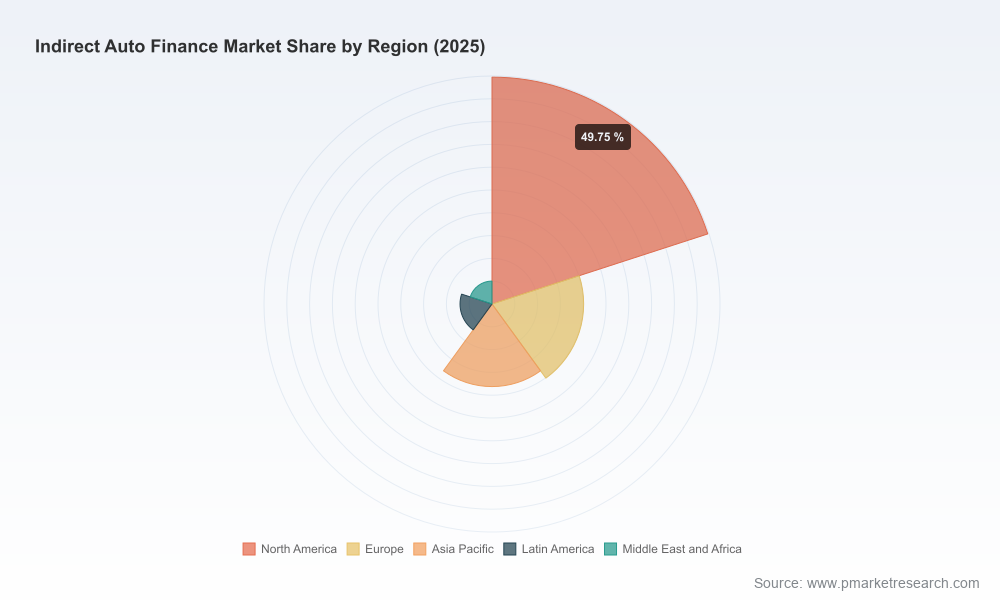

PW Consulting’s new Indirect Auto Finance Market report (base year 2025, forecast 2026–2032) synthesizes five years of historic performance with a seven‑year forward view to equip boards, CFOs, head strategists, and dealer networks with the conviction to act in 2026. The sector has demonstrated material scale and resilience — total industry revenues approached USD 300 Billion in 2025 and, at a compound annual growth rate of 6.85%, are projected to exceed USD 470 Billion by 2032. This briefing highlights the strategic takeaways from our full study and explains how senior leaders should translate those insights into 2026 priorities. (Full segment-level tables, regional and application splits, and model-level sensitivity analyses are available in the published report.)

Indirect Auto Finance Market

Macro-to-micro crossover: Affordability pressures and vehicle price inflation have begun to reshape origination patterns. Industry forecasts and credit bureau signals indicate modest near‑term pressure on originations, while total outstanding balances and dealer-originated finance debt have been rising — a dynamic that requires lenders to manage credit, liquidity and dealer relationships simultaneously.

Indirect Auto Finance Market

Regulatory recalibration: 2025–2026 regulatory activity has created both compliance headwinds and strategic openings. The Consumer Financial Protection Bureau’s advance notices and the Congressional scrutiny of dealer‑originated indirect channels place heightened emphasis on origination thresholds and supervisory scope. Separately, interpretations around ECOA liability have shifted in ways that change risk and underwriting frameworks for indirect channels.

Indirect Auto Finance Market

Competitive rebalancing: Non‑captives and bank lenders are accelerating share gains in dealer‑originated channels, while captive finance arms continue to exploit brand and captive product differentiation. The top five lenders account for just over half of market share concentration, underscoring both consolidation and persistent competitive fragmentation elsewhere in the market.

Scale and growth trajectory: The indirect auto finance market nearly doubled in scope over the 2020–2025 period and is expected to expand meaningfully through 2032 under our base case, with a 6.85% CAGR across the forecast horizon. This trajectory masks important inflection points tied to affordability cycles, used‑vehicle price normalization, and evolving dealer inventory financing needs.

Market structure: Concentration metrics indicate the market is neither dominated by a single actor nor fully atomized — the competitive landscape invites tactical consolidation, strategic partnerships, and differentiated value propositions across credit tiers.

Recalibrate origination playbooks. With dealer-originated flows still representing the vast majority of new auto loans, lenders must refine dealer incentive structures, underwriting overlays, and quick-turn digital pre-approval engines to preserve conversion rates while tightening credit performance.

Reassess liquidity and warehouse strategies. Dealer floorplan financing and short-cycle inventory finance are increasingly strategic. Operations and treasury teams should stress-test warehouse capacity under scenarios of slower retail turn and higher collateral holding periods.

Invest in compliance-by-design. Proposed changes to larger participant definitions and rulings affecting disparate impact theory require firms to bake traceable, auditable decision models into dealer channels. This is not a back-office exercise; it directly affects product capability and speed-to-market.

Differentiate on underwriting at the margin. As pricing compression emerges in prime segments, competitive returns will be found by tightening risk segmentation in non-prime strata, improving recovery analytics, and deploying real‑time behavioral signals that reduce loss severity.

Forge dealer-centric digital ecosystems. Dealers will select finance partners who reduce friction, offer transparent compensation structures, and integrate underwriting across DMS, CRM and e‑contracting platforms. Lenders that can provide embedded financing solutions will capture higher funnel conversion.

The market is an arena of distinct capability clusters: captive manufacturers with fidelity to vehicle brands, large national banks deploying scale and balance sheet depth, and specialist independents focused on margin optimization in non‑prime channels.

Captive finance arms (examples: Toyota Financial Services, GM Financial, Ford Motor Credit, American Honda Finance) will continue to exploit product-led capture — using leases, loyalty pricing and brand-aligned retention offers. Their advantage is structural: close alignment with OEM sales and supply chain visibility.

Large banks and bank-affiliated lenders (examples: Ally Financial, Capital One Auto Finance, Chase Auto Finance, Wells Fargo Auto) will compete on speed, rate competitiveness and dealer network breadth. These players are investing in digital underwriting and dealer integration to defend and expand dealer-originated share.

Independent specialists (examples: Westlake Financial Services) will remain pivotal in serving thin-file and non-prime segments. Their underwriting sophistication and flexible dealer products give them durable niches despite pricing pressure.

In practice, competitive advantage will be decided by three execution vectors: dealer economics (compensation and co‑op structures), underwriting precision (data and model agility), and platform openness (APIs, e‑contracting, and originations orchestration). Our full profiles of leading firms evaluate each company across these vectors, identify recent strategic moves, and model likely responses to regulatory scenarios.

Policy tightening around larger nonbank originator thresholds: Lenders should assume higher compliance costs and potentially more intensive examination intensity if annual originations cross newly proposed thresholds.

ECOA-related litigation risk and operational changes: Clarifications around disparate impact frameworks have already altered how pricing and dealer discretion must be documented.

Credit cycle sensitivity: TransUnion and other bureaus flag modest declines in new originations under affordability stress. Scenario planning should include a modest originations reduction and an extended recovery window for used-vehicle valuations.

Dealer finance concentration risk: Dealer-originated loan volumes and dealer finance debt trends will amplify counterparty exposure if inventory financing pressure intersects with demand softness.

Our full Indirect Auto Finance Market report is built for practitioners. It delivers:

Proprietary market size and forecast models (2020–2032) with Monte Carlo sensitivity and three scenario paths (baseline, downside, upside) calibrated to macro and policy shocks.

Competitive scorecards for the leading providers, benchmarking dealer reach, product breadth, digital maturity, and capital efficiency. Each provider profile includes business‑model stress tests and suggested strategic responses for 2026.

Deal‑level playbooks for dealer partnerships: recommended compensation architectures, underwriting delegation matrices, and implementation roadmaps to reduce dealer friction and legal exposure.

Compliance checklists and model governance templates aligned to the latest CFPB and Congressional guidance, including operational red flags to prepare for examinations and potential rulemaking changes.

Operational KPI dashboards and implementation templates for treasury, risk, and sales leaders to align incentives and measure progress against 2026 milestones.

Boards and executive teams: Use the report’s scenario outputs to set capital allocation ranges and to determine the timing and scale of dealer network investments versus captive product expansion.

Heads of Origination and Credit: Adopt the underwriting segmentation playbooks to improve marginal yield without materially increasing portfolio volatility.

COOs and Technology leaders: Prioritize investments in dealer API integration and e‑contracting modules that reduce cycle-time and produce auditable decision trails for compliance.

Risk & Compliance teams: Implement the compliance-by-design roadmaps and governance templates to insulate origination programs from evolving supervisory focus.

Dealer-originated channel dominance remains entrenched: independent analysis confirms the large majority of auto loans continue to originate via dealers, making dealer economics a primary battleground for share.

Market share movement toward banks and non-captives: industry reporting through early 2026 shows these providers growing share in dealer-originated loans, increasing competitive intensity.

Regulatory attention is active and actionable: CFPB notices and Congressional analysis during 2025–2026 have already produced material changes in supervisory emphasis, affecting underwriting documentation and origination thresholds.

For firms that want to preserve optionality and grow in 2026, we recommend a three-part immediate agenda: (1) quantify dealer exposure and reprice dealer incentives where they distort risk; (2) stand up a regulatory stress-test tied to the report’s downside scenarios and embed remediation playbooks; (3) accelerate dealer integration pilots with two to three priority dealer groups to validate speed-to-yes improvements and compliance traceability.

PW Consulting’s Indirect Auto Finance Market report packages the models, playbooks, and vendor-independent execution templates you need to convert these recommendations into measurable outcomes. We deliberately present deep, actionable analysis while reserving full segment-level tables and model workbooks for the report to enable a rigorous client follow-up and to protect analytic integrity. For the full dataset, granular segmentation, and the executable roadmaps referenced above, please consult the report and supporting models on our website.

For detailed analysis of this topic, please visit the official page:Indirect Auto Finance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com