Power Tools Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-18 10:39:24

PW Consulting’s new market study on Worldwide D-Ring Blood Pressure Cuffs provides a concise, decision-focused briefing for executives preparing strategy, procurement, and R&D roadmaps in 2026. Drawing on a 2020–2025 historical base and a 2026–2032 forecast horizon, the report synthesizes macro growth, competitive dynamics, regulatory constraints, and practical commercial levers. Key headline: the global D-ring cuff market, measured in USD million, expands steadily from the 2025 base year and is projected to grow at a mid-single-digit CAGR of roughly 7.0% through 2032—an environment that rewards disciplined product strategies and selective partnerships.

Worldwide D-Ring Blood Pressure Cuffs Market

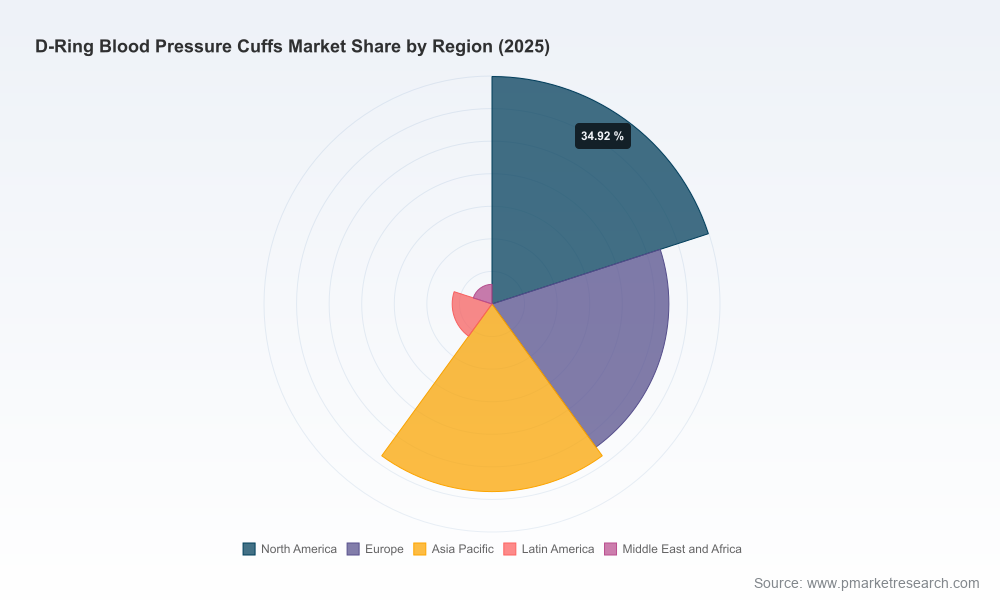

The market’s compound annual growth rate of 7.0% over the forecast window reflects several persistent tailwinds: the migration of monitoring from institutions to homecare, continued investment in non-invasive monitoring technology, and steady replacement cycles in hospitals and ambulatory centers. By design, this briefing emphasizes the overall scale and trajectory rather than granular regional or application splits; detailed segmentation tables and time-series by region, material and end-user are reserved for the full report and subscriber portal.

Worldwide D-Ring Blood Pressure Cuffs Market

Base and forecast framing: PW Consulting’s baseline calculations use 2025 as the reference year and project through 2032; the topline market value grows materially over the period, reinforcing the strategic importance of cuff product lines in device OEM and consumables portfolios.

Worldwide D-Ring Blood Pressure Cuffs Market

Market structure: concentration metrics indicate a market that is neither fully fragmented nor dominated by a single player—leading three firms control a meaningful but not overwhelming share of global revenues, and the top five approach majority market share. This creates room for mid-sized specialists and agile entrants to carve durable niches.

For executives preparing budgets and roadmaps for 2026, three practical implications flow from the market context:

Prioritize product modularity. With monitors and cuffs increasingly bundled in OEM ecosystems, configurable cuff families (reusable vs single-patient, fabric choices, sizing ranges and connection interfaces) provide optionality across hospital, ASC and homecare channels without multiplying SKUs unnecessarily.

Invest selectively in regulatory prework. Compliance to ISO 81060-1:2019 clinical validation and major market agency requirements is table stakes. Early investment in verification and clinical evidence shortens time-to-market and mitigates post-launch corrective costs.

Lock strategic supply positions for critical inputs. Medical-grade fabrics and bladder components are commoditized but subject to pricing swings and lead times; a modest prioritization of supplier diversification and safety-stock policies materially reduces commercial risk.

The landscape is shaped by a mix of large monitor OEMs and specialized cuff manufacturers. Key players—each with differentiated strategies—include established device OEMs selling proprietary or compatible cuff families, and independent cuff specialists focused on design, materials and single-use options. Recent corporate activity underscores strategic patterns market participants should watch:

OEM-led assurance and certification: Major monitor suppliers continue to bundle cuffs with patient monitors and pursue clinical/agency approvals to embed compatibility and infection-control claims—moves that raise switching costs for large hospital contracts.

Catalog expansion by specialists: Independent cuff companies are broadening size ranges and single-patient options to target homecare and bariatric segments, signaling that product breadth remains an effective route to capture adjacencies.

Channel and connectivity plays: Trade shows and product demos show an emphasis on one-tube connectivity, quick-fit ports and compatibility across monitor families—features that are becoming expected rather than exceptional.

PW Consulting’s competitive profiles synthesize publicly filed product claims, recent approvals and catalog activity to highlight each vendor’s addressable design strengths and go-to-market posture. The full report includes vendor scorecards, patent and partnership mapping, and a scenario matrix for likely competitive moves over the next 18–24 months.

Regulatory guardrails: ISO 81060-1:2019 imposes clinical validation requirements for cuff accuracy (typically validation within ±5 mmHg), and adherence to device-specific standards remains a procurement filter used by hospitals and large group buyers.

Procurement economics: Reimbursement rules materially influence buyer behavior in some markets—e.g., certain reusable cuff categories are covered under healthcare reimbursement codes, shaping price floors and competitive entry points for reusable designs.

Raw material sensitivity: Medical-grade fabrics and PVC bladders are modest-cost inputs, but unit economics are sensitive to raw-material pricing and conversion yields. PW Consulting’s unit-cost model allows manufacturers to stress-test margins under different commodity scenarios.

Our analysis translates market signals into a compact list of high-impact operational moves that firms can adopt in 2026 to protect or extend margins and share:

SKU rationalization with outcome-based bundling: Reduce complexity by standardizing on a small set of modular cuffs that serve multiple monitor interfaces and sizing needs; pair with service and warranty bundles to capture aftermarket value.

Targeted clinical evidence programs: Rather than broad, expensive trials, run focused validation studies that demonstrate accuracy and durability for key customer segments (e.g., homecare hypertensive patients, bariatric arms in hospital settings).

Selective vertical integration: Negotiate long-term supply agreements for high-risk inputs or co-invest in converting capacity with a trusted contract manufacturer to lock in lead times and improve per-unit costs.

Channel-specific value propositions: Design marketing and rebate programs tailored for homecare distributors vs hospital procurement—homecare buyers value simplicity and compatibility; hospital GPOs prioritize clinical evidence and sterile workflows.

The full report is structured for commercial teams, R&D leaders and procurement heads who must act in 2026. Core deliverables include:

Topline and scenario forecasts (2026–2032) with sensitivity runs versus low/high demand, reimbursement shifts, and raw-material shocks.

Competitive heatmaps and vendor scorecards summarizing product breadth, regulatory posture, channel strength, and recent strategic moves.

Supplier selection and cost-to-serve templates that translate fabric and bladder inputs into unit-cost and margin targets.

Go-to-market playbooks with segmented value propositions for hospital networks, ambulatory centers and the high-growth homecare channel—plus recommended KPIs to track adoption and churn.

Compliance checklist and a prioritized clinical validation plan aligned to ISO 81060-1:2019 and major agency expectations.

Decision support tools: interactive dashboards (license access) that let users explore the topline forecast, run "what-if" scenarios and download anonymized benchmarking tables.

Recent vendor activity illustrates practical competitive consequences for 2026 planning:

Regulatory clearances for antimicrobial or clinically enhanced cuffs raise the bar for hospital purchasing committees that now treat infection-prevention features as a procurement filter rather than an incremental benefit.

Catalog expansions into specialized sizes, including bariatric offerings, highlight the role of breadth in capturing one-off high-value contracts; however, breadth without evidence risks inventory drag.

Visible trade show demonstrations and connectivity innovations show that compatibility and ease-of-use will remain meaningful differentiators in tenders and high-volume channel agreements.

For product leaders: Use the report’s validation roadmap to prioritize a 12–18 month clinical program that targets the highest ROI use-cases for your core customers.

For commercial teams: Align pricing and rebate strategies to the reimbursement environment and test channel-specific bundles in pilot markets before broad rollouts.

For procurement and operations: Implement the supplier scorecard in the report to identify two near-term candidates for strategic supply agreements or co-investment discussions.

As the D-ring cuff market grows from the 2025 baseline through 2032 at an approximate 7.0% CAGR, companies that translate macro growth into disciplined product portfolios, targeted clinical validation and resilient supply chains will capture outsized returns. PW Consulting’s study blends quantitative projection with hands-on playbooks and vendor due diligence to shorten the path from insight to execution. To preserve the commercial value of our segmentation work while providing a clear decision framework in this briefing, detailed regional and end-use splits are held in the full report. Executives seeking the granular tables, interactive dashboards and vendor scorecards should consult the PW Consulting report page for access and licensing options.

For detailed analysis of this topic, please visit the official page:Worldwide D-Ring Blood Pressure Cuffs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com