Ewing Sarcoma Drug Market Size, Share, Technological Trends, and Forecast by 2032

Other |

2026-07-01 08:36:36

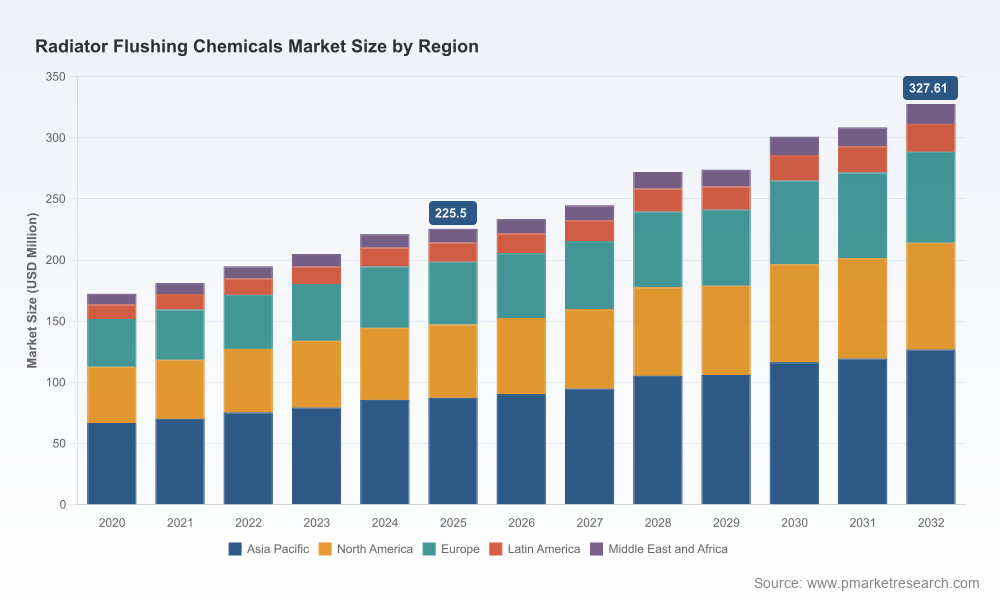

As the global automotive and industrial cooling ecosystems continue to evolve, radiator flushing chemicals are moving from a commoditized maintenance input toward a strategic product class that intersects regulatory compliance, materials science and aftermarket services. PW Consulting’s latest market intelligence finds the Worldwide Radiator Flushing Chemicals Market expanding from USD 172.4 Million in 2020 to USD 225.5 Million in the base year 2025, and projects sustained growth through the forecast window (2026–2032) at a compound annual growth rate (CAGR) of 5.48%. By 2032 the market is expected to exceed USD 327 Million under the report’s central scenario. This briefing explains why that trajectory matters for corporate strategy in 2026, what levers managers should prioritize, and which tactical moves can convert market tailwinds into defensible commercial advantage.

Worldwide Radiator Flushing Chemicals Market

Transition-driven demand: The cooling requirements of modern powertrains (including enhanced thermal management for hybrids and certain battery-electric platforms) and tighter maintenance standards across fleets are reshaping product requirements for flushing chemistries and service protocols. This is elevating demand for differentiated formulations and integrated service solutions.

Worldwide Radiator Flushing Chemicals Market

Input cost volatility: Upstream feedstock dynamics are already influencing supplier pricing strategies and margin profiles. Ethylene glycol experienced notable price swings through 2025 with a rebound from year-end lows; the market outlook for 2026 suggests an initial weakness followed by range-bound stability roughly in the RMB 4,000–4,400/ton neighborhood amid ample supply. Separately, phosphoric acid pricing observed regional spreads in early 2026 (e.g., around USD 1.21/kg in North America and USD 1.37/kg in Europe in March 2026), signaling localized cost pressures that will affect formulation economics and regional sourcing decisions.

Worldwide Radiator Flushing Chemicals Market

Regulatory ripple effects: Recent regulatory updates have indirect but material implications for the radiator chemicals value chain. For example, tighter U.S. EPA refrigerant management rules that became fully effective in 2026 raise the bar on reclaimed refrigerant quality and handling procedures, increasing compliance obligations for service providers. Likewise, building-code updates such as the California Energy Code 2025 (effective 2026) strengthen ventilation and EV charging requirements for new construction, indirectly accelerating electrification-related service volumes in certain markets and creating new thermal-management use cases.

Industry structure: The market remains moderately consolidated with leading firms capturing a meaningful share while a long tail of regional specialists and formulators persist. This creates distinct opportunities for scale players to invest in premium, performance-tuned chemistries and for agile specialists to capture niche fleet and industrial accounts.

Our full report is built as a practical playbook for 2026 strategy. It blends bottom-up market sizing with scenario-driven forecasts and a suite of tools designed for immediate operational use by product managers, procurement leads, M&A teams and business development executives. Key deliverables include:

Verified market sizing and trend maps (base year 2025; historical coverage 2020–2025; forecast horizon 2026–2032) with transparent assumptions and sensitivity ranges.

Demand-driver diagnostic — linking vehicle parc composition, maintenance intervals, industrial cooling cycles and aftermarket service models to forecast trajectories.

Raw-material risk models that quantify margin exposure to ethylene glycol and phosphoric acid price scenarios, and supplier concentration heatmaps to prioritize hedging and alternative sourcing.

Competitive benchmarking and playbooks — product positioning matrices, channel strategies for consumer retail vs. professional service centers, and pricing architecture for value-based selling.

Go-to-market and commercialization roadmaps for premium formulations (acidic, alkaline and solvent-based chemistries), including formulation risk checklists, regulatory compliance templates and label/packaging guidance for global rollouts.

M&A and partnership screening tools — quantified screens for targets (scale, technology, channel access), synergy models and integration risk assessments, accompanied by a 90/180/360-day execution checklist.

Proprietary scenarios (baseline, accelerated electrification, regulatory tightening) to stress-test capex, inventory and product development priorities.

Procurement and cost engineering — Build proactive feedstock strategies. Given the observed ethylene glycol volatility and regional phosphoric acid price differentials, procurement leaders should secure multi-sourced supply agreements and deploy hedging strategies tied to the most material inputs. Small formulation changes can materially affect COGS; run pilot syntheses to identify cost-neutral swaps.

Portfolio prioritization — Differentiate along performance and compliance. Formulations that reduce flushing time, lower water usage or minimize neutralization steps unlock both environmental and service efficiency claims attractive to commercial fleet operators and multi-site maintenance providers.

Commercial model innovation — Move up the value chain. Suppliers can capture higher margins by combining chemistry sales with diagnostic services, subscription-based maintenance contracts, or certified reconditioning programs that address both product and service lock-in.

Regulatory readiness — Treat compliance as a market access lever. U.S. EPA and regional code changes mean product labels, handling protocols and training programs must be updated in 2026. Early compliance — and the ability to certify service centers — becomes a competitive moat.

Capex and manufacturing footprint — Localize critical SKUs where input cost or regulatory regimes justify it. The moderate market concentration implies opportunities for regional players to secure premium positioning with localized inventory and faster service response times.

M&A and partnerships — Target capability gaps, not just revenue. Look for targets with unique formulation IP, fast-service networks, or fleet-contracted relationships. Integration playbooks should prioritize retention of technical talent and customer-facing field teams.

The market comprises global brands with broad aftermarket reach, specialty formulators with differentiated chemistries and regional players focused on price and service. Our report includes deep profiles and strategic positioning for the key players you’ll want to benchmark against and potentially engage as partners:

Prestone Products Corporation — A recognized consumer and professional brand whose multi-action cooling-system cleaners emphasize compatibility across metal types and a 2-in-1 cleaning-protect value proposition.

Valvoline Inc. — Brings vertically integrated service capabilities and a packaged offering that ties in its coolant product lines with flush services, creating cross-sell opportunities at service points.

Liqui Moly GmbH — A European specialty chemicals house that markets radiator cleaners engineered to remove scale and sludge, emphasizing performance restoration for water-cooled engines.

CRC Industries — Offers rapid-flush and rust-removal formulas that target professional service workflows where speed and non-acidic chemistries are prioritized.

Bar’s Leaks, BG Products, Jelmar (CLR PRO) and other specialty brands — Each brings distinct formulation and channel strengths (from buffing agents and biodegradable acids to phosphate-free blends) that appeal to different customer segments.

Regional formulators such as Chemtex Speciality and RX Marine — Operate in geographies and vertical niches (marine, industrial cooling) where localized formulations and service models are decisive.

Callington (ROX®) — Represents the concentrated, pro-focused SKUs aimed at professional workshops and fleet maintenance operations.

Collectively, the top three firms hold a material but not overwhelming share of the market (the report documents a three-firm concentration in the high 30-percent range and a five-firm share a touch north of 50%), which underscores both the benefits of scale and the persistent room for specialists to outcompete on technical differentiation or service execution.

Run a product-margin stress test against the report’s ethylene glycol and phosphoric acid scenarios to understand worst-case COGS impacts.

Prioritize one “premium” formulation for accelerated commercialization that reduces service time or offers environmental credentials attractive to fleet customers.

Audit regulatory compliance gaps across top markets and allocate budget to label updates, training and certified service-center rollouts.

Screen acquisition targets using the report’s M&A filters (technology, channel access, customer contracts) and run 100-day integration plans for shortlisted targets.

Design pilot bundled offers (chemistry + service + digital maintenance tracking) for fleet customers and measure churn and lifetime-value improvement.

Establish a quarterly raw-material watch and procurement trigger points aligned with the report’s price bands to avoid margin erosion.

This preview outlines the strategic contours derived from PW Consulting’s Worldwide Radiator Flushing Chemicals Market study. The full report contains the segment-level data, regional breakdowns, vendor scorecards and downloadable models that are intentionally withheld here to preserve the commercial utility of the research. For teams that must make budgetary, R&D or M&A commitments in 2026, the full dataset and executable playbooks provide the granular evidence-base required to de-risk decisions and accelerate time-to-value.

Contact PW Consulting to access the complete report, scenario models and a tailored briefing for your executive team. Our analysts are available to walk through the sensitivity models and help translate the findings into a 90-day action plan customized to your cost structure, product mix and growth ambitions.

For detailed analysis of this topic, please visit the official page:Worldwide Radiator Flushing Chemicals Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com