Asia-Pacific Spirometer Market: Key Trends and Future Growth Forecast 2025 –2032

Health |

2026-06-26 04:27:18

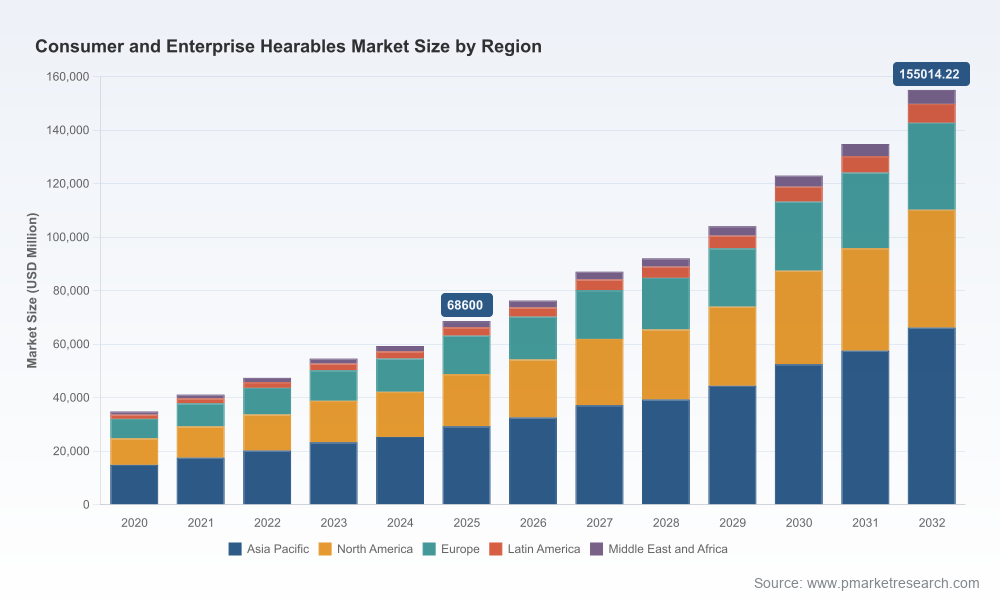

PW Consulting’s latest Worldwide Consumer and Enterprise Hearables Market report provides an executive-grade intelligence package designed to inform and accelerate strategic decisions in 2026. Built on a rigorous historical base (2020–2025) and a detailed forecast (2026–2032), the study synthesizes market sizing, competitive benchmarking, supply-chain stress-testing, technology roadmaps, and actionable go-to-market playbooks. The global hearables market has been one of the fastest-growing adjacent electronics segments — expanding from roughly USD 34.8 billion in 2020 to about USD 68.6 billion in 2025 — and is projected to sustain strong growth over the forecast horizon with a compound annual growth rate of 12.35% (2026–2032). By 2032 the market is expected to exceed USD 155 billion, creating both opportunity and disruption for vendors, enterprise buyers, and health-tech integrators.

Worldwide Consumer and Enterprise Hearables Market

Hearables have moved beyond entertainment: they are now platforms for communications, health monitoring, workplace collaboration, and immersive experiences. For 2026, strategic choices will determine who captures platform value versus who remains a component supplier. This report translates market momentum into board- and C-suite-ready guidance by mapping where revenue pools are expanding, which business models monetize features versus services, and which competitive moves materially alter market share dynamics. We adopt a “trailer” approach: this briefing reveals the direction and implications while the full report contains the granular splits, regional dynamics, and vendor scorecards necessary to operationalize decisions.

Worldwide Consumer and Enterprise Hearables Market

Growth profile — The category roughly doubled in scale across 2020–2025, and our forecast conservatively assumes a mid-teens annualized growth path into the following decade, underpinned by continued consumer adoption of TWS products, the emergence of hearables-as-health-devices, and increasing enterprise adoption for hybrid work and frontline communications.

Worldwide Consumer and Enterprise Hearables Market

Platformization — Hearables are evolving from discrete hardware to integrated hardware+software+services platforms. Vendors that convert single-sale hardware into subscription services (health analytics, enhanced noise suppression for enterprise UC, device management) will capture higher lifetime value.

Concentration — The market exhibits a moderate concentration profile: a small number of large vendors control a meaningful share of the market while a long tail of specialized players and regional OEMs compete on price, features, or clinical differentiation. Competitive intensity will increase around ecosystem lock-in and cross-device integration capabilities.

Supply-side constraints — Raw-material volatility (MEMS microphones, certain battery and rare materials, and quartz/silicon component lead times) and geopolitical trade policy (tariff changes and incentives for regional manufacturing) are immediate risk factors. Our supply-chain risk matrix quantifies time-to-impact for these shocks and models mitigation levers such as dual-sourcing and nearshoring.

Enterprises (IT procurement and occupational health teams): Hearables increasingly sit at the intersection of communications and health—adoption decisions must balance audio performance, security/certification, and interoperability with unified communications platforms. The report includes decision frameworks for total cost of ownership, pilot design, and phased rollouts that align procurement cycles to voice and health regulatory timelines.

Vendors (OEMs and component suppliers): Companies must prioritize two strategic bets — ecosystem integration (operating-system and cloud-service partnerships) and differentiated low-level sensory capabilities (microphone arrays, ANC, on-device AI inference). Our playbooks identify which investments produce defensible moats versus short-term feature parity.

Health-tech and clinical integrators: Hearing aids and hearables are converging. Vendors that can reliably demonstrate clinical-grade outcomes while navigating medical-device regulation will unlock premium pricing and recurring revenue through service subscriptions.

The competitive map spans consumer incumbents, premium audio specialists, hearing-health leaders, and enterprise-focused providers. Examples of strategic positioning reflected in the market:

Platform-integrated consumer leaders leverage OS and device ecosystems to embed hearables as default companions across devices, creating stickiness beyond pure audio. Recent product and firmware updates that add health and contextual-awareness features illustrate this evolution.

Premium audio brands continue to compete on fidelity and advanced ANC, which remain important for both consumer satisfaction and enterprise office-use cases. Differentiation here translates into margin resilience in premium segments.

Hearing-health specialists are closing the gap with consumer hearables by integrating AI-driven audiological features and building clinician-friendly management tools — a pathway to premium service revenue and closer ties with healthcare payers and providers.

Enterprise UC-focused players win where certification, multi-device management, and predictable call-quality metrics matter. Their strength is in selling into procurement cycles that value integration with contact-center and collaboration platforms.

To illustrate market momentum: industry shipment data and trade-show disclosures over the past 18 months have highlighted continued unit demand for TWS products and a rising emphasis on health and immersive audio at major events. Leadership moves (firmware additions for health monitoring; new AI-tuned form factors) are focused on convertibility of users into services customers rather than incremental hardware upgrades alone.

Component risk: MEMS microphone supply volatility and localized semiconductor disruptions remain high-impact triggers. We model scenarios where component lead-time extensions push product launch windows by quarters and quantify margin erosion under inventory buffers.

Regulatory risk: Evolving tariff regimes and medical-device classifications create windows of regulatory opportunity and complexity. We provide a compliance timeline and a “regulatory readiness” checklist tailored to companies commercializing health-related features.

Technology risk: Advances in on-device AI, ultra-low-power sensing, and new sensor types create both opportunity and product obsolescence risk. Our technology-adoption heatmap prioritizes which sensor and chipset investments are likely to yield sustainable differentiation.

PW Consulting’s report is structured to move from strategic context to execution. Key inclusions are:

Market model and forecast workbook (scenario-based) — downloadable models that allow users to stress test assumptions against different macro, regulatory and technology scenarios.

Vendor scorecards and competitive positioning — qualitative and quantitative assessments across capabilities, product roadmaps, channel strategy, and enterprise-readiness.

Go-to-market playbooks for vendors and procurement playbooks for enterprise buyers — including pilot templates, procurement KPIs, and pricing strategies that reflect service monetization pathways.

Supply-chain risk matrix and mitigation plans — component-level vulnerability mapping and supplier diversification options with time-to-implement estimates.

Regulatory scanner and timeline — an actionable checklist for health-feature rollouts, certification requirements, and tariff exposure.

Technology roadmap and patent/standards watch — highlighting sensory innovations, codec/ANC developments, and standards activity that affect interoperability and lock-in.

Based on our analysis, leaders should prioritize a short list of executable moves in the coming quarters:

Initiate targeted pilots that validate on-device health sensing or ANC-as-a-service in controlled enterprise environments, with measurement protocols aligned to procurement KPIs.

Lock in multi-sourcing agreements for key MEMS and silicon components and evaluate nearshoring options to reduce tariff and lead-time exposure.

Accelerate partnerships that embed hearables into collaboration stacks or into clinical workflows, capturing early subscription revenue while competitors chase hardware differentiation.

Deploy pricing experiments that separate hardware from recurring service elements, tracking conversion and churn to determine the most lucrative bundles by customer segment.

This briefing is a strategic summary; the full PW Consulting Worldwide Consumer and Enterprise Hearables Market report is the operational manual for 2026. It contains the granular regional and end‑user splits, the complete vendor scorecards, downloadable scenario models, and supplier‑level risk assessments that boards, product leaders, and procurement executives will use to set budgets and roadmap priorities. Organizations that pair the report’s quantitative modules with our advisory sessions gain access to tailored decision-support (market-entry, M&A diligence, and go-to-market sequencing).

The hearables market in 2026 presents a classic inflection: large-scale consumer demand continues to grow, while enterprise and health applications create new, higher-margin value streams. Success will favor organizations that treat hearables as platforms rather than discrete hardware, that operationalize supply-chain resilience, and that build partnerships across ecosystems. PW Consulting’s report gives leaders the strategic line-of-sight and executable tools needed to convert market growth into sustainable advantage.

To access the full dataset, vendor scorecards, and the downloadable forecast models referenced here, please consult PW Consulting’s full Worldwide Consumer and Enterprise Hearables Market report on our website.

For detailed analysis of this topic, please visit the official page:Worldwide Consumer and Enterprise Hearables Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com