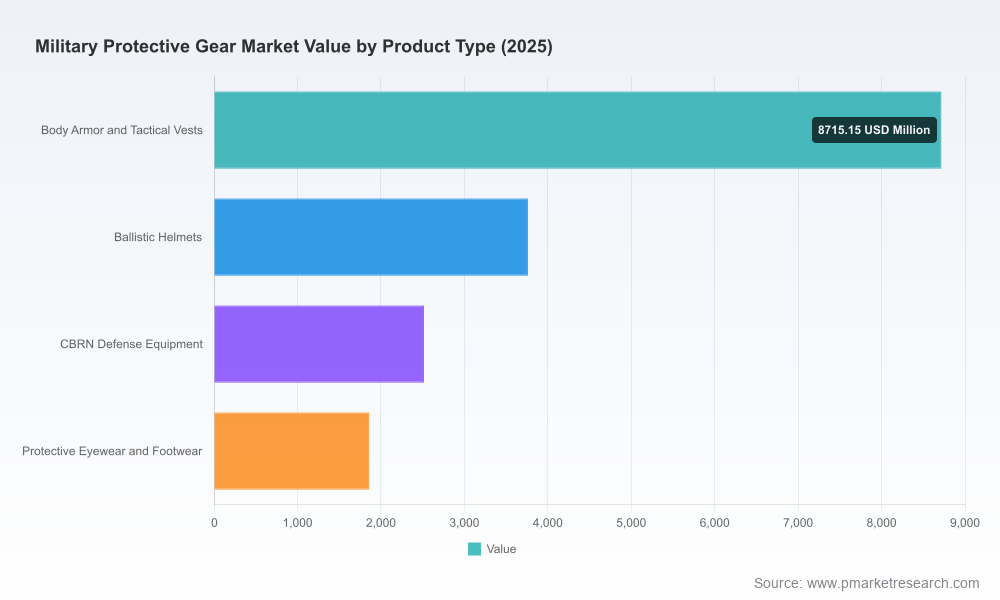

Worldwide Military Protective Gear Market — Strategic Insights for 2026 Decision-Makers

PW Consulting's latest market intelligence on the Worldwide Military Protective Gear Market equips leaders across defense OEMs, suppliers, procurement agencies, and investors with the forward-looking analysis they need to make high‑stakes 2026 decisions. Our base-year audit (2025) places the global market at USD 16,850.5 Million (revenue unit: Million, USD), up from USD 13,850.2 Million in 2020. The market is projected to grow at a steady compound annual growth rate (CAGR) of 4.5% through our forecast horizon (2026–2032), with our conservative baseline pointing to roughly USD 17,877.5 Million in 2026 and an expected expansion to approximately USD 22,931.2 Million by 2032.

Worldwide Military Protective Gear Market

Why this report matters in 2026

Procurement windows, industrial policy shifts, and technology roadmaps already scheduled for 2026 make this an inflection year for military protective systems. The combined pressures of modernization programs among NATO members, export-control regimes that restrict cross-border technology flows, and premium pricing for next‑generation ballistic materials mean that commercially viable product and supply strategies must be defensible on technical, regulatory, and financial grounds.

Worldwide Military Protective Gear Market

- Actionable foresight for procurement and budgeting: Use our 2026 baseline and 4.5% CAGR to stress‑test acquisition pipelines and sustainment budgets across mid‑cycle procurement reviews.

- Risk‑calibrated supplier strategy: Understand where scale, materials access, and certification capabilities matter most when selecting or partnering with suppliers.

- M&A and partnership signal map: Identify consolidation opportunities and partnership vectors in a market that shows moderate top‑end concentration alongside a diverse ecosystem of niche specialists.

What the report delivers — pragmatic, implementable intelligence

Beyond headline forecasts, PW Consulting’s Worldwide Military Protective Gear Market report was designed as a practitioner’s toolkit. It blends quantitative modeling with procurement- and operations‑level playbooks so that recommendations can be executed, not just discussed.

Worldwide Military Protective Gear Market

- Executive dashboard: 2020–2032 historic and forecast trajectories, scenario variants, and sensitivity tables to support 2026 capital and inventory planning.

- Supplier scorecards: Independent assessments of technology maturity, production footprint, certification readiness, and aftermarket service capabilities for leading vendors.

- Technology roadmaps: Comparative analyses of advanced ballistic fibers, UHMWPE composites, helmet‑integrated systems, and CBRN protection trends with time‑to‑adoption estimates.

- Procurement playbooks: Step‑by‑step guidance on RFP structuring, test and qualification gating, domestic industrial participation clauses, and export‑control compliance workflows.

- Supply‑chain stress tests: Scenarios for raw‑material price shocks, logistics disruption, and certification bottlenecks, with mitigation options and cost implications.

- M&A and partnership briefs: Target profiles, expected upside drivers, and integration risk matrices for dealmakers focused on building scale or capability verticals.

Market dynamics shaping strategic choices

Five dynamics dominate the competitive and procurement calculus in 2026:

- Material economics: Advanced ballistic materials — including aramid fibers and UHMWPE composites — command a premium. Their unit economics and manufacturing intensity directly influence product pricing, lifecycle costs, and the viability of lightweight, multi‑hit protection systems.

- Certification and testing overheads: Ongoing third‑party validation against evolving ballistic standards increases time to market and creates a defensible moat for manufacturers with established testing pipelines.

- Geopolitical procurement priorities: Rising defense spending targets among alliance members and preferences for regional sourcing are accelerating investments into localized manufacturing and technology transfer agreements.

- Integration of electronics and modularity: Demand for helmets and vests that host communications, sensors, and augmented reality overlays is reshaping product definitions from passive protection to integrated mission systems.

- Regulatory constraints on technology flows: Export controls, including ITAR-style regimes, constrain commercialization strategies for certain protective technologies and must be factored into go‑to‑market and partnership strategies.

Competitive landscape — strengths, gaps, and tactical moves

The market is neither a highly concentrated oligopoly nor a pure cottage industry; our concentration analysis shows a moderately fragmented landscape at the top with meaningful room for strategic consolidation. This creates a dual imperative: volume and scale matter for R&D and certification economics, while focused specialists capture premium niches with differentiated technologies and customer relationships.

- 3M Company: Leverages advanced composites and a systems approach to offer lightweight, multi‑threat helmets and integrated personal protection. Its R&D cadence and materials expertise make it a go‑to for program offices seeking proven material science partners.

- BAE Systems: Positions itself around integrated soldier systems and modular architectures that help military customers standardize interfaces across platforms — advantageous where interoperability and logistics simplicity are procurement priorities.

- Gentex Corporation: Focused on helmet systems with embedded communications and AR‑capable visors. Recent contract continuations on legacy helmet programs underscore the value of sustainment relationships and qualification continuity.

- DuPont and Honeywell International: Material suppliers that underpin the product strategies of OEMs. Their control over advanced fibers and composite shielding technologies creates upstream leverage; for OEMs, securing long‑term material access is strategic.

- Avon Protection and Revision Military: Specialists in respiratory and eye protection who are expanding into integrated offerings for high‑threat environments, positioning themselves well for CBRN and special‑operations demand.

- Regional producers (e.g., MKU, ArmorSource, Point Blank, Safariland): Deliver localized capability and cost competitiveness, often winning programs with regional preference clauses or rapid delivery windows.

Recent industry activity — contract renewals for advanced helmet programs, government orders for protective plates, and targeted acquisitions among niche suppliers — highlights two trends: (1) sustainment contracts and incremental upgrades are a steady revenue base, and (2) M&A continues to be the fastest route for capability aggregation for suppliers seeking to enter adjacent segments.

Strategic recommendations for 2026

PW Consulting’s advisory priorities for executive teams and procurement officials center on practical tradeoffs between performance, cost, and supply‑chain resilience.

- For OEMs: Prioritize modularity and open‑architecture interfaces to reduce obsolescence risk and create upgrade monetization paths. Invest in certification pipelines early to shorten procurement lead times.

- For material suppliers: Lock in strategic, long‑term offtake agreements with OEMs and co‑fund certification and test infrastructure to reduce client procurement friction.

- For procurement agencies: Build multi‑vendor qualification tracks and require clear sustainment pathways in initial contracts; treat export‑control compliance and technology transfer as bidding criteria—not afterthoughts.

- For investors and M&A teams: Target bolt‑on transactions that provide immediate technical differentiation (e.g., AR visors, CBRN integration) and evaluate cross‑border risk from export controls when pricing deals.

- For supply‑chain managers: Implement dual‑sourcing for critical ballistic fibers, stress‑test logistics under extreme scenarios, and quantify the premium for “assured” domestic supply versus lowest‑cost imports.

Using the forecast to make 2026 decisions

Our 2026 baseline and the 4.5% CAGR provide a defensible template for fiscal planning. Organizations should use our scenarios to calibrate three levers: procurement cadence (how many units per year), technology upgrade cycles (when to retrofit vs. replace), and sustainment economics (spare parts and lifecycle support). Even modest deviations from the baseline demand materially different inventory and cash‑flow strategies; the report’s sensitivity matrices convert those deviations into actionable budgetary adjustments.

What we intentionally withhold — and why

Consistent with the “trailer” principle of this release, we are publishing high‑level market sizes, growth rates, and competitive dynamics to establish credibility and strategic orientation. Detailed segmentation tables, region‑ and application‑level revenue splits, granular vendor market shares and contract‑level revenue breakdowns are reserved for the full report and online data portal. That granular intelligence is what procurement teams and deal‑makers rely on to size opportunities, validate supplier claims, and execute negotiations — and it is available through our secure report access.

How PW Consulting can help

Our team supports clients with tailored briefings, supplier due‑diligence packages, and hands‑on procurement playbooks built from the dataset behind this report. Typical engagements for 2026 include:

- Supplier shortlisting and technical verification for major modernization programs.

- Supply‑chain resilience audits, including raw‑material hedging strategies for aramid and UHMWPE inputs.

- M&A target screening and integration planning with an emphasis on certification continuity and export‑control exposure.

- Customized scenario planning workshops aligning finance, engineering, and procurement teams on a single acquisition and sustainment plan.

To move from strategy to implementation, decision‑makers should access the full report and dataset, which contains the granular segmentation, regional and application forecasts, vendor scorecards, contract databases, and test/certification timelines that are critical to executing 2026 plans. PW Consulting stands ready to convert that intelligence into bid‑ready procurement strategies, technical roadmaps, and deal execution support.

Contact PW Consulting for an executive briefing and secure access to the full Worldwide Military Protective Gear Market report to obtain the data and supplier intelligence necessary for confident 2026 decisions.

For detailed analysis of this topic, please visit the official page:Worldwide Military Protective Gear Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com