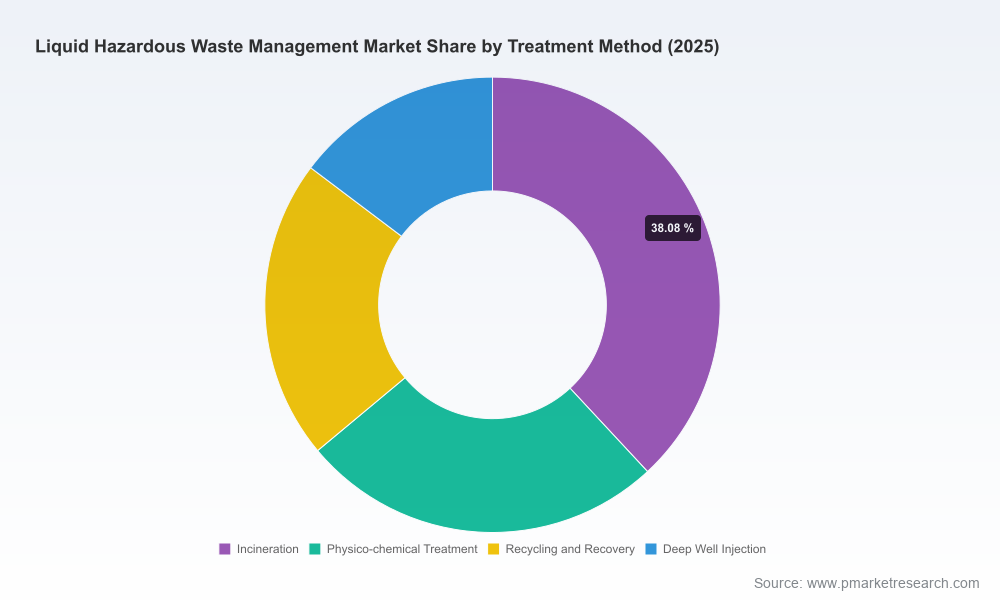

PW Consulting Predicts 6.08% CAGR for Liquid Hazardous Waste Management Market, Topping USD 73.34 Billion by 2032

Other |

2026-07-02 07:16:54

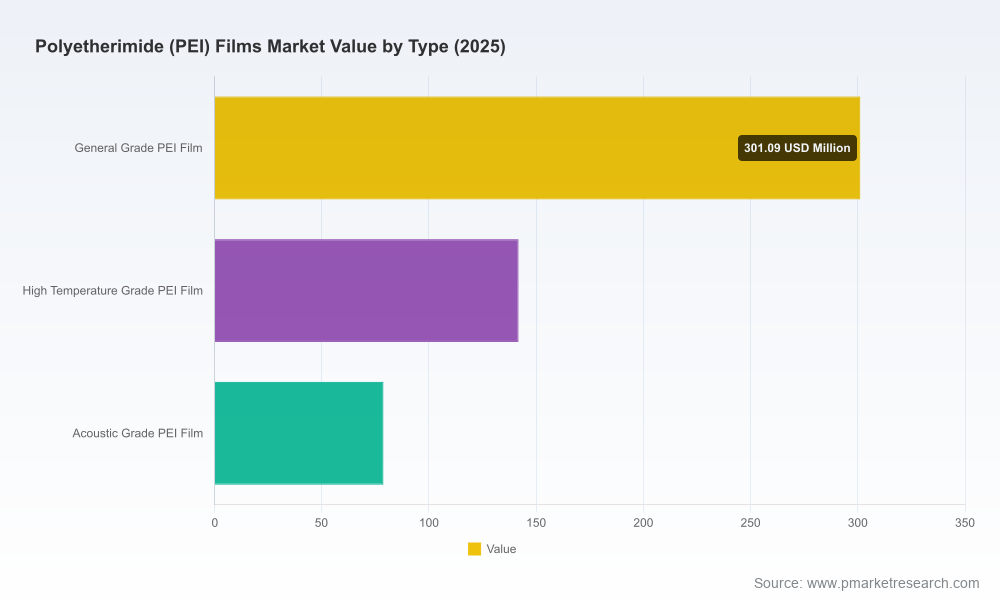

PW Consulting’s latest market study on Worldwide Polyetherimide (PEI) Films synthesizes five years of historical performance and a seven-year forecast horizon to deliver a practical playbook for boards, investment committees, and commercial leaders preparing budgets and strategic plans for 2026. The global PEI films market expanded from USD 382.45 Million in 2020 to USD 521.5 Million in 2025, and our baseline projection anticipates continued expansion to USD 843.66 Million by 2032, reflecting a compound annual growth rate (CAGR) of 7.12% across the forecast period. This trajectory underscores both the resilience and the structural revaluation happening across applications that rely on PEI’s unique combination of heat resistance, mechanical performance, and regulatory compliance.

Worldwide Polyetherimide (PEI) Films Market

Several converging forces make 2026 a decision point for manufacturers, OEMs, and materials buyers. First, demand vectors that favor high-performance polymers—miniaturized electronics, electrified powertrains, aerospace modernization, and medical device complexity—are maturing simultaneously. Second, regulatory and certification dynamics continue to ratchet product specifications upward: certain PEI grades can meet UL 94 V-0 ratings at remarkably thin gauge levels and comply with stringent migration restrictions relevant to food-contact and healthcare use. Third, input-cost volatility is real and actionable—m-Phenylene diamine (MPDA), a critical monomer for PEI synthesis, experienced a notable price uptick in 2024 in Asia driven by feedstock tightness, and this type of raw-material pressure can compress margins or accelerate supplier consolidation if left unaddressed.

Worldwide Polyetherimide (PEI) Films Market

For executives evaluating portfolio choices, 2026 represents the inflection where supply-chain resilience, product differentiation, and regulatory readiness transition from “nice-to-have” to “must-have.” The numbers in this report provide a quantified backdrop: after a steady recovery through 2025, our forecasted mid-single-digit-plus CAGR implies meaningful incremental market value—value that will accrue unevenly to players that align product, process, and go-to-market strategies to emerging customer willingness to pay for performance and compliance.

Worldwide Polyetherimide (PEI) Films Market

The report is designed as a working document. While this press release highlights major themes and headline market growth, the report itself contains the granular tables, supplier-level demand estimates, and downloadable models required to operationalize decisions—and those core segmentation tables are accessible on the report page for licensed clients.

The PEI films market exhibits a concentrated structure: the top three players account for a material majority of market share, and the top five increase that concentration further. This profile creates both barriers and opportunities. Market concentration implies pricing discipline for leading suppliers and a clear premium for advanced or certified grades. At the same time, it leaves space at the margins for specialized players that can deliver custom compounding, short-run flexibility, or differentiated service models.

Three archetypal supplier profiles are especially instructive for 2026 strategy:

For incumbents, the strategic choices are clear: invest in certification pathways, secure feedstock and intermediate supplies through long-term agreements or backward integration, and maintain R&D focused on thinner gauges and multifunctional grades. For challengers, options include focus-play strategies (e.g., acoustic-grade or high-temperature specialty films), regional service differentiation, or platform partnerships with chemical integrators and OEMs.

Leaders should use this study as a prioritized action plan rather than a passive reference. Tactical uses include: informing capital allocation (capacity vs. automation), defining procurement hedging strategies, setting R&D roadmaps tied to target applications, and establishing M&A screening criteria (e.g., capability gaps, regional coverage, or supplier consolidation targets). The report’s scenario suite also supports short-listing suppliers under multiple market stress cases and helps commercial teams build segmented value propositions for OEM accounts.

PW Consulting’s forecast and tools were developed with a focus on usability: licensed clients receive exportable models, supplier scorecards, and a regulatory checklist framed against realistic timelines. That means teams can plug the outputs directly into financial planning models, supplier scorecards, and procurement RFIs.

PEI films remain a high-value niche within the broader polymers landscape. The market’s steady compound growth through 2032 reflects a balance of demand strength in high-performance end-uses and manageable supply-side concentration. For 2026 planning, the strategic priorities are clear: secure feedstock resilience, invest in certification and thin-gauge capabilities where margin is available, and pursue targeted partnerships or acquisitions to close capability gaps.

For executives seeking to convert these insights into executable plans, PW Consulting’s full report contains the detailed segmentation tables, company-level demand models, supplier heatmaps, and scenario outputs that power board-level decisions. Visit the PW Consulting report page to license the complete dataset and modelling tools and access our team’s bespoke advisory services to accelerate your 2026 strategy.

For detailed analysis of this topic, please visit the official page:Worldwide Polyetherimide (PEI) Films Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com