What Keeps the Statin Market at the Center of Cardiovascular Disease Management?

Networking |

2026-07-02 09:47:48

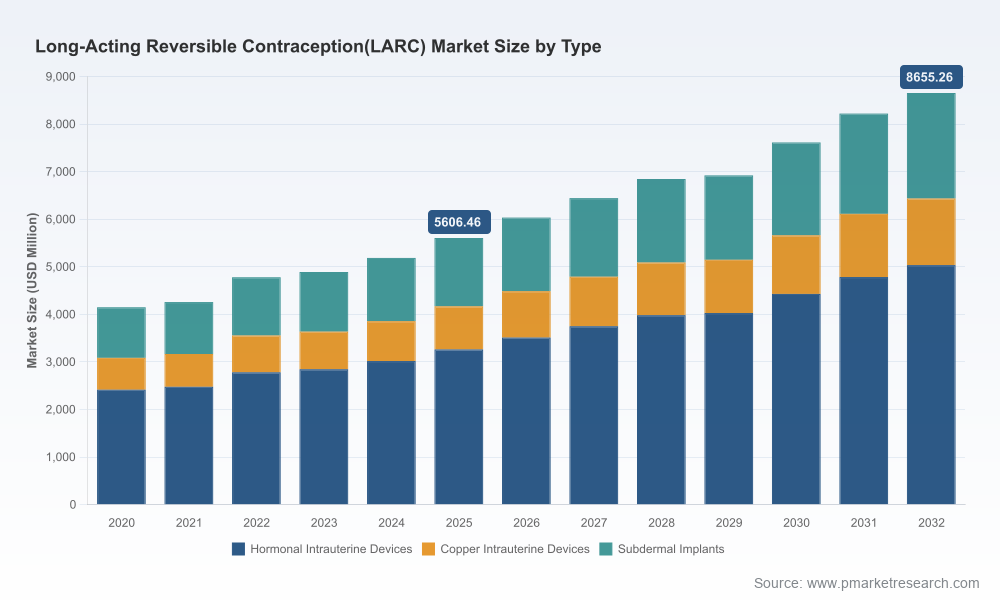

PW Consulting’s latest Worldwide Long-Acting Reversible Contraception (LARC) Market study, anchored on a 2025 base year and projecting through 2032, delivers a forward-looking playbook for executives navigating a market characterized by steady expansion, concentrated competition, and rapid product- and policy-level change. The global LARC market is expanding at a mid-single-digit compound annual growth rate (CAGR) of 6.4%—a structural growth trajectory that translates into meaningful scale for incumbents and new entrants alike. For 2026 corporate planning cycles, this study provides layered scenario analyses, regulatory and reimbursement intelligence, and actionable commercial playbooks aimed at converting market momentum into durable advantage.

Worldwide Long-Acting Reversible Contraception(LARC) Market

Extension and expiry dynamics: Key product lifecycle events—supplemental approvals extending labeled duration of use, and staggered patent expirations—are reshaping competitive moats in implants and intrauterine devices (IUDs). These transitions create windows for price, distribution and training disruptions that demand pre-emptive strategy.

Worldwide Long-Acting Reversible Contraception(LARC) Market

Reimbursement and cost-per-outcome economics: Health systems and payers are increasingly favoring LARC methods because of their high efficacy and lower long-term average cost compared with short-acting contraceptives. This creates pathways to broaden public and private reimbursement, but also invites tender-based competition.

Worldwide Long-Acting Reversible Contraception(LARC) Market

Product innovation meets procurement pragmatism: Innovations such as lower-copper-load, flexible-frame copper IUDs and extended-duration implants are changing the product-value equation—while established public-sector supply chains and WHO-prequalified manufacturers continue to exert pricing pressure and influence adoption in emerging markets.

Our analysis quantifies a clear and durable market uptrend: a mid-single-digit CAGR across the 2026–2032 forecast horizon that lifts the global market from its 2025 base to materially higher scale by the end of the projection period. This is not episodic growth—drivers include broader public-health adoption, improving clinician capacity for insertion and removal procedures, and product life-cycle extensions that increase cumulative device-years per unit sold. At the same time, the market’s concentration profile—where the top three and top five players collectively command a substantial majority of revenue—creates asymmetry: scale benefits incumbents, but targeted innovation and channel strategies can still deliver disproportionate returns for challengers.

Regulatory and clinical practice requirements: Clinician training programs and, in some jurisdictions, REMS-like requirements for implants create a two-edged sword. They raise barriers to rapid adoption of new devices but also produce stickiness for manufacturers that invest early in training infrastructure and provider certification programs.

Patent cliffs and extension opportunities: Upcoming expirations of core implant patents create opportunities for generic entrants and alternative delivery systems; concurrently, extended applicator or formulation patents can preserve differentiation for incumbents. Companies should model three scenarios—accelerated generic entry, staggered entry due to secondary patents, and proactive lifecycle management—to stress-test commercial forecasts.

Raw material and design innovation: Copper remains the active agent in non-hormonal IUDs, but innovation on copper load and delivery geometry (e.g., flexible frames) can materially change insertion profiles, side-effect perceptions and acceptance rates. These design decisions, while not costly individually, can influence procurement specifications and clinician preference at scale.

Public-sector supply and affordability: WHO-prequalified manufacturers and government-owned suppliers continue to anchor affordability programs. For commercial players, hybrid models—combining volume-based pricing for public tenders with premium branded offerings for private channels—are necessary to protect margin while accessing scale.

The LARC market displays high concentration, with a few large multispecialty and women’s health-focused firms shaping both innovation and go-to-market norms. Our competitive review identifies differentiated strategic postures among leading players—from lifecycle-extension and licensing deals to nonprofit partnerships and low-cost manufacturing partnerships—each with distinct implications for 2026 initiatives.

Organon & Co. has pursued both lifecycle extension and portfolio breadth through recent approvals and licensing agreements. Regulatory approvals extending implant duration and an exclusive global licensing deal for a next-generation copper IUD signal a dual strategy: defend implant leadership while expanding into hormone-free IUDs via licensing.

Bayer AG remains strategically focused on hormonal IUDs, advancing long-duration label claims and late-stage clinical work to preserve premium positioning. Expect ongoing investment in evidence generation to support extended-duration claims and indications expansion.

CooperSurgical continues to leverage its hormone-free copper IUD franchise in markets where a non-hormonal option is clinically preferred; its position underscores the enduring commercial value of a hormone-free alternative.

AbbVie (and collaborative models) utilizes public–private and nonprofit collaborations to advance affordability and access—strategically important where payer mix and procurement dynamics favor low-priced bulk supply without zeroing out brand equity in commercial channels.

Smaller and regionally focused manufacturers—including several WHO-prequalified producers—are critical supply nodes in public programs and emerging markets. Their role in price-setting and supply security is underappreciated in many commercial forecasts but central to execution risk in global expansion plans.

Supplemental approvals extending implant duration of use materially increase the effective lifetime value per device and change unit-demand dynamics for implants.

Licensing and approval of next-generation, lower-copper-load copper IUDs may shift clinician preference and procurement criteria, particularly where side-effect profiles and insertion simplicity are buying considerations.

Patent expirations and applicator patent timelines require playbooks that combine intellectual property monitoring, manufacturing readiness for potential generic competitors, and differentiated services (training, digital tools) to preserve share and margin.

Our report is built for decision-makers needing executable insight in 2026. Highlights include:

Demand modeling calibrated by device-year economics and clinician capacity, with scenario levers for patent timing, reimbursement shifts, and supply disruptions.

Commercial playbooks for incumbents, challengers and contract manufacturers—covering pricing, tendering, channel segmentation, and provider engagement strategies tailored to short-, medium- and long-term horizons.

Regulatory and reimbursement intelligence—detailing training requirements, label-extension pathways, and payer evidence thresholds necessary to unlock formulary and public-program adoption.

Manufacturing and supply-chain risk matrices that pinpoint exposure to raw-material volatility, single-source components, and public-sector procurement cycles.

Partnering and M&A opportunity maps that integrate clinical, IP and distribution footprints to reveal where bolt-on acquisitions or licensing deals can accelerate market entry or defend against erosion.

Prioritize evidence generation that targets both extension-of-use claims and real-world outcomes; the incremental clinical data to support longer-duration labeling is high ROI in terms of lifetime revenue per device.

Invest in provider training ecosystems—digital, in-person and certification-based—to convert regulatory requirements into a competitive advantage and a commercial barrier to entry for lower-cost competitors.

Adopt a dual-channel pricing strategy: protect margins in premium private markets while competing aggressively in price-sensitive public tenders via strategic licensing or contract manufacturing arrangements.

Model IP scenarios explicitly in 2026 budgets. Prepare contingency plans for earlier-than-expected generic entry and identify non-product revenue streams (training, consumables, digital adherence tools) that are less exposed to substitution.

Use supply diversification as a strategic lever—secure alternate suppliers for critical components and consider partnerships with WHO-prequalified manufacturers to support access commitments without ceding commercial share.

Leaders using this PW Consulting study will be able to translate macro growth into specific 2026 initiatives—product investments, go-to-market restructures, and M&A prioritization—with scenarios tied to measurable commercial outcomes. The study’s combination of market-scale projection, concentration analytics, regulatory timing, and company-level strategic profiles creates a single reference point for board-level debates and resource-allocation decisions during a year when product lifecycles and policy shifts converge.

PW Consulting’s full report contains the detailed forecasts, scenario models, country-level risk matrices and commercial templates referenced above. For market participants preparing budgets, M&A screens, or launch plans in 2026, the report is designed to be operational the day after delivery. To access the complete dataset, segment-level forecasts, and downloadable strategy templates, visit our report landing page or contact your PW Consulting account representative.

— PW Consulting, Global Health Practice

For detailed analysis of this topic, please visit the official page:Worldwide Long-Acting Reversible Contraception(LARC) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com