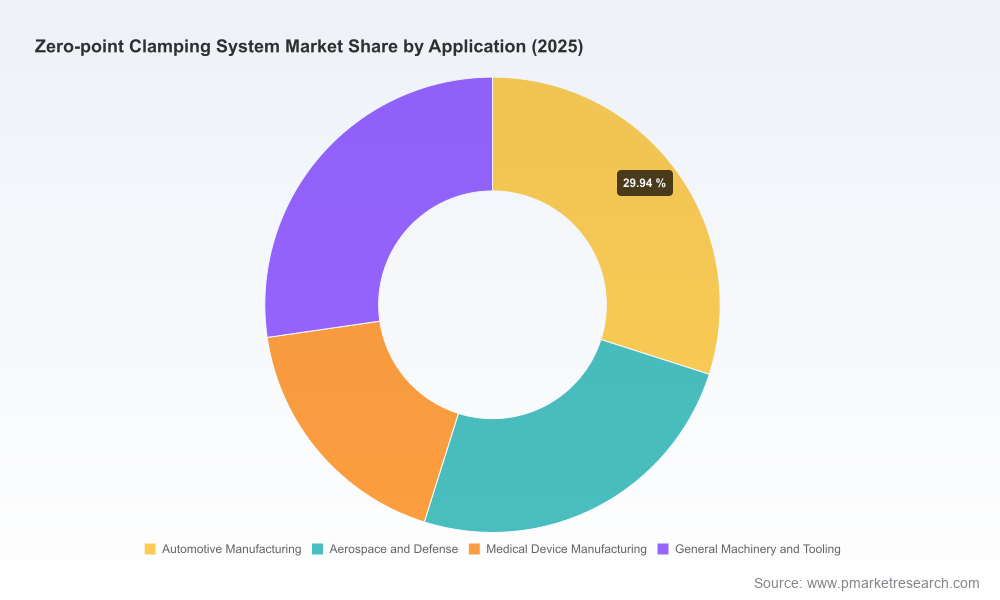

Worldwide Zero-point Clamping System Market: Strategic Preview for 2026 Decision-Makers

PW Consulting’s latest market intelligence brief — the Worldwide Zero-point Clamping System Market report (base year 2025, forecast 2026–2032) — synthesizes five years of historical performance with forward-looking scenario analysis to equip manufacturers, OEMs, automation integrators, and strategic investors for decisions to be made in 2026. This briefing summarizes the report’s strategic value and how executive teams should prioritize investments, supplier strategies, and product roadmaps in response to an industry that is stabilizing into steady, mid-single-digit growth while rapidly industrializing around automation and modular workholding.

Worldwide Zero-point Clamping System Market

Market trajectory at a glance

The market shows a clear recovery and disciplined growth profile: after consistent expansion through 2020–2025, the global market reached a meaningful inflection point in 2025 (base year), and our 2026–2032 projection is underpinned by a 6.55% compound annual growth rate. The market’s long-term outlook reaches into the high hundreds of millions (USD) by the end of the forecast window, reflecting ongoing automation adoption, retrofit cycles in existing machine fleets, and new-build OEM integration for lights-out production.

Worldwide Zero-point Clamping System Market

Why this matters for 2026 corporate decisions

- Capital allocation and CapEx timing: With predictable mid-single-digit growth, capital investments in workholding can be staged to coincide with machine tool upgrades, enabling better ROI profiles than one-off retrofit spending.

- Automation and lights-out enablement: Zero-point systems increasingly serve as the standardized interface for robotic and unmanned cells. Procurement strategies that prioritize standardized, automation-ready platforms materially shorten integration timelines.

- Supplier selection and risk management: The supplier landscape is moderately consolidated. Concentration metrics indicate that a small cohort of suppliers capture a meaningful share of market value — an important factor for supply continuity, pricing resilience, and strategic partnerships.

- Product and service roadmaps: High-mix, low-volume manufacturers are accelerating adoption to reduce setup times and increase machine utilization; firms that align product development to modularity, repeatability, and integrated actuation options capture commercial advantage.

- M&A and partnership targeting: Given the market structure and technology clustering, targeted acquisitions or alliances — particularly for automation, fixturing ecosystems, and IP around ultra-high repeatability — can be value-accretive in 2026.

What the full report delivers (operational, decision-ready content)

PW Consulting’s report is built as a practitioner’s playbook, not a high-level survey. Executives will find:

Worldwide Zero-point Clamping System Market

- Validated historical market sizing (2020–2025) and an itemized projection model for 2026–2032 that supports sensitivity testing across macro scenarios.

- Actionable vendor scorecards, benchmarking mechanical/hydraulic/pneumatic architectures, and a matrix comparing key performance indicators such as setup-time reduction potential, repeatability, and thermal behavior.

- Total cost of ownership templates (CapEx/Opex) and payback calculators tailored to retrofit versus greenfield machine purchases.

- Integration playbooks for automation integrators and factory engineers — covering electrical, pneumatic, and mechanical interfaces, handling, and quick-change workflows for lights-out cells.

- Supply resilience and procurement tools: supplier grading, dual-sourcing scenarios, and contingency playbooks for critical components.

- Patent and technology landscape mapping to identify adjacent capabilities (e.g., integrated rotary-table implementations, sealed modules for harsh environments).

- Prioritized implementation roadmaps and pilot designs sized for small-series manufacturers versus high-volume OEMs.

Competitive landscape — who matters and why

The market’s competitive dynamic is defined by established European specialists, precision-engineering houses from Switzerland and Germany, international integrators, and a growing cohort of Asia-based suppliers. Rather than a pure commodity market, zero-point clamping remains technology- and system-driven; leadership is tied to modularity, precision, automation readiness, and ecosystem support.

- STARK Spannsysteme GmbH (ROEMHELD Group) — a long-time pioneer whose systems are often positioned where setup-time optimization across milling, turning and automation is mission-critical.

- LANG Technik GmbH — known for modular grid solutions and strong retrofit appeal across established machine fleets, a pragmatic choice for minimizing downtime in mixed-machine shops.

- Zimmer Group — emphasizes application-specific configurations and error reduction across a wide range of processes, supporting specialized use-cases including grinding and EDM.

- HAINBUCH GmbH — offers form-fit clamping optimized for stationary applications and rapid changeovers, well-suited to shops looking for fast, repeatable fixturing.

- SMW-AUTOBLOK — known for high-clamping-force modules and sealed designs suited to harsh cutting environments and where robust pull-down forces matter.

- EROWA AG — a specialist in automation-ready platforms tailored for lights-out production; integration with loading units is a key differentiator.

- AMF Andreas Maier GmbH & Co. KG — offers breadth across actuation technologies and recently updated catalogs that reflect design-for-manufacturing insights relevant to 2026 procurements.

- ZeroClamp GmbH — positions its platform as an alternative to traditional T-slots with claims of ultra-low repeatability and thermal symmetry, attractive for precision toolrooms.

- NIKKEN Kosakusho Works Ltd. (Lyndex-Nikken) — integrates zero-point interfaces into rotary solutions to preserve machine rigidity; a notable option for 5-axis setups.

- SCHUNK GmbH & Co. KG — recognized for industrial-grade systems widely adopted in automation-heavy operations.

- Jergens Inc. — U.S.-based player promoting dramatic setup-time reductions, often favored in North American retrofit projects.

- Gressel AG — active in product evolution with module launches and iterative plate improvements relevant to 2025–2026 purchasing cycles.

- Suzhou SET Industrial Equipment System Co., Ltd. — represents China-based precision alternatives with competitive repeatability specifications and custom solutions for regional supply chains.

Recent developments that shape the 2026 landscape

- Product refreshes and new plate modules introduced in 2025 highlight a supplier focus on modularity and retrofittability.

- Leading vendors showcased at the major trade fair cycle in late 2025, signaling renewed emphasis on integration with additive and high-temperature processes.

- Catalog and product updates released in 2024–2025 reflect suppliers’ efforts to broaden actuation options — mechanical, hydraulic, and pneumatic — responding to diverse user needs.

- Examples of integrated rotary-table clamping highlight a trend toward embedding zero-point function into machine axes to preserve rigidity and reduce stack height.

Strategic implications and a six-point action plan for 2026

For executives preparing budgets and strategic initiatives in 2026, the PW Consulting report drives a focused set of actions:

- Run prioritized pilots: Define two pilot deployments — one retrofit and one greenfield — to validate ROI and integration timelines under your shop-floor conditions.

- Formalize interface standards: Standardize on mechanical/electrical/pneumatic interfaces across your fleet to reduce customization costs and accelerate automation integration.

- Use procurement scorecards: Adopt multi-criteria supplier scorecards (technical fit, automation readiness, lead time resilience, aftermarket support) to select preferred partners.

- Stage CapEx with modularity in mind: Favor modular systems that can be scaled or upgraded to extend useful life and protect against obsolescence.

- Mitigate supply risk: Develop dual-sourcing pathways for critical modules and components, and map second-tier suppliers in regions aligned with your supply-chain risk appetite.

- Monitor M&A and tech licensing: Keep watch lists for specialist providers whose IP or automation integration capabilities complement your roadmap; build partnership-first outreach plans.

How PW Consulting helps

Our full report delivers the data models, vendor scorecards, supply-risk matrices, and implementation playbooks that operational teams need to convert strategy into action. For procurement teams we provide RFP templates and TCO calculators; for engineering teams we provide integration checklists and pilot design guides; for corporate development teams we supply M&A screening criteria and technology-fit assessments. The published report intentionally omits the granular segment-by-region breakouts in this preview to preserve the actionable intelligence for subscribers.

To access the complete analysis, granular segment modeling, and the practitioner tools referenced above, please consult the full report on the PW Consulting report page. The complete dataset and appendices include downloadable models (Excel), vendor appendix with recent development logs, and step-by-step implementation templates to convert insight into measurable 2026 outcomes.

PW Consulting — translating machinery-market intelligence into decision-ready action.

For detailed analysis of this topic, please visit the official page:Worldwide Zero-point Clamping System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com