What Is Driving Demand in Automotive Dynamic Spotlight Market for Smart Lighting?

Networking |

2026-05-07 10:54:51

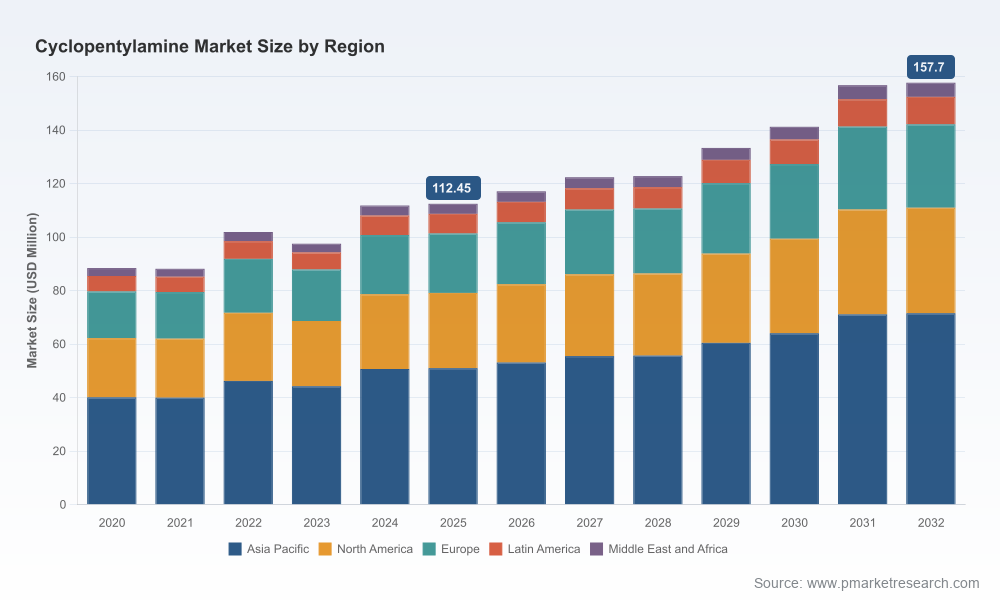

PW Consulting’s latest market study on Cyclopentylamine provides a commercially focused, board-level briefing tailored for 2026 strategic planning. Our analysis synthesizes historical performance (2020–2025) and a detailed forecast through 2032 to deliver decision-grade intelligence. The market, having grown from a subdued base early in the decade, registered an estimated USD 112.45 Million in 2025 and is modeled to expand at a compound annual growth rate (CAGR) of approximately 4.95% over the 2026–2032 forecast horizon, reaching roughly USD 157.7 Million by 2032. These headline metrics frame a market characterized by moderate growth, pockets of premium demand, and an upstream feedstock dynamic that can materially affect margin profiles across the value chain.

Worldwide Cyclopentylamine Market

Actionable foresight for CAPEX and capacity decisions: our supply-demand modelling identifies timing windows where incremental capacity or plant upgrades yield the highest ROI relative to anticipated demand upticks in pharma and specialty applications.

Worldwide Cyclopentylamine Market

Procurement and raw-material hedging: granular scenario work on cyclopentanone price trajectories and availability equips procurement teams to design resilient sourcing and pricing strategies.

Worldwide Cyclopentylamine Market

Regulatory preparedness: the report translates evolving safety and environmental controls into practical compliance roadmaps, crucial for firms expanding into regulated geographies in 2026.

M&A and partnership prioritization: a curated shortlist of value-accretive targets and entry strategies for companies seeking concentration or geographic diversification.

Our historical review captures volatility and recovery phases from 2020 through 2025, with the 2024–2025 period showing renewed stability as end-use demand in pharmaceutical intermediates and specialty chemicals firmed. The baseline market size in 2025 provides a dependable reference for scenario planning. From that base, the 2026–2032 forecast reflects steady compound growth driven by sustained demand in high-purity segments, incremental adoption across agrochemical applications, and continued use in rubber processing and other niche sectors.

The growth path is not uniform: while volume-based opportunities exist in lower-cost supply corridors, long-term margin expansion will favor suppliers who can deliver consistent high-purity product, regulatory documentation, and reliable supply chains. Concentration metrics indicate a market where the top three and top five suppliers command meaningful shares, but not dominance—leaving room for mid-sized specialists and new entrants to carve differentiated positions.

End-market resilience in pharmaceuticals: demand for Cyclopentylamine as an intermediate for API and specialty molecular synthesis remains the chief demand pillar. Quality, traceability and regulatory documentation are decisive procurement criteria for upstream buyers.

Agrochemical cycles and formulation shifts: demand linked to crop protection innovation and seasonality creates discrete procurement windows and price elasticity that savvy suppliers can monetize via contract structures.

Upstream feedstock dynamics: cyclopentanone is the primary upstream feedstock. Regional oversupply in late 2024 led to a measurable price softening in China, and through 2025 prices across major markets trended stable to slightly declining due to broader petrochemical feedstock softness. These movements materially affect margin sensitivity—producers with feedstock integration or long-term offtake agreements will have a competitive edge.

Regulatory and environmental constraints: Cyclopentylamine falls under EU REACH requirements with specific environmental exposure control expectations, and is subject to standard US EPA/FDA handling and documentation practices. Compliance costs and the need for environmental risk mitigation are non-trivial and must be priced into bids and capital plans.

The market is populated by a mix of global reagent houses, contract manufacturers, and regional bulk producers. Our competitive heatmap categorizes suppliers by capability, scale, and market reach, highlighting strategic differentiators.

Global reagent and specialty players (example: Sigma-Aldrich / Merck KGaA) — Positioning: premium high-purity reagent suppliers with strong brand-recognition in research and pharma. Strategic advantage derives from certified quality grades, global distribution networks, and integrated documentation packages attractive to regulated end-users. These players are defensible on specification, service and compliance rather than price alone.

R&D and multi-channel distributors (example: Biosynth Ltd) — Positioning: flexible suppliers able to serve both discovery-stage and production-scale needs with hazardous material handling and global logistics. Their value proposition is responsiveness and tailored service; in 2026, strategic partnerships with contract manufacturers and co-development clauses will be a growth lever.

China-based bulk manufacturers (examples: TNJ Chemical, Volant-Chem) — Positioning: cost-competitive producers with significant bulk capacity and certifications (e.g., ISO 9001). Their strategic options in 2026 include capacity rationalization to protect margins, backward integration into cyclopentanone, and targeted certification upgrades to access higher-margin pharmaceutical intermediate markets.

Specialized US suppliers (example: Broadpharm) — Positioning: regional service and speed-to-market for North American chemical and pharma sectors. Their strengths include local inventory, regulatory support for domestic manufacturers, and rapid-response supply chains—attributes of high strategic value in tight-timeline projects.

Collectively, market concentration figures show that the leading three and five firms hold a material but non-monopolistic share of the market, leaving strategic space for focused specialists and agile new entrants to grow through service, quality, or cost differentiation.

Regulatory oversight—especially under REACH and comparable frameworks—creates both compliance costs and market opportunities. Suppliers that invest early in environmental risk management, effluent controls, and exhaustive safety data will gain privileged access to regulated supply chains. For buyers, contract clauses that transfer compliance risk and require supplier transparency are now standard negotiating levers.

On sustainability, lifecycle assessments that quantify upstream feedstock impacts and propose mitigation levers (feedstock substitution, solvent recovery, energy-efficiency programs) are increasingly requested by tier-one pharmaceutical and agrochemical corporates. 2026 decision calendars should account for modest near-term costs associated with these initiatives and larger reputational benefits thereafter.

Supply Chain & Procurement: lock in multi-year contracts with volume flexibility, institute feedstock price pass-through clauses, and expand dual-sourcing from geographically diverse suppliers to reduce concentration risk.

Manufacturing & Operations: evaluate brownfield upgrades for impurity control and invest selectively in analytics to meet higher purity tolerances demanded by pharmaceutical intermediates.

Commercial & Sales: segment customers by regulatory sensitivity and willingness-to-pay; create tiered offerings (standard vs. certified high-purity product) with differentiated lead times and service levels.

Corporate Development: prioritize acquisition targets that deliver feedstock integration, certificate-of-analysis depth, or regional distribution networks, and model integration synergies under conservative price scenarios.

R&D and Product Management: collaborate with key customers to co-develop formulations that reduce solvent use or enable lower-cost downstream processing, creating sticky revenue streams.

The PW Consulting study is designed as a practical playbook, not a high-level summary. Key deliverables include:

A detailed demand model by end-use category and scenario-based forecasts through 2032;

Supply mapping and capacity utilization analysis, including plant-level intelligence and certification status;

Price and margin sensitivity models tied to cyclopentanone feedstock trajectories and alternative sourcing scenarios;

Regulatory & environmental compliance checklists and cost impact estimates for major markets;

A competitive playbook with capability matrices for leading suppliers and recommended commercial countermeasures;

M&A screening framework and prioritized target profiles with indicative valuation sensitivities;

Primary interview excerpts and supplier scorecards that inform negotiation and partnership strategies.

Our findings rest on a hybrid methodology: primary interviews with supply-chain participants, proprietary shipment and inventory models, price series for key feedstocks, and regulatory impact assessments. We apply sensitivity analysis across three demand scenarios and stress-test margins under feedstock price volatility. Where public disclosure is constrained, our intelligence is validated by cross-referencing independent industry sources and supplier-level documentation.

For 2026 planning cycles, executives should use this report to: prioritize investments that secure high-purity supply; renegotiate supplier agreements with explicit compliance and volatility clauses; and re-evaluate go-to-market strategies that capture higher-margin specialty demand.

PW Consulting’s study intentionally highlights core strategic vectors while reserving detailed segment-level splits and proprietary supplier-level metrics for the full report. These detailed tables and scenario models are accessible via our report page and are essential for granular budgeting, contract drafting, and M&A diligence.

To obtain the full Worldwide Cyclopentylamine Market report, including comprehensive regional and application splits, supplier scorecards and our interactive forecast models, please visit PW Consulting’s report page. The full dataset and appendices provide the granular evidence base required for executable 2026 strategies.

For detailed analysis of this topic, please visit the official page:Worldwide Cyclopentylamine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com