Fruit Processing Market Forecast: Sustainability and Eco-Friendly Packaging

Food |

2026-02-26 12:04:01

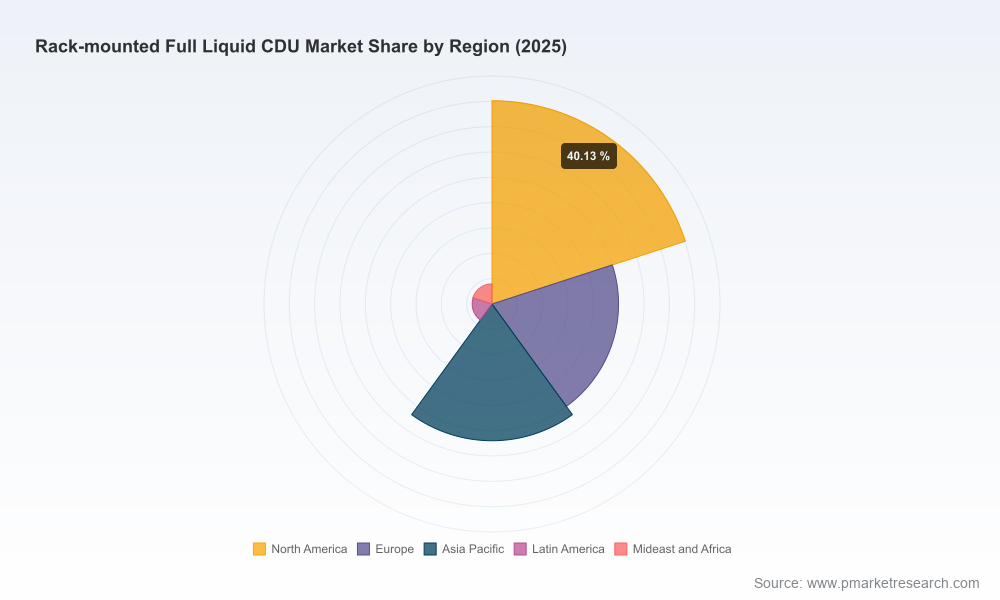

PW Consulting today publishes an executive-level industry briefing accompanying our full Rack-mounted Full Liquid Coolant Distribution Unit (CDU) Market report. Grounded in a 2025 base-year assessment and a detailed 2026–2032 forecast horizon, the briefing distills the commercial dynamics that will materially affect capital planning, sourcing strategies, and operational roadmaps for data-center owners, hyperscalers, colocation operators, and chip-to-rack solution integrators in 2026. Our core quantitative signal: the market—measured on a USD million revenue basis—more than doubles during the forecast window, with a compound annual growth rate of 9.85% underpinning a rapid shift from niche pilots to mainstream rack-level thermal platforms.

Rack-mounted Full Liquid CDU Market

AI and high-performance computing architectures are compressing IT power density and shifting thermal management from building-scale to rack- and chip-level solutions. Enterprises renewing refresh cycles in 2026 must treat CDU selection as a strategic infrastructure decision, not a commodity mechanical purchase.

Rack-mounted Full Liquid CDU Market

Regulatory and standards updates are reducing ambiguity but increasing compliance demands. Guidance from technical committees is raising the bar on isolation, testing methodology, and performance validation—requirements that will be material to procurement, warranty negotiation, and long-term serviceability.

Rack-mounted Full Liquid CDU Market

Supply-chain and input-cost pressures—driven in part by global refrigerant policy changes—are altering product TCO assumptions. Lifecycle costing, including certification and end-of-life handling, must now be modeled alongside CapEx to avoid mid-life margin erosion on hosted infrastructure.

Product innovation is accelerating. Vendors are moving from single-unit offerings to modular, rack-scalable CDU platforms designed for phased deployment across hybrid estates, enabling new financing, deployment, and reliability constructs.

Actionable forecast and sizing models calibrated to 2020–2025 historic performance and refreshed for a 2026–2032 outlook. These models are designed for integration into capital planning spreadsheets and include sensitivity scenarios for power-density trajectories and different cooling architectures.

Vendor scorecards and procurement matrices built from capability, service-model, integration, and risk criteria. Each profile evaluates channel maturity, systems engineering support, warranty design, spare-parts strategy, and cross-supplier interoperability—inputs that directly inform supplier shortlists and RFP scoring.

Deployment playbooks and trial-to-scale templates that reduce onboarding risk: mechanical/piping checklists, commissioning acceptance tests aligned with emerging test standards, and operational KPIs to track coolant quality, pump efficiency, and fault-domain isolation.

TCO and lifecycle calculators that incorporate upfront hardware, integration labor, certification costs, refrigerant and coolant handling, energy performance, and scheduled maintenance—enabling procurement and finance teams to compare liquid strategies against air-cooled baselines on consistent terms.

Design decision frameworks that map architecture choices (in‑rack vs. in‑row, liquid-to-liquid vs. liquid-to-air approaches) to use cases and rollout cadence, preserving optionality for future server refreshes and AI scaling.

The market is evolving from a collection of specialist suppliers to a competitive ecosystem that includes established IT OEMs, systems integrators, and niche liquid-cooling innovators. Our qualitative benchmarking identifies three distinct archetypes that buyers will encounter:

Specialist liquid-cooling innovators: firms with deep thermal-engineering portfolios and productized, rack-oriented CDUs that prioritize high-density and narrow approach-temperature performance. These vendors excel at bespoke integration for AI/HPC workloads and typically offer close engineering support during proof-of-concept and commissioning stages.

Systems OEMs and scale suppliers: larger platform providers are bundling CDUs with compute and power distribution offerings, emphasizing modularity, supply-chain resilience, and enterprise-grade service contracts. Their value proposition centers on simplified procurement and integrated support across compute, power, and cooling stacks.

Components and infrastructure specialists: vendors focusing on reliability, redundancy, and coolant distribution subsystems—targeting customers that prefer to assemble multi-vendor stacks with standardized mechanical and controls interfaces.

Representative firms profiled in the report include long-standing innovators and new modular entrants. Each profile covers strategic focus, typical customer archetypes, channel and partnership models, engineering strengths, and go-to-market implications. Recent vendor movements underscore the competitive intensity:

An established electronics contract manufacturer introduced a modular rack-level CDU platform late last year, signaling a push to supply GPU-dense deployments with scalable, multi-unit solutions.

A major power-and-thermal product group announced a next-generation CDU platform early this year positioned at the higher end of density and scalability for AI production lines.

Server OEMs continue promotional activity around integrated rack CDUs targeting dense HPC and AI racks, expanding the range of integrated options available to procurement teams.

Standards bodies are tightening test and performance protocols. New test methods under consideration will make comparative performance claims more auditable but also increase verification costs for vendors. Buyers should require third-party test evidence aligned to these emerging methods as part of procurement evaluation.

Technical guidance emphasizes the operational imperative of isolating facility water systems from technology coolant circuits to uphold reliability and maintainability. This affects valve architecture, monitoring strategy, and run-to-failure contingency planning.

Global refrigerant phase-downs and evolving environmental compliance regimes are changing materials sourcing and certification timelines. Procurement must account for extended lead times on certified components and for incremental certification costs when comparing supplier proposals.

Integrate CDU selection into the platform strategy. Treat coolant distribution as part of the compute platform and involve facilities, IT, procurement, and service teams in vendor evaluation from day one to avoid costly field rework during refresh cycles.

Prioritize modularity and staged scalability. Given the market’s rapid growth trajectory, opt for CDU platforms that support phased addition of capacity and can be deployed incrementally across heterogeneous estates.

Insist on standards-aligned test evidence. As testing standards become formalized, require suppliers to provide performance validation and interoperability proofs that map to the new test methods and ASHRAE guidance.

Model TCO with regulatory and certification scenarios. Include alternative refrigerant pathways and extended warranty/service options in financial models to capture the full range of future obligations and costs.

Design pilot programs to resolve integration risk. Structured pilots that run to acceptance criteria—covering thermal performance, leakage containment, and operational maintenance—provide the most reliable path to scale with minimized service disruption.

Negotiate service-level architecture, not just hardware. Contracts that cover hardware, controls, spares provisioning, and remote diagnostics reduce long-term operational risk and improve MTTR in liquid-cooled environments.

The PW Consulting full market study is structured to serve both strategy teams and hands-on engineers: macro forecasts and scenario models for finance and strategy, plus engineering playbooks and procurement scorecards for operations and sourcing. The briefing you are reading is intended as a strategic primer; the full report contains the underlying datasets, supplier scorecards, programmable TCO models, and vendor-comparison matrices that enterprises use to finalize 2026 CapEx and procurement plans.

For teams preparing RFPs, planning multi-site rollouts, or evaluating CAPEX vs. service models, the report provides the empirical inputs and negotiation templates needed to compress decision cycles while preserving optionality as rack densities evolve.

As rack-mounted full liquid CDUs transition from experimental to foundational in modern data-center architectures, the decisions made in 2026 will set the operational and financial trajectory for the next refresh cycle. PW Consulting’s study offers both the high-level market signals—including the strong mid-term growth rate—and the field-proven tools that procurement, engineering, and finance teams require to translate those signals into executable plans. For readers seeking the full dataset, vendor benchmarking, and implementation templates referenced above, the comprehensive report and accompanying models are available through our official distribution channels.

For detailed analysis of this topic, please visit the official page:Rack-mounted Full Liquid CDU Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com