Soy Protein Ingredient Market to Witness Strong Expansion by 2036

Other |

2026-03-20 12:15:14

PW Consulting’s new Worldwide Ox Bezoars Market report (base year 2025; forecast 2026–2032) offers a concise, operational-grade briefing for corporate strategy, investment committees, and regulatory affairs teams preparing for decisions in 2026. The market has shown a sustained recovery and expansion since 2020, and our topline modeling points to continued momentum: the global market reached an estimated USD 1.29 billion in 2025 and is projected to exceed USD 2.35 billion by 2032 on a 2026–2032 compound annual growth rate (CAGR) of approximately 9.0%.

Worldwide Ox Bezoars (Cow Bezoars) Market

This release explains why that trajectory matters, what dynamics will influence commercial outcomes in 2026, and which practical actions market participants should prioritize now. The article deliberately highlights professional depth while withholding granular segment tables and proprietary breakdowns—those are available in the full report on our website.

Worldwide Ox Bezoars (Cow Bezoars) Market

Timing: 2026 is the inflection window where tactical investments (production scale, authentication labs, supplier contracts) translate into strategic advantage. The market transition from niche traditional-use product to a mixed-use commodity for research and specialty pharmaceuticals accelerates capital deployment and supplier rationalization.

Worldwide Ox Bezoars (Cow Bezoars) Market

Regulatory posture: Classification and access rules are tightening in major supply geographies, raising compliance costs and entry barriers for low-maturity players.

Value chain shifts: New sourcing technologies—particularly in-vitro cultivation and validated synthetic/alternative compounds—are moving from R&D into pilot-scale commercial production, reshaping supplier economics and margin pools.

Between 2020 and 2025 the market more than recovered from pandemic-era disruption, driven by stabilized supply chains and renewed demand across traditional medicine and research applications. Our topline trajectory shows growth from under USD 0.85 billion in 2020 to about USD 1.29 billion in 2025. With an expected CAGR of roughly 9.0% over 2026–2032, the market is projected to cross the USD 2.35 billion mark by 2032.

Two implications follow. First, absolute demand expansion creates space for new entrants that can meet certification and quality requirements. Second, growth is sufficiently robust to warrant dedicated supply-chain investments (traceability systems, captive cultivation facilities, and contract manufacturing scale-ups) for firms aiming to capture meaningful share.

China’s Pharmacopoeia classification: Ox bezoars are listed as materials for traditional Chinese medicine, which imposes authentication and quality-control expectations for pharmaceutical-grade use. Companies that invest early in validated QA/QC protocols reduce time-to-market risk for value-added product lines.

Western regulatory status: Ox bezoars are not approved as pharmaceuticals by regulators such as the US FDA or the EMA and currently circulate primarily as herbal supplements or traditional medicine ingredients. This regulatory reality shapes route-to-market strategies—purists seeking drug approval face a longer, more CAPEX-intensive runway than firms focused on high-grade supplements or contract research supply.

Export controls: International trade is influenced by wildlife and trade frameworks; exports of cattle-derived materials from key origins are regulated under CITES Appendix II-style regimes to prevent overexploitation. Compliance capability (permits, chain-of-custody documentation) becomes a commercial differentiator.

The market’s supplier landscape is best described as fragmented with emerging consolidation pockets. Our concentration analysis shows a modest concentration among top players—enough to put scale advantages in play but not so high as to exclude agile specialists. Practically, this yields three archetypal players:

Traditional aggregators and exporters: firms with long-standing field collection networks and trading relationships. Strengths: supply access and price flexibility. Weaknesses: variable quality controls and regulatory readiness.

Specialized cultivators and biotech entrants: operators commercializing in-vitro cultivated products and validated substitutes. Strengths: traceability, repeatability, and alignment with pharmaceutical standards. Weaknesses: higher upfront capex and scale-up risk.

Value-added processors and branded manufacturers: companies that perform authentication, fractionation, and formulation to serve TCM manufacturers and supplement brands. Strengths: formulation expertise and route-to-market. Weaknesses: exposure to raw-material price volatility.

Supply-side squeeze: surge in authenticated-commodity demand could create short-term shortages of pharmaceutical-grade material. Firms dependent on low-cost suppliers may face margin compression unless they secure contracted volumes or vertically integrate.

Regulatory shocks: reclassification, stricter export licensing, or new pharmacopoeial requirements could raise compliance costs materially. Scenario planning should include stress tests for permit-delays and batch rejections.

Reputation and authenticity risk: counterfeit or poorly authenticated materials threaten downstream manufacturers’ brands. Investing in third-party authentication or blockchain-enabled traceability can be a defensible moat.

Substitution risk: as in-vitro and synthetic analogs commercialize, price-sensitive segments will shift, creating divergent winners across premium vs. mass-market channels.

The full PW Consulting report is built for immediate use by corporate teams. It contains:

Topline market sizing (historical 2020–2025, base-year 2025) and demand-driven forecasts through 2032, with scenario vintages that model policy, supply and technology outcomes.

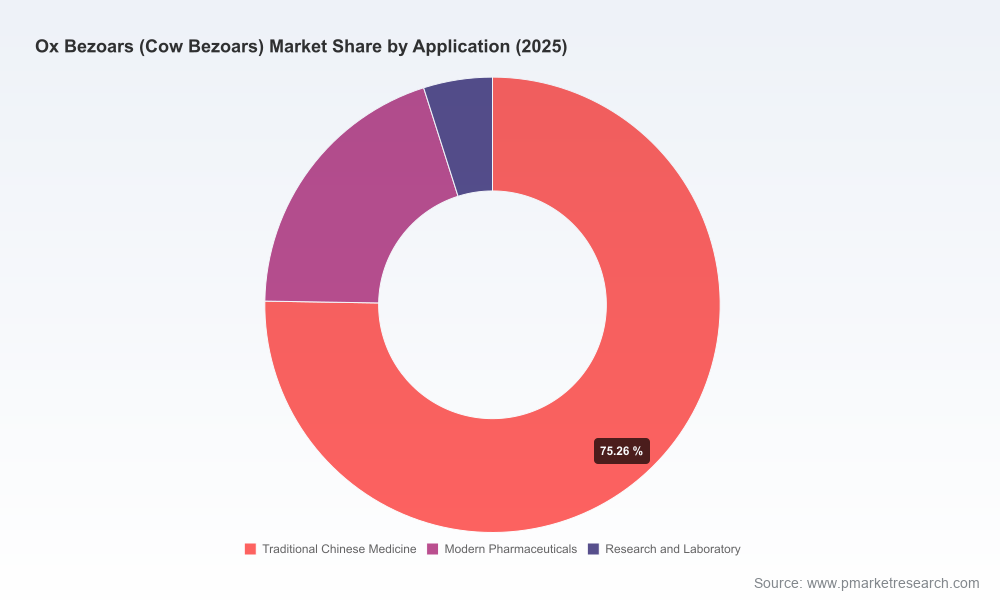

A segmentation framework (by type, application and region) and an explanations matrix that links demand drivers to supplier behaviors—segment-level numbers are reserved in the report to preserve competitive value.

Value-chain mapping and cost-to-serve templates, including an actionable supplier-selection scorecard and recommended KPIs for procurement and quality teams.

Regulatory playbook: checklist templates for export compliance, pharmacopoeial authentication, and steps to pursue regulatory pathways in Western markets should firms elect to pursue drug-approval strategies.

Commercial playbooks for five archetype companies (aggregators, cultivators, processors, formulators, and pure-play exporters), with recommended go-to-market moves and capex timing for 2026.

Operational stress tests and Monte Carlo scenarios to quantify financial impact of supply interruptions, price spikes, and regulatory delays on EBITDA and working capital.

Secure quality-focused supply: convert spot purchases into multi-year, quality-assured contracts with audit and traceability clauses. For buyers, prioritize suppliers that can demonstrate pharmacopoeial-aligned authentication.

Pilot cultivated alternatives: allocate a controlled R&D/scale-up budget to in-vitro cultivation pilots. Even if a firm does not commercialize an alternative, learning early reduces late-stage disruption risk.

Invest in authentication: deploy third-party chemical-fingerprinting and provenance systems across key SKUs; reduce brand exposure to counterfeit material.

Regulatory hedging: for companies considering pharmaceutical pathways, begin dialogue with regulators early and budget for extended clinical/analytical programs. For supplement-focused players, reinforce compliance with export and labeling laws.

M&A and JDAs: target acquisition of capacity (cultivation or processing) to secure margin capture; consider joint-development agreements with biotech providers to share scale-up risk.

Our methodology combines primary interviews with supply-chain operators, lab-validated authentication sampling, and a trade-level view of export permits to triangulate market trends. We overlay regulatory scenario modeling (including stricter pharmacopoeial requirements and export controls) with economic sensitivity analyses to deliver not only a forecast but also a prioritized actions list tied to P&L and working-capital outcomes.

We also quantify market concentration to contextualize competitive dynamics—our analysis shows a moderate concentration among the largest players, creating strategic space for both scale players and specialized innovators.

The 2026 decision window demands precision: which supply contracts to lock, where to allocate capex, and how to design compliance-proof commercialization pathways. PW Consulting’s Worldwide Ox Bezoars Market report translates high-level market signals into executable programs—pricing playbooks, supplier scorecards, regulatory checklists, and stress-tested financial scenarios. If your 2026 plan involves sourcing, manufacturing, investing in, or regulating ox bezoar-derived products, the full report is the practical briefing you need to move from hypothesis to action.

For access to the full dataset, segment-level insights, and downloadable operational templates, please visit the report page on PW Consulting’s website.

For detailed analysis of this topic, please visit the official page:Worldwide Ox Bezoars (Cow Bezoars) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com