Worldwide MRI Compatible IV Infusion Pumps Market — Strategic Outlook for 2026 Decision‑Makers

Executive summary: why this market matters in 2026

The market for MRI compatible IV infusion pumps is transitioning from a specialized clinical niche into a strategically important product class for hospital systems, diagnostic imaging centers, and advanced clinical networks. Our PW Consulting base‑year assessment (2025) values the worldwide market at approximately USD 465.0 Million (USD Million convention). Forecasting through 2032 at a compound annual growth rate (CAGR) of 8.6% yields a projected market size of roughly USD 828.4 Million by 2032, with a step‑function increase expected as next‑generation non‑magnetic technologies achieve broader regulatory clearances and institutional adoption.

Worldwide MRI Compatible IV Infusion Pumps Market

For executives making capital allocation, product road‑map, or M&A decisions in 2026, this is a market where technology specificity, regulatory posture, and procurement pathways converge to create outsized value for companies that can move quickly and credibly. Our new Worldwide MRI Compatible IV Infusion Pumps Market report — built on historical data from 2020–2025 and a detailed forecast through 2026–2032 — is designed to translate that opportunity into operational choices and concrete investment cases.

Worldwide MRI Compatible IV Infusion Pumps Market

What the report provides — practical, board‑ready intelligence

- Consolidated market sizing and trend decomposition (historical and forecast), including base‑year validation and scenario overlays to stress‑test demand under alternative adoption curves.

- Competitive intelligence dossiers: profiles, strategic positioning, product features, IP posture, regulatory milestones, and procurement signals for the leading suppliers in MRI‑compatible infusion therapy.

- Regulatory and procurement mapping: a curated timeline of relevant FDA actions, guidance implications, and public‑sector procurement behaviors that materially affect buying cycles and sole‑source justifications.

- Commercial playbooks: segmented go‑to‑market strategies, pricing sensitivity and reimbursement considerations, total cost of ownership (TCO) models, and service & spare‑parts economics tailored to hospital capital planning horizons.

- Transaction support: valuation frameworks, synergy matrices, and diligence checklists for M&A or JV activity focused on MRI‑safe infusion platforms and adjacent services.

- Decision support tools: downloadable Excel models for demand forecasting, payback analysis, and deployment sequencing aligned to typical 8‑year infusion pump lifecycles used in hospital capital planning.

Competitive landscape — what the market structure means for strategy

The MRI compatible infusion pump market is highly concentrated: the top three suppliers account for roughly 84.5% of industry revenue, and the top five account for over 92%. This concentration creates both barriers to entry and predictable vectors for consolidation or strategic partnership.

Worldwide MRI Compatible IV Infusion Pumps Market

Key industry participants include technology specialists and large infusion therapy platform providers. IRadimed Corporation has emerged as a focal point following its 510(k) clearance for a next‑generation non‑magnetic MRI infusion system (MRidium 3870) in May 2025 and subsequent procurement interest from large public health purchasers in 2026. Their product attributes — non‑magnetic ultrasonic motor drive, touchscreen UX, expanded drug library, and built‑in wireless remote control — illustrate the innovation trajectory buyers are rewarding.

Established infusion therapy companies, including major OEMs with broad hospital portfolios, are deploying different competitive plays. Some, like B. Braun, address MRI safety through integrated solutions that enable conventional infusion pumps to be used safely in controlled MRI environments; others — including Baxter, Fresenius Kabi, Becton Dickinson, ICU Medical/Smiths Medical, Arcomed, and Moog (Curlin) — are leveraging existing customer relationships, service networks, and product families to protect share while incrementally improving MRI compatibility and workflow integration.

Strategic implications:

- Incumbents with broad hospital footprints should prioritize product retrofits, service bundles, and procurement facilitation (e.g., training, MRI‑safe workflows) to defend share against specialist entrants.

- Pure‑play MRI specialists can monetize first‑mover regulatory advantages through targeted institutional pilots, clinical evidence programs, and sole‑source procurement pathways.

- Investors and acquirers will find asymmetric value in bolt‑on acquisitions that combine MRI‑safe pump technology with scale service organizations to extend margins via aftermarket and clinical service contracts.

Regulatory, procurement, and lifecycle dynamics shaping 2026 decisions

Three dynamics are especially important for decision‑makers in 2026:

- Regulatory scrutiny and clearance pathways: FDA guidance (including infusions pump lifecycle considerations) has increased expectations for human factors and clinical evidence. Recent 510(k) clearances for MRI‑safe devices confirm a credible pathway for differentiated product introductions, but they also raise the bar for documentation and post‑market surveillance.

- Public‑sector procurement signals: specialized equipment can be justified on a sole‑source basis where unique safety requirements exist. Recent procurement intent notices underscore how non‑magnetic technologies can secure preferential contracts when clinical safety and workflow benefits are demonstrable.

- Capital equipment lifecycle economics: hospital capital planners commonly use an 8‑year useful life benchmark for infusion pumps. This has material implications for amortization of new MRI‑specific investments, trade‑in strategies, and timing of scale deployments to align with replacement cycles.

How corporate leaders should act in 2026 — prioritized playbook

- Procurement timing: Align major purchases to coincide with replacement windows in multi‑hospital systems. Use TCO models tied to an 8‑year life cycle to make the case for premium MRI‑safe assets where downtime, patient throughput, or staff exposure risks are reduced.

- Product strategy: Prioritize non‑magnetic actuation (e.g., ultrasonic motors), MRI‑aware software features (drug libraries, remote control), and interoperability with imaging suites. Invest early in human factors validation to shorten regulatory timelines.

- Evidence generation: Sponsor pragmatic clinical studies and workflow evaluations that quantify MRI suite throughput gains, safety improvements, and net clinical benefit. These datasets materially influence procurement committees and public‑sector sole‑source justifications.

- Commercial models: Offer bundled service, training, and software licensing to convert hardware sales into recurring revenue streams and to lock in long‑term maintenance contracts.

- M&A and partnership criteria: Target firms that fill capability gaps (e.g., MRI actuation tech, imaging‑oriented workflow software, or regional distribution in under‑penetrated markets). Valuations should incorporate the high market concentration and the likely need for regulatory investment post‑acquisition.

- Geographic approach: Pursue a phased roll‑out — validate in tertiary imaging centers and high‑acuity hospitals, then expand to ambulatory imaging centers and regional hospitals as evidence and service capacity scale.

Using this report in the boardroom and investment committees

PW Consulting’s deliverables are designed for immediate use in capital allocation exercises and M&A diligence. Included tools make it straightforward to:

- Create defensible spend requests that quantify near‑term productivity and long‑term depreciation impacts across multi‑facility networks.

- Run sensitivity analyses that show how regulatory milestones and procurement outcomes (e.g., sole‑source wins) shift valuation ranges for target assets.

- Build integration roadmaps that align product development sprints to hospital procurement calendars, minimizing time‑to‑revenue after regulatory clearance.

What we intentionally withhold — and why you should read the full report

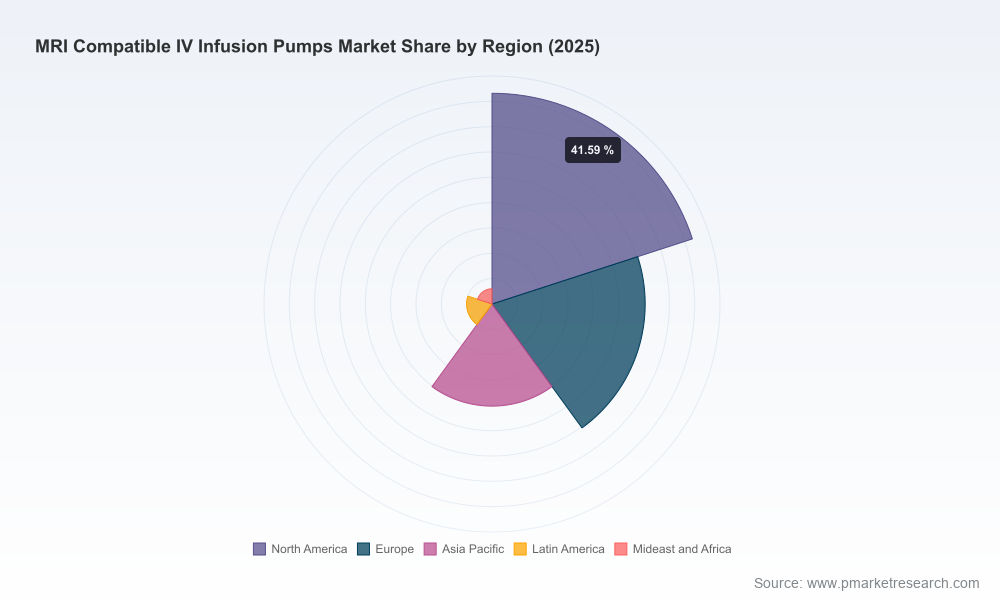

In this executive preview we present the consolidated market trajectory, concentration metrics, and the strategic implications of recent regulatory and procurement events to support rapid, high‑level decision making. We have intentionally withheld granular regional and application‑level splits, and detailed segment revenue tables — data that drive pitch‑ready commercialization plans and valuation workstreams. Access to these segmented datasets, company‑by‑company benchmarking, and downloadable financial models is included in the full PW Consulting report and is essential for tactical execution (e.g., setting prioritized SKU lists, regional launch sequencing, and precise bid pricing).

Closing perspective

By 2026 the MRI compatible infusion pump market will reward organizations that combine clinical credibility, regulatory foresight, and disciplined commercial execution. The combination of meaningful regulatory clearances, growing institutional procurement awareness, and predictable capital replacement cycles creates a window of opportunity for both specialists and incumbents to capture share and lock in recurring service streams.

PW Consulting’s Worldwide MRI Compatible IV Infusion Pumps Market report synthesizes these dynamics into actionable intelligence designed to support procurement officers, product leaders, corporate development teams, and investors. For access to the full dataset, company scorecards, and the downloadable decision‑support models referenced here, please consult the PW Consulting report page or contact our industry practice team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Worldwide MRI Compatible IV Infusion Pumps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com