What Is Driving the Arab Thobe and Abaya Fabric Market Toward USD 6.12B by 2032 at a 6.8% CAGR?

Other |

2026-06-27 11:40:45

PW Consulting’s latest market intelligence — the Worldwide Automotive Platooning System Market report (base year 2025) — equips senior executives and investment committees with proven frameworks to convert early momentum in platooning into durable commercial advantage. The sector has moved rapidly from experimentation to scalable pilots: global market value expanded from the low tens of millions in 2020 to roughly USD 126.5 Million in 2025, and our forecast shows an accelerated trajectory through the end of the decade. With a compound annual growth rate of 34.56% across the 2026–2032 forecast window, the market is projected to surpass the USD 1 Billion threshold by 2032. For leaders making resource-allocation and partnership decisions in 2026, the report is designed as a strategic playbook — providing granular scenario models, deployment templates, and supplier benchmarking while intentionally withholding certain proprietary segment-level tables to encourage direct engagement with the full dataset.

Worldwide Automotive Platooning System Market

Regulatory momentum has converted platooning from a technology experiment into a near-term compliance and efficiency lever. Hard targets on truck CO₂ reductions, vehicle-safety mandates and regional fleet procurement rules are creating deterministic demand pathways for technologies that demonstrably reduce fuel consumption and improve operational efficiency.

Worldwide Automotive Platooning System Market

Commercial operators are now evaluating platooning not as a standalone feature but as part of integrated fleet modernization strategies that include electrification, telematics, and route optimization. These combined investments change the economics of adoption and the cadence of scale-up.

Worldwide Automotive Platooning System Market

Market economics show a steep adoption curve: historical growth from 2020–2025 establishes a base, and our forecast — driven by deployment acceleration and enterprise pilots — demonstrates outsized opportunity over the remainder of the forecast period. That makes 2026 the year to move from passive monitoring to active capture.

When should my company move from pilot to fleet-wide deployment, and what are the critical scaling milestones?

Which partnership models (OEM-led, Tier-1-integrator, neutral platform provider) best protect margin while enabling rapid interoperability?

How do regulatory timelines and regional approvals change procurement sequencing and network design for multi-state / multi-country operations?

What are the realistic total-cost-of-ownership (TCO) outcomes when platooning is paired with electrification or alternative powertrain investments?

Decision-grade forecasting models: scenario-driven revenue and adoption curves with sensitivity levers you can toggle for fuel-price volatility, regulatory acceleration, and communication-technology choices.

Comprehensive TCO and ROI templates: downloadable spreadsheets that let fleet planners quantify payback windows under custom operating profiles, retrofit vs integrated purchase choices, and training costs.

Go-to-market playbooks: operator-facing commercial models, pricing approaches (hardware, software subscription, transaction-based services), and pilot-to-scale checklists.

Regulatory and compliance mapping: jurisdiction-level decision trees highlighting approval requirements, mandatory safety baselines and near-term regulatory risks across priority markets.

Supplier and technology scorecards: vendor evaluation matrices, integration risk assessments, and procurement RFP templates tailored to large-fleet buyers.

Pilot evaluation framework and KPIs: operational metrics, safety case templates, and change-management plans so trials convert into repeatable programs.

Note: The report demonstrates methodology and sample outputs in the executive summary; full datasets (including country- and application-level tables, time-series files, and an interactive scenario builder) are available on the source page for licensed users.

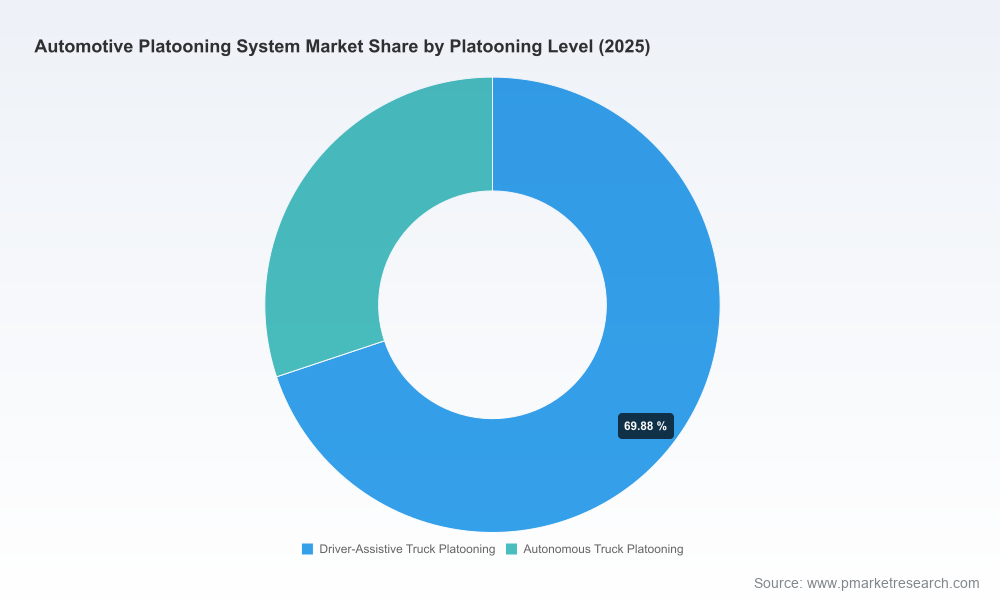

The market structure shows a clear tiering: OEMs with integrated vehicle platforms, systems suppliers that provide modular subsystems (sensors, braking and steering actuation, communications stacks), and a cohort of systems integrators and software-first players that stitch multi-vendor ecosystems together. Each class of player has distinct strategic advantages and blind spots.

Systems integrators and software-first firms (example: Peloton Technology) continue to commercialize driver-assistive platooning solutions that leverage proven short-range vehicle-to-vehicle communications and deep fleet partnerships to deliver near-term fuel-savings and safety benefits.

Dual-application providers (example: Kratos Defense & Security Solutions) demonstrate the value of cross-domain deployments — logistics and defense — which can accelerate scale and diversify revenue. Recent 2026 deployments on high-profile logistics corridors are proof points that dual-use strategies can create rapid, visible adoption.

OEMs and large truck manufacturers (examples include legacy heavy-truck brands) are embedding platooning capabilities into new vehicle platforms, emphasizing integration, warranty alignment and lifecycle services. Their propositions are attractive to large fleets seeking turnkey solutions.

Tier-1 component suppliers and braking/steering specialists are competing on reliability and standards compliance, selling the critical hardware and software primitives that make platooning safe and certifiable.

Strategic implications:

Partnership architecture matters. Fleets should prefer modular architectures that allow swapping communications stacks (DSRC vs C-V2X), sensor suppliers, and SaaS providers without full truck replacement.

New entrants can win by focusing on integration risk reduction (certified retrofit kits, operator training, nationwide maintenance networks) rather than feature parity alone.

OEMs and Tier-1s must accelerate multi-brand interoperability activities if they want to own fleet-level services rather than being relegated to component vendors.

One of the most decisive variables for 2026 capital planning is unit economics. Implementation of platooning systems typically carries significant up-front costs driven by sensors, camera suites, advanced braking and actuation hardware, software and operator training. Fleet planners should expect material per-truck investments when initiating scale pilots; however, these investments are offset, in many use cases, by route-level fuel savings, reduced driver fatigue costs and regulatory compliance value.

Regulatory tailwinds are uneven but powerful. Examples that materially affect adoption timelines include stringent CO₂ reduction mandates in regional blocs, state-level fleet procurement rules that push carriers toward zero- or near-zero-emission vehicles, mandatory safety baseline regulations (e.g., automated emergency braking) that lower the marginal safety cost of platooning, and active platooning approval processes in several U.S. states that condition operations on training and documented operational plans. Operators must treat regulatory programs as both constraint and catalyst — aligning deployment corridors and partner selection to jurisdictions with pragmatic approval frameworks.

Run a fleet-readiness audit: map routes, duty cycles, and driver availability to identify top 3 corridors for high-probability paybacks.

Build a modular pilot: select one OEM and one neutral integrator to de-risk supplier lock-in; include retrofit and new-vehicle paths in the same pilot.

Engage regulators early: submit operational plans in jurisdictions with clear approval pathways and negotiate data-sharing arrangements that preserve commercial confidentiality.

Model combined TCO: include electrification and platooning in the same financial model — synergies in energy use and route design materially change outcomes.

Design procurement for scale: insist on defined upgrade paths, software update SLAs, and data-export standards in contracts to protect future optionality.

Secure evident safety cases: adopt independent third-party validation for pilot safety KPIs to accelerate insurer and regulator acceptance.

The next 18 months will determine which organizations capture disproportionate value from platooning: those who treat it as a marginal tech upgrade and those who deploy it as a node in a broader fleet transformation strategy. With market momentum already visible in the historical record and a strong forecasted CAGR through 2032, 2026 is not the year to delay decisive action. PW Consulting’s Worldwide Automotive Platooning System Market report gives executives the empirical tools and executable roadmaps to move from pilot to scale with confidence. Our deliverables combine forecasting, procurement templates, regulatory maps, and vendor scorecards — with the full data sets and interactive models available through the report page.

Contact PW Consulting to obtain the full report and to schedule a private briefing where we will walk through tailored scenarios for your fleet, investment thesis, or M&A target set.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Platooning System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com