North America Homecare Medical Beds Market Trends, Demand and Revenue Forecast

Health |

2026-06-09 08:59:36

As companies set strategy for fiscal 2026 and beyond, our new Worldwide PVDF Fluorocarbon Coatings Market study delivers a targeted, decision-ready view of a market undergoing structural transition. The global PVDF fluorocarbon coatings market reached approximately USD 1,600.7 Million in the base year (2025) and is projected to expand at a compound annual growth rate (CAGR) of 6.02% through the 2026–2032 forecast window, reaching roughly USD 2,410.0 Million by 2032. This preview outlines the strategic value the full report provides to corporate leadership, M&A teams, product and commercial functions — and highlights the tactical choices that will determine winners in the next three years.

Worldwide PVDF Fluorocarbon Coatings Market

Timing: 2026 is a pivot year. Regulatory tightening, supply-side rebalancing and selective capacity additions are converging to reshape margins and access to PVDF resins — the feedstock that defines fluorocarbon coating economics and formulations.

Worldwide PVDF Fluorocarbon Coatings Market

Decision horizon: With a projected mid-single-digit CAGR through 2032, the market offers attractive volume growth but requires differentiated execution to capture premium pricing and durable share.

Worldwide PVDF Fluorocarbon Coatings Market

Strategic complexity: Accelerating demand for low-VOC, PFAS-scrutinized formulations, and pressure on raw-material costs mean that product roadmaps, procurement strategy, and customer value propositions must be tightly aligned.

Concise market sizing and forward-looking scenarios: base, growth, and stress cases to stress-test investment plans and capacity strategies across 2026–2032.

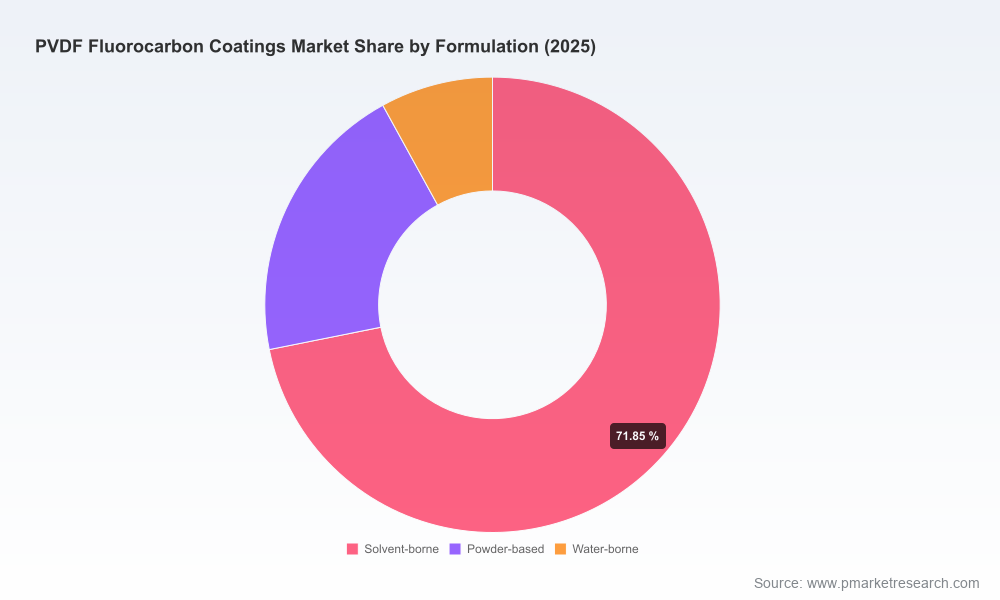

Demand architecture: segmented drivers by application classes and formulation preferences, with adoption curves and buyer decision matrices to prioritize go-to-market effort.

Price and input-cost modelling: forward curves and sensitivity analysis that link VDF and PVDF feedstock moves to coating ASPs and margin impacts under alternative pass-through assumptions.

Supply-chain topology and capacity maps: visibility on incumbent resin producers, licensed formulators, toll-coaters, and potential chokepoints for rapid escalation mitigation.

Regulatory impact playbook: jurisdictional regulatory levers, compliance cost overlays, and formulation change matrices to quantify R&D and requalification burdens.

Competition and product-mapping toolkit: company scorecards, capability heatmaps, and white-space matrices for partnership and acquisition screening.

M&A and commercial diligence templates: acquisition price levers, synergies, and integration checklists calibrated to PVDF value pools.

Actionable go-to-market and commercialization roadmaps: pilot-to-scale paths for waterborne and surfactant-free solutions, and recommended channel/partner models for architectural and industrial end-markets.

The PVDF fluorocarbon coatings value chain remains moderately concentrated. The top three producers account for a meaningful share of resin supply, while the top five further consolidate market control, reflecting a mix of global resin manufacturers and large formulated-coating suppliers. This structure creates both opportunity and risk for new entrants and downstream formulators: access to qualified 70% PVDF resin streams and colocated service support matters. Our intelligence on leading players synthesizes public announcements, product positioning, and observed commercial behavior:

Arkema (France) — Arkema’s Kynar® portfolio remains a benchmark for high-performance PVDF resins in architectural and industrial coatings. Recent moves include a capacity expansion plan in Changshu (announced March 2026) that targets roughly a 20% uplift to support coatings and other uses, and earlier product advances with Kynar Aquatec® waterborne systems aimed at low-VOC architectural protective coatings. These steps illustrate a two-track strategy: secure upstream feedstock capacity while accelerating lower-VOC downstream offerings.

Solvay (Belgium) — With its Hylar® PVDF resins, Solvay continues to be a preferred supplier for licensed formulators seeking premium, long-lasting facade coatings. The company’s emphasis remains on resin performance for color retention and substrate protection—an important differentiator in durability-driven procurement cycles.

PPG Industries (United States) — As both a formulator and a customer of high-durability resin systems, PPG leverages vertical capabilities to marry resin selection, formulation know-how, and global distribution, particularly for architectural coil and extrusion markets.

AkzoNobel (Netherlands) and Sherwin-Williams (United States) — These coatings majors continue to protect architectural market share with branded PVDF fluorocarbon systems optimized for weather resistance and cladding applications; their scale in coil-coating channels and OEM relationships remains a structural advantage.

Daikin Industries and Kureha (Japan) — Focused primarily on resin manufacture, these firms bring technical depth on chemical resistance and polymer consistency. Their competitiveness is increasingly defined by feedstock sourcing resilience and ability to support formulators through quality and supply reliability.

Raw-material volatility is a near-term and persistent factor. Northeast Asia PVDF pricing was observed at USD 15.36/kg in April 2026, reflecting recent upward pressure. More broadly, rising costs of vinylidene fluoride (VDF) monomer and episodic regulatory clampdowns in key Chinese provinces have created discrete production cost shocks — industry sources attribute localized cost increases on the order of 10–12% in impacted facilities. These dynamics combine with selective capacity additions to create a segmented market: supply flexibility will favor players with diversified sourcing, tolling agreements, or local production footprints.

Concurrently, regulatory tightening — especially VOC emission ceilings and PFAS-related scrutiny in North America and Europe — is accelerating formulatory change toward low-VOC and surfactant-free PVDF systems. That trend imposes near-term R&D and requalification expenses but unlocks premium, specification-driven pricing for compliant, high-durability products.

Short-term risk mitigation: secure medium-term resin offtake through hedged contracts, tolling partnerships, or localized inventory hubs to protect critical projects from supply disruption and spot-price swings.

Product differentiation: accelerate validation and commercialization of waterborne, low-VOC, surfactant-free fluorocarbon coatings for regulated markets; prioritize performance claims that are certifiable under evolving standards.

Value-chain capture: evaluate selective vertical integration or strategic alliances with resin producers to gain preferential access to qualified 70% PVDF streams and to protect margins.

Commercial model redesign: move from transactional selling to solutions-selling for architectural customers—warranty-linked pricing, lifecycle cost calculators, and performance-backed guarantees to justify premium positioning.

M&A and partnership filters: prioritize targets with proven formulation IP, regional coating capacity near growth corridors, or complementary service offerings (e.g., pretreatment, testing labs) to accelerate time-to-market.

Sustainability and regulatory preparedness: embed compliance scenarios into product roadmaps and procurement contracts to avoid reactive redesign costs and to secure first-mover advantages in low-emission specifications.

The published report is structured as a practical playbook: modular, model-driven, and oriented to rapid executive decision-making. Clients receive an interactive forecast model, scenario dashboards, supplier heatmaps, M&A screening matrices and a prioritized 30/90/180-day action list tailored to their role (commercial, procurement, R&D, or corporate development). For companies that need faster alignment, we offer executive workshops that translate the market model into specific pricing, sourcing, and product-extension actions for FY2026.

This release is a strategic preview designed to highlight the analytic depth and practical utility of our full study. To preserve the competitive value of our granular segmentation, regional build-ups and deal-level benchmarks (which underpin the robust recommendations outlined here), detailed breakdowns and proprietary datasets are available exclusively with the full report. Corporate teams evaluating investments, supply agreements, or R&D pivots for 2026 should consult the complete model and bespoke advisory services to convert this intelligence into executable advantage.

Contact PW Consulting to request the full Worldwide PVDF Fluorocarbon Coatings Market Report and to schedule a briefing with our senior industry analysts. In a market where supply, regulation, and formulation preferences are shifting rapidly, the right insights—and the right timing—will determine who leads the next cycle of durable, high-value fluorocarbon solutions.

For detailed analysis of this topic, please visit the official page:Worldwide PVDF Fluorocarbon Coatings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com