Silicon Anode Battery market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-14 09:36:13

In a year when capital allocation and technology bets will determine winners in precision manufacturing and photonics-enabled industries, PW Consulting’s latest Worldwide High Power Continuous-Wave (CW) Laser Market report provides the strategic intelligence leaders need for 2026. The global high-power CW laser market reached roughly USD 3.4 billion in 2025 and, under the baseline scenario modeled in this study, is on a compound annual growth trajectory of 8.5% across 2026–2032 — approaching the USD 6.0 billion mark by the end of the forecast period. This briefing summarizes the actionable implications of those trends while preserving the report’s proprietary drill-down tables and supplier scores for full subscribers.

Worldwide High Power CW Laser Market

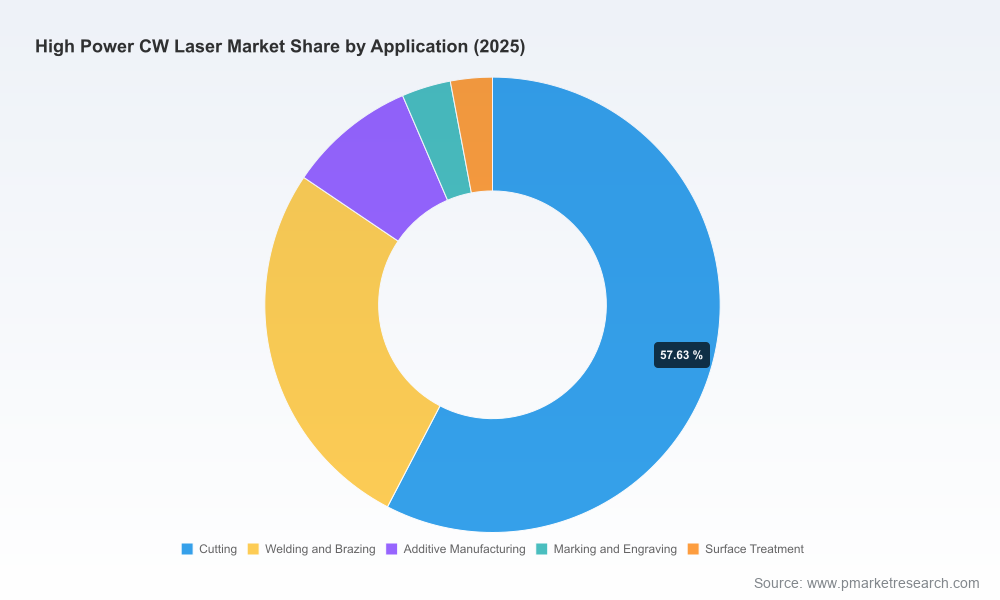

Three near-term structural forces converge in 2026 to reshape supplier selection, capital investment, and product roadmaps for high-power CW lasers: accelerating adoption of Industry 4.0 automation in metalwork, rapid electrification (notably battery welding in EVs), and expanded requirements for additive manufacturing in aerospace and defense. At the same time, downstream demand is diversifying — from traditional sheet-metal cutting to high-precision welding and emerging datacenter and silicon-photonics use cases — creating parallel value chains with distinct technical and commercial requirements.

Worldwide High Power CW Laser Market

From a technology strategy perspective, 2026 will be defined by a few high-impact inflection points:

Worldwide High Power CW Laser Market

Raw-material concentration remains an operational risk. Gallium and indium supply dynamics, for example, experienced volatility in recent years, with spot-price spikes followed by partial reprieve through regional recycling initiatives. For procurement and strategic sourcing teams, the implication is clear: develop multi-tiered supplier strategies, build inventory and recycling programs for critical elements, and prioritize component standardization where possible to reduce single-sourcing exposure.

Regulatory and safety constraints compound technical risks. High-power CW devices necessitate rigorous thermal and optical safety engineering, impacting product certification timelines and aftermarket maintenance models. Companies that invest early in compliance engineering and training for field technicians will realize faster market access and lower warranty costs.

Our competitive analysis synthesizes company-level strengths and near-term moves across high-power CW suppliers. Highlights include:

Selected near-term developments reinforce these dynamics. A leading fiber-laser vendor showcased a compact 8 kW single-mode source at a major optics conference and received industry recognition for the design; another major supplier is sampling high-power, datacenter-focused CW lasers for silicon-photonics co-packaging; and niche photonics companies continue to push high-efficiency DFB and InP technologies that feed emerging markets. These moves signal both incremental innovation in traditional processing and potential disruptive linkage to datacenter and photonics supply chains.

This report is built for decision-makers who need both strategic clarity and operational templates. Subscribers receive:

For CEOs and strategy teams, our analysis identifies where to place bets and where to stay flexible. Procurement leaders should lean into multi-year supplier engagements that lock in service-level agreements and spares visibility. R&D heads must prioritize thermal management and beam-control innovations that materially reduce process cycle time or expand material compatibility. Private equity and corporate development groups will find the market concentration metrics useful when screening consolidation targets; the dominant incumbents remain attractive acquirers of complementary capabilities.

High-power CW lasers are not a single market but a set of intersecting markets: industrial materials processing, precision manufacturing, and nascent photonics-enabled data infrastructure. PW Consulting’s report quantifies the growth path to 2032 and translates it into actionable choices for procurement, R&D, M&A, and risk management. It shows where scale matters, where modularity wins, and where supply-chain resilience is a make-or-break variable.

For executives preparing budgets, supplier lists, and product roadmaps in 2026, the report delivers both the macro market context and the operational tools to execute. Detailed regional and application splits, full vendor scorecards, price curves, and downloadable financial models are intentionally reserved for the full report — to serve as the operational playbook you can use immediately.

For detailed analysis of this topic, please visit the official page:Worldwide High Power CW Laser Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com