Worldwide Application Security Solution Market — Strategic Preview for 2026 Decision-Making

As organizations accelerate software delivery while defending increasingly sophisticated attack surfaces, application security (AppSec) has moved from checkbox compliance to a strategic priority. PW Consulting’s latest market study — Worldwide Application Security Solution Market — synthesizes five years of historical data and a seven‑year forecast to equip executives with the insight required to make informed investments in 2026. This preview highlights the report’s strategic value, key market dynamics, and high‑impact recommendations, while preserving detailed segment-level intelligence for subscribers who access the full report.

Worldwide Application Security Solution Market

Market snapshot: scale and pace matter

Our analysis shows that the global AppSec market has entered a high‑velocity growth phase. The market reached roughly USD 15.7 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 17.22% across the 2026–2032 forecast horizon, exceeding USD 47 billion by 2032. These macro numbers underscore an inflection point: vendors and adopters that align product strategy, procurement, and engineering practice now can capture outsized value as demand for integrated, automated security rises.

Worldwide Application Security Solution Market

Why this report matters to 2026 decision-makers

- Actionable vendor intelligence: The study profiles market leaders and specialist challengers across testing modalities, supply‑chain security, and runtime protections, assessing product breadth, technical depth, and go‑to‑market models.

- Operational playbooks: Practical integration patterns for shift‑left testing, CI/CD pipelines, and cloud‑native runtimes are included — not just theory, but executable steps and sample KPIs for 90‑, 180‑ and 365‑day pilots.

- Regulatory and risk mapping: We translate policy shifts (e.g., software product security mandates and SBOM expectations) into programmatic requirements and prioritized controls for procurement and engineering teams.

- Financial decision support: TCO and ROI frameworks illustrate when to favor developer‑first tools versus platform suites, and quantify the impact of faster remediation and fewer production incidents.

- Roadmaps for integration of AI: Given rapid adoption of GenAI in AppSec workflows, the report provides guardrails and integration patterns for safely deploying AI augmentation without introducing new supply‑chain risks.

Market dynamics driving 2026 priorities

Several converging forces make 2026 a decisive year for AppSec strategy:

Worldwide Application Security Solution Market

- Regulatory acceleration: New and pending regulations are raising the bar for software security obligations, including requirements for handling vulnerabilities and visibility into software supply chains. Organizations selling into regulated markets must reconcile product roadmaps with compliance timelines.

- Shift in attacker economics: As common injection and access‑control weaknesses remain persistent, attackers increasingly monetize automated exploitation. Enterprises face rising operational and reputational costs for application incidents.

- AI as a force multiplier: The market is witnessing a rapid uptake of AI to triage, prioritize, and even remediate vulnerabilities. While AI shortens mean time to remediation, it also changes procurement criteria — buyers now ask about models, data lineage, and guardrails as much as detection accuracy.

- Architecture divergence: Legacy monolithic applications continue to present outsized exploit risk compared with modern microservices and cloud‑native stacks, necessitating differentiated risk treatment and tooling choices.

Competitive landscape — who to watch and what they mean for buyers

The competitive topology is a mix of broad‑platform incumbents, developer‑centric disruptors, and highly focused runtime or SCA specialists. Market concentration metrics indicate the sector is neither a tight oligopoly nor entirely atomized: the top three and five players command meaningful shares without stifling innovation from specialists.

- Platform incumbents (enterprise suites): Established vendors continue to compete on breadth across static, dynamic, software composition analysis (SCA), and runtime capabilities, with deeper SIEM/ITSM integrations that appeal to large program teams. Acquisition activity has reinforced breadth and enterprise footprint, and buyers seeking end‑to‑end visibility lean toward these suites for operational consistency.

- Developer‑first challengers: Tools designed for rapid feedback in developer workflows — focusing on low friction SAST/SCA or container and IaC scanning — are accelerating adoption among modern engineering organizations. Their differentiator is speed and usability, especially where developer productivity is a strategic priority.

- Runtime and protection specialists: RASP and IAST providers offer real‑time detection and protection in production. For regulated or high‑risk environments, runtime controls are increasingly viewed as complementary to shift‑left prevention.

- Supply‑chain and repository controls: SCA and repository lifecycle platforms have become critical as SBOM and component risk management move from checkbox to boardroom agenda items.

Recent vendor moves illustrate tactical directions the market is taking: AI‑driven remediation engines are being launched to shorten fix cycles; integrations between AppSec platforms and popular AI coding assistants are emerging to secure AI‑generated code; targeted acquisitions are strengthening supply‑chain security; and FedRAMP and other certifications are enabling public sector adoption. These developments change procurement checklists and vendor evaluation criteria for 2026.

Core report contents — what you’ll find inside

PW Consulting’s full report delivers layered, usable intelligence for decision-makers:

- Macro market sizing and forecast models with scenario analyses that reflect divergent adoption and regulatory pathways.

- Vendor scorecards assessing technical coverage (shift‑left, build‑time, CI/CD, runtime), integration maturity, developer experience, and enterprise‑grade controls.

- Deployment blueprints tailored to archetypes — legacy enterprise, cloud‑native scale‑out, regulated verticals, and high‑velocity fintech — with stepwise milestones and KPI templates.

- Procurement playbook including RFP language, contractual security clauses, and evaluation matrices that compare operational and financial tradeoffs.

- Use‑case analyses (e.g., open source risk reduction, API security, mobile app protection) that map to technical controls and operational costs — enabling prioritization without requiring wide retooling.

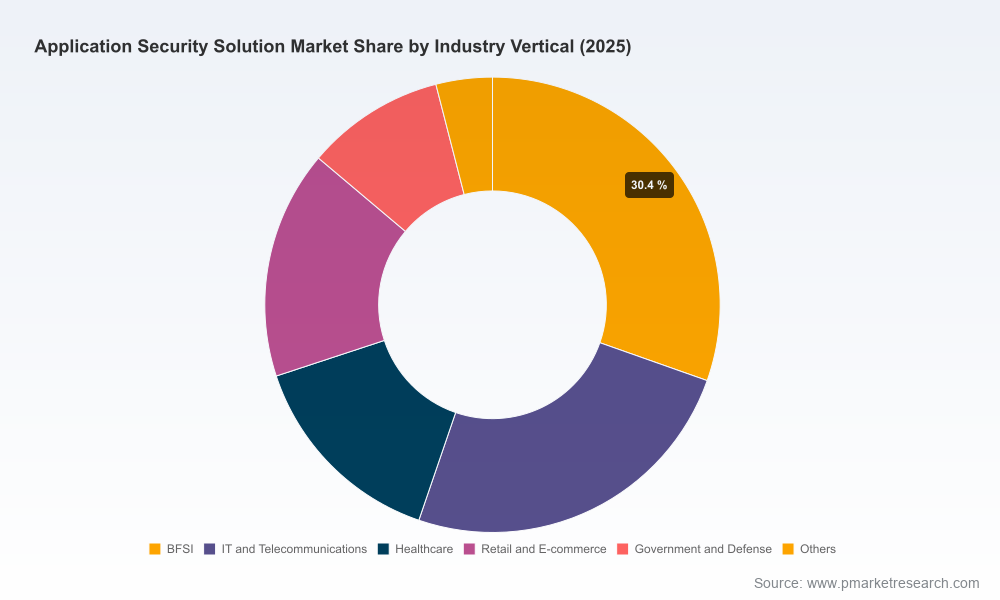

To honor the “preview” principle, detailed split metrics by region, solution type, and vertical are available in the full report and interactive dataset. These granular insights are curated to support vendor selection and budget allocation decisions for 2026.

Strategic recommendations for 2026

Executives should translate this market intelligence into a compact set of strategic moves over the next 12 months:

- Prioritize developer experience in tool selection: Where speed and scale matter, favor tools that integrate natively into CI/CD and IDEs and provide clear remediation guidance tied to code ownership.

- Adopt an AI‑governed remediation layer: Pilot AI‑assisted remediation engines with strict governance: model provenance, explainability, and human‑in‑the‑loop checkpoints to mitigate automation risk.

- Map compliance to engineering milestones: Translate regulatory timelines into technical tickets and SBOM rollouts; treat compliance as a delivery stream rather than a standalone audit activity.

- Balance prevention and runtime controls: Combine shift‑left testing with runtime protections for high‑risk services; runtime controls provide a safety net while prevention maturity ramps up.

- Invest in SCA and supply‑chain hygiene: Given evolving procurement standards, secure software composition processes now reduce legal and operational exposure later.

- Build vendor flexibility into contracts: Seek modular commercial terms and clear SLAs for model updates, vulnerability lifecycle expectations, and certification obligations.

What to expect next from PW Consulting

PWC’s full Worldwide Application Security Solution Market report is designed as an executive decision pack for 2026. Subscribers receive the detailed dataset, vendor scorecards, deployment playbooks, and a short briefing session with our analysts to tailor findings to your organization’s risk profile and engineering roadmap. For procurement teams, we provide an editable RFP template and TCO model tuned to your delivery cadence and compliance footprint.

If your enterprise will be making AppSec investments, changing vendors, or committing to an operational security program in 2026, this report reduces execution risk by aligning technical choices with regulatory timelines, developer needs, and financial constraints.

Call to action

Access the full intelligence package on the PW Consulting website to obtain the granular segment analysis, interactive forecasts, and vendor matrices that underpin the strategic recommendations summarized here. Our team is also available for tailored briefings to convert these insights into a prioritized implementation roadmap for your organization.

For detailed analysis of this topic, please visit the official page:Worldwide Application Security Solution Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com