Retrovert Hoodie: A Fresh Look at Modern Streetwear Style

Shopping |

2026-07-06 08:23:19

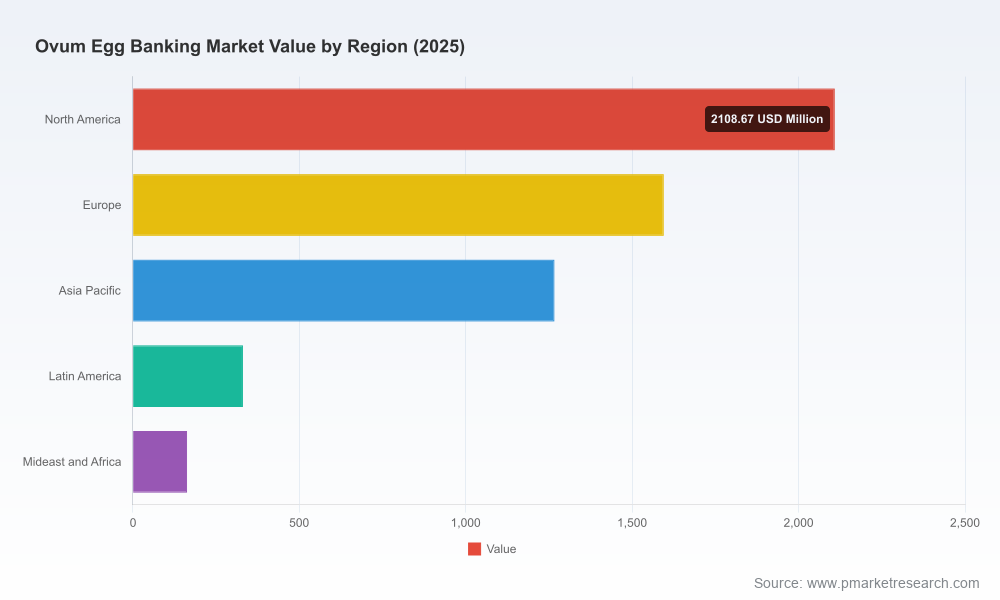

PW Consulting’s new market brief, Worldwide Ovum Egg Banking Market (base year 2025, forecast 2026–2032), equips executives with the strategic intelligence required to make high-stakes decisions in 2026 and beyond. The global market reached an estimated USD 5,464.3 Million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 12.48% through the 2026–2032 horizon, reaching approximately USD 12,462.5 Million by 2032. These macro dynamics underscore a period of accelerated demand, technology diffusion, and commercial reconfiguration across clinical providers, dedicated cryobanks, and new market entrants.

Worldwide Ovum Egg Banking Market

Policy and clinical clarity: Recent professional guidance and regulatory activity in 2025–2026 are reducing clinical uncertainty, enabling more predictable adoption pathways for planned and medically indicated oocyte cryopreservation.

Worldwide Ovum Egg Banking Market

Commercial inflection: A mid‑decade inflection point is visible—market headroom and patient demand are converging with improved logistics, distributed storage models, and expanding clinic networks to accelerate monetization.

Worldwide Ovum Egg Banking Market

M&A and scale opportunities: Fragmentation metrics indicate meaningful opportunities for consolidation and platform plays that capture cross‑border volume flows, clinical networks, and digital patient acquisition advantages.

This report is built for executives who need more than high‑level trend lines: it provides a pragmatic playbook to capture value in a growing and evolving market. Core deliverables include:

Validated market sizing and high‑granularity forecasts (2020–2032) with scenario modeling to stress-test investment cases under alternate clinical, reimbursement, and regulatory outcomes.

Commercial segmentation framework and go‑to‑market archetypes for new entrants and incumbents, including customer segmentation, channel economics, and acquisition cost benchmarks.

Regulatory and reimbursement compendium covering coding, payer pathways, and mandates that materially affect demand and pricing realization across key jurisdictions.

Clinic and cryobank benchmarking tools: operational KPIs, capacity planning templates, and cost-to-serve models to optimize utilization and margin profiles.

Technology and logistics assessment: evaluation of cryopreservation methods, cold‑chain innovations, and digital platforms that reduce loss, improve match rates, and lower patient friction.

Risk and resilience playbook: practical mitigations for supply‑chain disruption, regulatory divergence, litigation risk, and clinical outcome variability.

M&A road map and valuation heuristics tailored to strategic buyers, financial sponsors, and strategic alliances—including integration checklists for clinical and laboratory consolidation.

The market comprises a spectrum of specialized cryobanks, vertically integrated clinic groups, and vertically neutral service providers. Market concentration remains relatively low—top three and top five market shares indicate the sector is fragmented—creating an environment that favors both focused specialists and ambitious consolidators.

Cryos International A/S — A Europe‑based donor egg specialist with international distribution capabilities. Its strengths lie in donor network scale and cross‑border logistics, presenting a relevant benchmark for firms building global distribution channels.

California Cryobank (Human Potential, Inc.) — A legacy brand in reproductive tissue banking with strong clinical partnerships. Its integration of cryopreservation services and reproductive medicine know‑how highlights the value of trusted brand equity and clinical relationships in pricing power and patient acquisition.

Donor Egg Bank USA LLC and Fairfax EggBank, Inc. — Specialists focused on searchable donor inventories and clinic distribution. Their models underscore the importance of data‑driven donor matching, inventory management, and digital patient journeys.

ReproTech LLC and Cryo-Cell International Inc. — Long‑standing cryogenic storage providers whose value proposition emphasizes long‑term storage security, chain‑of‑custody rigor, and compliance — critical attributes as reputational risk rises.

Clinic Networks (CCRM Fertility, IVIRMA Global, Shady Grove Fertility, Kindbody, Boston IVF, Monash IVF Group, Genea, Extend Fertility, etc.) — These integrated clinic groups combine clinical services with banking capabilities. Their competitive advantage comes from patient funnel control, bundled service offerings, and the potential to optimize clinical throughput and match rates.

Strategic implication: incumbents with strong clinical‑to‑storage linkages can extract higher lifetime value per patient, while pure‑play cryobanks must differentiate on cost, safety, and distribution reach. New entrants should evaluate partnerships with clinic networks or buyer consolidation strategies to accelerate scale.

Professional guidance is changing the narrative. The American Society for Reproductive Medicine (ASRM) updated its Ethics Committee and Practice Committee opinions in 2025–2026, reaffirming planned oocyte cryopreservation as ethically permissible while stressing informed consent around long‑term uncertainties. This clarity reduces adoption friction for elective users and supports broader clinical acceptance.

Coding and reimbursement create asymmetric economics. Current procedural terminology (CPT) codes exist for cryopreservation and thawing, but direct third‑party reimbursement for donor egg services remains limited in many markets. This keeps purchase transactions predominantly out‑of‑pocket, shaping pricing strategies and patient financing product design.

Mandates and medical indications are growth accelerants. Fertility preservation mandates in certain jurisdictions—particularly provisions for patients undergoing gonadotoxic therapy—create stable baseload demand and help normalize the clinical pathway for medical oocyte banking.

Clinical evidence and outcomes matter increasingly. Milestones reported by leading clinics—such as multi‑hundred cycle programs and measurable live birth outcomes from frozen oocytes—bolster confidence in efficacy and support higher willingness to pay, particularly for elective procedures.

Prioritize partner ecosystems: Secure distribution partnerships with clinic networks early to lock in referral streams and reduce customer acquisition costs.

Invest in trust architecture: Demonstrable quality systems, audit trails, and transparent outcomes reporting will differentiate providers as patient scrutiny rises.

Design flexible pricing and financing: With out‑of‑pocket dynamics dominant, flexible payment plans, subscription models for long‑term storage, and value‑bundling with fertility services will expand addressable demand.

Plan M&A as a capability play: Target acquisitions that add donor databases, cold‑chain logistics, or clinic access rather than merely revenue—these capabilities accelerate path to profitability.

Use scenario modeling to de‑risk investments: Test investment cases against alternate regulatory and reimbursement outcomes; early winners will be those who can pivot between elective and medically indicated demand curves.

Strategic investors and private equity: Use the scenario models and M&A road map to size investment opportunities and set realistic exit multiples tied to clinical KPIs.

Clinic groups and hospital systems: Leverage the benchmarking toolkit to optimize capacity planning, reduce cycle costs, and assess the economics of in‑house storage versus outsourcing.

Manufacturers and logistics providers: Identify product and service gaps where technology can lower cost‑per‑unit and improve cold‑chain reliability.

Policymakers and payers: Access the report’s regulatory and reimbursement analysis to understand how coding, mandates, and clinical guidance affect utilization and budget impact.

As the ovum egg banking market moves from niche to mainstream, 2026 will be a decisive year for organizations choosing between expansion, defensible specialization, or consolidation. With the global market on a trajectory from an estimated USD 5.46 billion in 2025 to an anticipated USD 12.46 billion by 2032 at a 12.48% CAGR, executives must act on validated scenarios, operational levers, and partnership strategies to capture disproportionate value.

PW Consulting’s Worldwide Ovum Egg Banking Market report translates these macro trends into concrete, executable strategies—without giving away the proprietary segmentation and granular payer-sensitive numbers that power investor and M&A decisions. For a complete set of charts, country rollups, segment dynamics, and the proprietary vendor scoring model, access the full report and supporting data on the PW Consulting website.

For detailed analysis of this topic, please visit the official page:Worldwide Ovum Egg Banking Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com