Whey Protein Isolate Market Witnesses Strong Growth Driven by Rising Demand for High-Protein Nutrition

Food |

2026-04-06 14:29:56

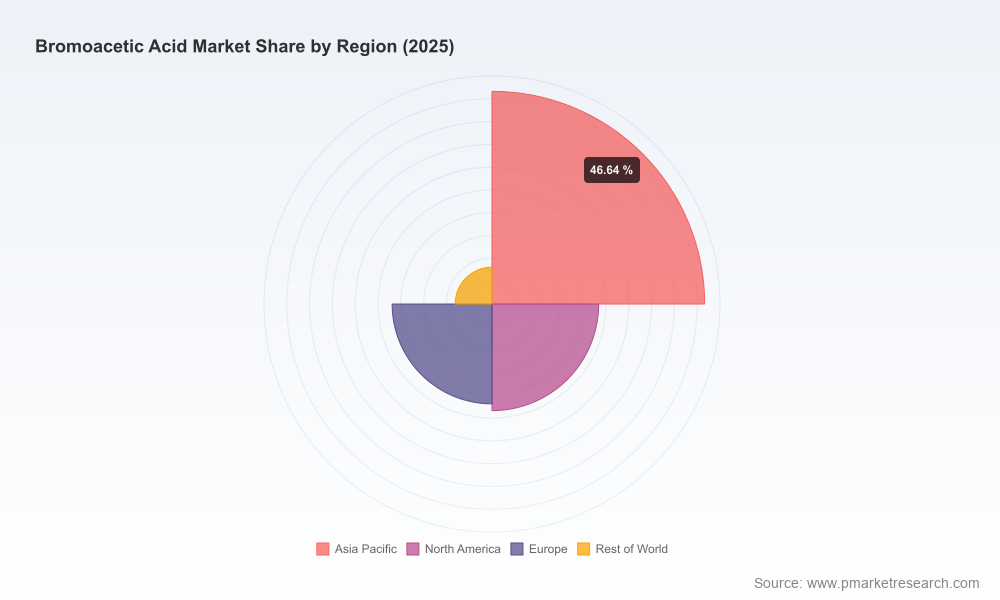

PW Consulting today publishes an executive preview of our Worldwide Bromoacetic Acid Market report (base year 2025; historical 2020–2025; forecast 2026–2032). The market’s macro trajectory is clear: after steady growth through the first half of the decade, measured expansion continues into the forecast window with a compound annual growth rate (CAGR) of 4.4%. Our modelling projects global revenues rising from a 2025 base to a materially larger market by 2032 under the central-case scenario. This briefing explains why that trajectory matters for procurement, manufacturing, regulatory, and M&A decisions in 2026, and what pragmatic actions business leaders should prioritize.

Worldwide Bromoacetic Acid Market

Strategic raw-material exposure: Bromoacetic acid is a core intermediate used across pharmaceutical synthesis, agrochemicals, surfactants and fine chemicals. Its price and availability are tightly coupled to upstream acetic acid dynamics and to regulatory drivers that reshape permitted uses and logistics.

Worldwide Bromoacetic Acid Market

Manageable but non-trivial concentration: The market exhibits moderate concentration — our concentration metrics show that the top three suppliers account for a meaningful share, and the top five increase that share further. This structure produces a landscape where national champions and specialist reagent suppliers both exert pricing and quality influence.

Worldwide Bromoacetic Acid Market

Regulatory and transport complexity: Recent regulatory actions and transport classifications have altered compliance and cost structures for producers, distributors, and end users — an operational risk that must be incorporated into sourcing and product stewardship strategies in 2026.

Using 2025 as the analytical base year, our forecast envelope incorporates scenario and sensitivity testing across demand, upstream cost pass-through and regulatory disruption. The central-case CAGR of 4.4% through 2032 reflects a balance of sustained demand in high-value pharmaceutical intermediates, measured expansion in agrochemical syntheses, and pressure on certain low-margin industrial applications. Revenue growth in nominal USD terms is positive and resilient to moderate commodity shocks, but margin profiles differ markedly by product grade and customer segment — a dynamic the full report quantifies with region- and application-level scenarios.

Upstream feedstock volatility: Acetic acid remains the primary feedstock. Regionally divergent price moves in early 2026 — including notable increases in parts of Northeast Asia and more modest rises in North America, with other markets showing softening — translate into asymmetric cost pressures for producers. Buyers and manufacturers must adopt geographically-aware procurement strategies to avoid margin compression.

Regulatory tightening and use restrictions: European and international regulatory actions in 2025 and 2026 have added compliance overhead. Notably, certain derivatives of bromoacetic acid have been captured by restricted-substance provisions under major chemical regulatory frameworks, and biocidal product approvals have seen administrative adjustments. These measures increase approval timelines and the cost of stewardship — impacting time-to-market for formulations and requiring proactive regulatory dossiers.

Transport and handling constraints: Classification under dangerous goods protocols has practical implications for logistics pricing, packing choices and cross-border supply chain design. Firms that internalize transport risk and optimize packing and routing can extract competitive advantage at the margin.

Quality segmentation and value capture: The market clearly bifurcates between high-purity reagent/pharmaceutical grades and technical-grade volumes. Premiums accrue to suppliers that can demonstrate validated quality systems, traceability and material stewardship for regulated pharmaceutical manufacturing.

The competitive field blends global reagent suppliers, regional bulk producers, and specialty firms focused on pharmaceutical intermediates. Key players include a mix of Western reagent brands and Asian manufacturers that serve both domestic and export channels. Their profiles are illustrative for strategic benchmarking:

Established reagent suppliers: Global life-science and specialty-chemicals brands provide high-purity grades to R&D and regulated manufacturing customers. Their strengths are trusted quality, broad distribution networks and regulatory support; their weakness is higher cost structures versus commodity producers.

Indian and Chinese producers: Several manufacturers and exporters have built scale in bulk supply and have competitive cost positions. They are increasingly upgrading quality capabilities to capture higher-value pharmaceutical intermediate business. Their agility on pricing and capacity makes them pivotal suppliers for industrial-scale requirements.

Small to mid-sized specialists: Regional companies that emphasize custom synthesis, lot-size flexibility and rapid customer service are critical for niche markets and for customers needing expedited development supplies.

Our concentration analysis shows a market where the top three suppliers hold a substantial share but do not dominate to the point of creating a single price setter; the top five push concentration higher. This structure favors strategic partnerships, targeted capacity investment, and selective consolidation rather than large-scale monopolistic moves.

Regulatory scheduling and approvals: Recent decisions by European bodies have demonstrated both the risk of restrictions and the possibility of administrative postponements that provide breathing space for affected stakeholders. Companies should model time- and cost-to-compliance under multiple regulatory timelines.

Restricted derivatives: Inclusion of certain esters and derivatives on restricted lists warrants a forward-looking substitution and reformulation strategy for affected product lines, especially in markets with stringent REACH-like regimes.

Logistics and hazardous goods management: The UN classification and packing-group assignments affect cross-border freight costs and warehousing requirements. These are implemented unevenly across jurisdictions, so localized compliance programs are essential.

This report goes beyond market sizing to equip executives with operational playbooks and decision-ready analytics. Highlights include:

Proprietary demand model and scenario matrices covering 2026–2032, with sensitivity testing against feedstock price shocks, regulatory disruption and substitution trends.

Cash-flow and margin models for representative producer archetypes (reagent specialist, bulk exporter, and integrated chemical group) that quantify the impact of acetic acid price movements and logistics reclassifications.

Supply-chain maps and risk heatmaps showing supplier concentration points, logistical chokepoints, and mitigation levers for procurement teams.

Regulatory matrix and compliance playbook detailing pathways to maintain market access in major jurisdictions, dossier templates and timelines for common approval scenarios.

Commercial playbook: procurement hedging strategies, pricing-clauses best practices, and contract language to manage pass-through of feedstock costs and transport surcharges.

Competitive intelligence dossiers on the market’s leading suppliers, with capability matrices benchmarking quality, geography, scale, and strategic intent.

M&A and investment screening tools: target scoring for bolt-on acquisitions and greenfield vs. brownfield capacity expansion under alternative demand scenarios.

Integrate feedstock monitoring into procurement KPIs. Given the volatility observed across regions, buyers should implement price collars, strategic forward purchases in stable jurisdictions, and supplier multi-sourcing to reduce exposure.

Prioritize product stewardship capacity. Firms supplying regulated markets must invest in regulatory dossiers and in-house compliance capabilities to avoid market-access freezes and to capture premium pricing for validated material.

Reassess logistics strategies. Evaluate warehousing, routing and packaging options that reduce hazardous-goods surcharges and limit potential transshipment complications in regulated corridors.

Consider selective capacity augmentation. For producers with strong commercial access to pharmaceutical intermediates, targeted investments in high-purity manufacturing and quality systems can yield higher margins than volume-focused expansion.

Run M&A screens now. The market’s concentration profile creates opportunistic windows for bolt-on acquisitions that secure geographic access or technical expertise without requiring market-winning scale.

Our approach combines primary supplier interviews, validated price series, regulatory scanning and a calibrated demand model that internalizes feedstock cost pass-through, quality premia and regulatory timelines. The result is not a single forecast to be accepted uncritically, but a decision-focused toolkit: scenario outputs, stress testing, and transaction-ready valuation cushions that enable procurement, business development and strategy teams to act with confidence in 2026.

This preview highlights the strategic implications and operational levers that matter in 2026. For granular segment-level data, downloadable forecast spreadsheets, detailed company profiles and the full set of procurement and regulatory playbooks, consult the full PW Consulting Worldwide Bromoacetic Acid Market report. The full report contains the detailed splits, sensitivity tables and primary-source annotations that senior decision makers require to finalize budgets, prioritize investments and structure commercial agreements for the year ahead.

PW Consulting stands ready to support bespoke applications of this analysis — from supply-chain stress tests and supplier due diligence to regulatory impact assessments and M&A target screening. Contact our industry practice for tailored briefings and interactive model walkthroughs.

For detailed analysis of this topic, please visit the official page:Worldwide Bromoacetic Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com