Potato Planter Market Trends Reshaping Global Business Strategies in 2026

Other |

2026-05-15 07:03:23

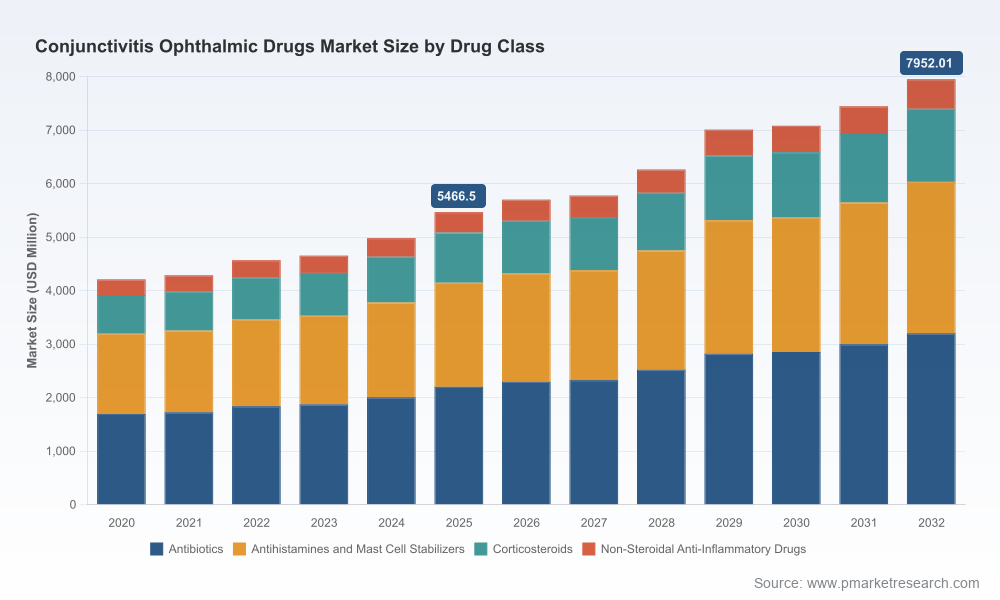

PW Consulting’s newest market study on the Worldwide Conjunctivitis Ophthalmic Drugs Market provides a decision-grade view of an established yet rapidly evolving therapeutic area. The market has expanded steadily through the 2020–2025 base period, rising from roughly USD 4.2 billion in 2020 to about USD 5.47 billion in 2025. Our forward-looking scenario analysis shows the market continuing to grow at a compound annual growth rate (CAGR) of 5.51% across the 2026–2032 forecast window, reaching approximately USD 7.95 billion by 2032. These headline metrics reflect durable demand driven by allergy prevalence, continued use of topical anti-infectives, lifecycle activity, and incremental therapeutic innovation (formulations, inserts, and delivery systems).

Worldwide Conjunctivitis Ophthalmic Drugs Market

Timing and resource allocation: The market’s mid-single-digit CAGR signals attractive, predictable growth for portfolio managers and business development teams. Companies must choose whether to invest in scale (manufacturing, distribution) or differentiation (novel formulations, device-enabled delivery) — and our scenario work quantifies the trade-offs.

Worldwide Conjunctivitis Ophthalmic Drugs Market

Risk management against generics: Generic entrants and off‑patent competition are a continuous theme. Our dynamics section assesses how recent generic launches and portfolio expiries are reshaping price corridors and uptake curves, enabling you to model margin erosion windows and defense strategies.

Worldwide Conjunctivitis Ophthalmic Drugs Market

Regulatory and reimbursement vectors: The report synthesizes regulatory approvals, labeled pediatric constraints, and reimbursement patterns that materially affect launch sequencing and expected uptake, particularly for device-based therapies and specialty formulations.

Historical sales trajectory (2020–2025) demonstrates a resilient market foundation with steady incremental growth led by allergy-related therapies and sustained demand for anti-infectives. The 2026–2032 forecast—anchored on a 5.51% CAGR—reflects a blend of continued branded innovation, measured uptake of drug-delivery technologies, and pricing pressure from generics. These macro assumptions are underpinned by demographic trends, seasonal allergy cycles, and secular improvements in diagnosis and access to care.

Innovation beyond active molecules: Inserts, sustained-release systems and preservative-free formulations are emerging as differentiators. Clinical and commercial considerations—such as insertion procedures in pediatric populations and reimbursement coding—determine which delivery innovations will scale.

Generics and API supply: Generic launches have accelerated in the recent past, and API supplier ecosystems for core actives (e.g., anti-allergy and anti-infective APIs) are well established. Companies must balance cost advantages of outsourcing with the operational risks of concentrated API suppliers.

Moderate market concentration: Top-tier incumbents capture a significant share of market value, but the field is not closed. Our concentration metrics show a market with clear leaders but room for challengers, niche specialty plays, and targeted M&A to shift competitive positions.

Regulatory nuance: Recent approvals and label changes (including pediatric indications and device labels) create both opportunity and constraint. For example, intracanalicular inserts that address ocular itching must account for practical limitations around pediatric insertion and corresponding reimbursement rules.

The competitive picture combines large multi‑therapy players, ophthalmology specialists, and aggressive generic houses. Our competitive intelligence profiles the strategic posture, product strengths, and likely next moves of leading companies to help you anticipate share shifts and competitive responses.

Alcon Inc. (Geneva, Switzerland; https://www.alcon.com) — Strong in branded anti-allergy drops with established, convenience-focused formulations that command loyalty; a continued focus on differentiation through dosing frequency and tolerability is apparent.

Bausch + Lomb / Bausch Health (Laval, Canada; https://www.bausch.com) — Broad ophthalmic portfolio across anti-allergy, anti-inflammatory and anti-infective categories; defensive lifecycle management around preservative-free claims is a core tactic.

AbbVie / Allergan (North Chicago, USA; https://www.abbvie.com) — Deep ophthalmic heritage with allergy-focused assets; capability to combine commercial scale with targeted clinical programs.

Novartis AG (Basel, Switzerland; https://www.novartis.com) — Global reach and historical product family in ophthalmology that can be leveraged for geographic relaunch and formulation upgrades.

Santen Pharmaceutical (Osaka, Japan; https://www.santen.com) — Specialty ophthalmology focus, including treatments for severe allergic presentations; positions itself in segments where differentiation avoids head-to-head generics competition.

Pfizer Inc. (New York, USA; https://www.pfizer.com) — Leverages anti-infective and anti-inflammatory capabilities with global commercial infrastructure to protect and extend share.

Nicox S.A. (Sophia Antipolis, France; https://www.nicox.com) — Niche innovation with targeted anti-allergy molecules seeking to carve reproducible commercial niches.

Sun Pharmaceutical & Alembic Pharmaceuticals (India; https://sunpharma.com, https://www.alembicpharmaceuticals.com) — Generics and specialty ophthalmic formulations from cost-competitive bases; ready to monetize off-patent windows.

Ocular Therapeutix (Bedford, USA; https://www.ocutx.com) — Developer of intracanalicular inserts; represents the kind of delivery-led innovation that creates new reimbursement conversations and clinical pathways.

Generic and launch activity: Market entry of generics for core anti-infectives and anti-allergy agents has accelerated; recent launches have demonstrable impact on price erosion timelines in our scenarios.

Regulatory approvals: New approvals and label changes (including certain pediatric indications and device-specific labels) create differentiated windows—both enabling and constraining—depending on clinician acceptance and payer coding.

Lifecycle extension and pipeline updates: Expanded approvals for inflammatory indications and new formulation filings suggest companies will increasingly pursue incremental innovations rather than risky blockbuster bets.

Prioritize portfolio clarity: Use the report’s scenario models to classify assets into “scale,” “defend,” and “divest/partner” buckets. This reduces execution risk when pricing pressure materializes.

Defend with differentiation: Fast-follower generics are inevitable for many molecules. Invest selectively in formulation improvements (preservative-free, sustained-release), delivery devices, and convenience benefits that raise switching costs.

Supply‑chain resilience: Secure multiple API sources and consider near-shoring critical intermediates to reduce single-source exposure and short-term disruption risk.

Evidence and access: Build pragmatic real-world evidence packages that address payer questions (e.g., pediatric safety of device-based inserts, comparative convenience metrics) to accelerate reimbursement conversations.

M&A & partnerships: Given the market’s moderate concentration, bolt-on acquisitions and licensing deals—especially in specialty allergy and delivery technology—offer high expected ROI versus greenfield launches.

Robust market sizing and scenario forecasts (historical 2020–2025 base; forecast 2026–2032) with revenue models expressed in USD (Million).

Competitor dossiers and product-mix analysis with assessment of commercial strengths, pipeline catalysts, and vulnerability to generics.

Regulatory and reimbursement playbooks tailored to regional variations (with practical checklists for launch teams and health-economics input templates).

Commercial playbooks for market-entry, pricing, and go‑to‑market sequencing—built from clinician interviews, payer conversations, and launch case studies.

Supply‑chain mapping, API risk assessments, and manufacturing optimization frameworks designed for quick operational execution.

Interactive Excel models and sensitivity analyses for executive use; tailored buy-side briefings and scenario walkthroughs are available on request.

The intelligence presented here highlights the market’s trajectory, competitive dynamics, and high-impact operational levers. To preserve the strategic value of the full study and to support actionable vendor discussions, granular cell-level subsegment tables (detailed region/application dollar splits and disaggregated pricing trajectories) are intentionally summarized rather than reproduced in this release. Clients seeking the complete set of subsegment figures, downloadable models, and bespoke scenario runs should refer to the full report package available from PW Consulting.

For executives and investors positioning for 2026, conjunctivitis ophthalmic drugs represent a market with predictable headline growth, ongoing innovation opportunities, and distinct commercial and operational risks. Whether your priority is defending a branded franchise, entering with a cost-competitive generic, or advancing a delivery innovation, the right mix of clinical evidence, supply-chain resilience, and reimbursement strategy will determine outcomes. PW Consulting’s study translates these complexities into executable choices—without revealing every granular cell—so teams can prioritize tactical action immediately and acquire the detailed subsegment intelligence needed to execute at scale.

For access to the full dataset, detailed subsegment numbers, interactive forecasting models, and tailored advisory support, please consult the PW Consulting report distribution page.

For detailed analysis of this topic, please visit the official page:Worldwide Conjunctivitis Ophthalmic Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com