Biotechnology Market: Size, Share, and Future Growth

Other |

2026-05-06 09:53:15

PW Consulting’s latest market intelligence—the Worldwide Wood Foam Market report (base year 2025, forecast 2026–2032)—translates an emergent material renaissance into a pragmatic roadmap for executives, investors, and policy strategists. As demand for bio-based, circular alternatives intensifies, wood-derived foams are graduating from pilot projects to commercial supply chains. This briefing highlights the report’s strategic value for 2026 decision-making while preserving the detailed subsegment matrices and proprietary model outputs for subscribers.

Worldwide Wood Foam Market

Market trajectory: Global wood foam revenue expanded from USD 41.25 Million in 2020 to USD 78.5 Million in 2025, and PW Consulting’s model projects continued acceleration to USD 247.74 Million by 2032. The compounded annual growth rate (CAGR) across the forecast window is 17.84%.

Worldwide Wood Foam Market

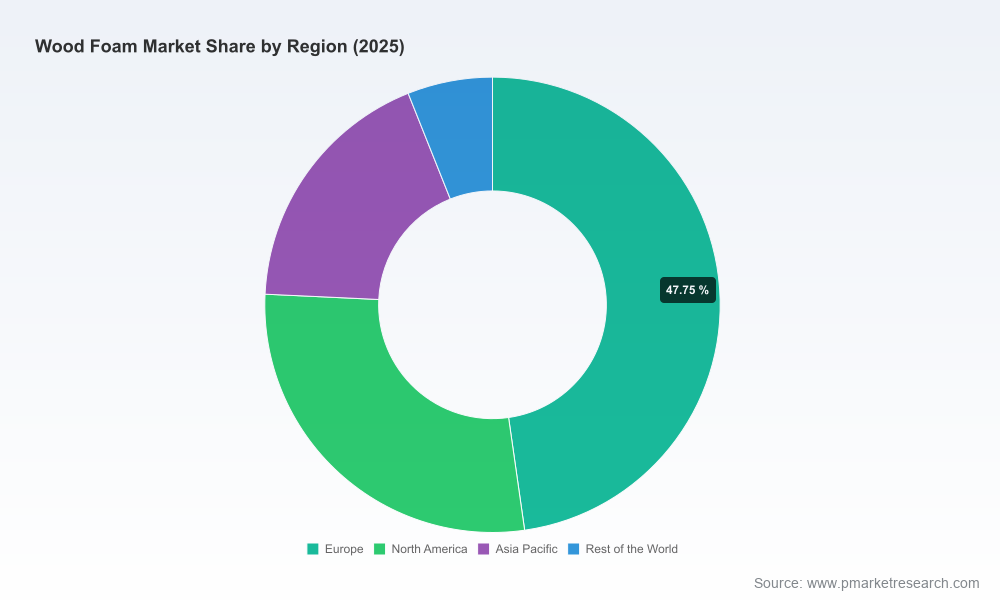

Market structure: The sector is materially consolidated—our concentration analysis shows a top-three share consistent with mid‑60s and a top-five presence approaching the high 70s—signaling both scale advantages for incumbents and attractive niches for focused entrants.

Worldwide Wood Foam Market

Commercial inflection: Several producers and technology centers have validated pilot and early commercial-scale production in 2024–2025, transitioning wood foam from R&D curiosity to manufacturable, supply-chain-ready material.

Two concurrent dynamics make 2026 a decision point rather than just another planning milestone. First, regulatory pressure—particularly packaging and waste policies in major markets—has crystallized corporate procurement mandates that favor fiber-based, curbside-recyclable solutions. Second, commercial capacity additions and partnerships have shortened the time-to-market for wood-foam-based replacements of certain polymer foams. The combination raises the opportunity cost of inaction: waiting risks being locked out of low-carbon supply chains and missing premium contracts that now require demonstrable circularity credentials.

We make full use of longitudinal, revenue-based projections to quantify risk-adjusted opportunity. The market’s near-term base (2025) and our 2026–2032 forecast envelope underpin scenario-based investment returns, capital-budgeting matrices, and payback sensitivity for retrofit and greenfield manufacturing options. To preserve the report’s role as the authoritative source, detailed regional and application splits, price-curve assumptions, and segmented elasticities are available only in the full report—this is intentional: the granular segment tables are the decision-grade inputs your M&A, procurement, and product teams will want on hand.

Actionable demand models: Revenue forecasts by scenario (base, accelerated-adoption, and constrained-adoption) with sensitivity to feedstock cost, energy price shocks, and regulatory adoption timing.

Cost-to-serve and margin maps: Facility-level CAPEX/OPEX templates, break-even thresholds for flexible versus rigid production, and labour/automation trade-offs.

Supply-chain playbooks: Sourcing strategies for sustainably managed wood fiber, co‑processing pathways, secondary logistics, and recommendations for integration with existing paper/cardboard recycling streams.

Commercial go-to-market blueprints: Positioning, pricing, channel segmentation, distributor agreements, and sample RFP language for procurement teams seeking certified circular materials.

M&A and partnership frameworks: Target screening criteria, valuation multipliers used in our model, integration risks, and a checklist for technology licensing or joint-venture due diligence.

Regulatory compliance matrix: Mapping of current and near-term policies—especially EU Packaging & Packaging Waste Regulation (PPWR)—to product attributes and labelling/claims validation steps.

Case studies and technology roadmaps: Commercialization case narratives (pilot-to-scale timelines), performance benchmarking (thermal, acoustic, cushioning), and an R&D investment prioritization schedule.

The market combines industrial producers, research institutions, and specialized converters/distributors. Key strategic takeaways for 2026 planning:

Incumbent industrialization: Established players with vertically integrated cellulose expertise are moving first. Their advantage lies in feedstock access, supplier relationships, and existing packaging sales channels—critical for rapid commercialization and scale economics.

Research-to-manufacturing translation: Institutes that have de-risked production processes (for example, foaming wood fiber suspensions without petrochemical additives) are accelerating time-to-scale by licensing or partnering with converters. This reduces technical uncertainty for investors but raises the premium on licensing terms and IP governance.

Distribution and conversion specialists: Converters and regional distributors that can supply finished parts, punched components, and retrofit packaging designs are important go‑to‑market allies. Their role in qualification cycles with OEMs is often the path to repeat commercial demand.

Our competitive profiles analyze capability clusters—product IP, feedstock control, production footprint, and channel reach—and translate those into tactical recommendations for potential partners, acquisition targets, or defensive strategies.

Product commercialization progress: Leading industrial suppliers have reported successful pilot-scale runs and continued commercial availability of fiber-based foam product lines—evidence that substitution of certain polymer foams in protective packaging is now commercially viable.

Capacity dynamics outside the immediate wood-foam cohort: Related investments in foam manufacturing elsewhere (for example, expansions of molded urethane capacity) demonstrate that overall foam demand growth is prompting incumbents to strengthen supply security, which can influence contract timing and pricing pressure for wood‑based alternatives.

Two structural factors define the runway for wood foam adoption:

Policy acceleration: Packaging waste regulations that incentivize recyclable fiber-based materials are shifting buyer specifications and shortening qualification cycles for suppliers that can demonstrate integration into existing paper/cardboard recycling systems.

Feedstock provenance: The sector’s environmental narrative depends on demonstrable sustainable sourcing from managed forests and processes that avoid petrochemical additives. Producers and technology licensors that secure verified chain-of-custody and low-carbon logistics will capture a price premium and reduce procurement friction with corporates pursuing Scope 3 reductions.

PW Consulting recommends a tailored three-track approach depending on your starting position:

For manufacturers and converters: pilot with clear commercial KPIs, secure feedstock agreements with flexible volume clauses, and invest in modular production lines to de‑risk capacity expansions.

For brand owners and OEMs: run parallel qualification streams—one fast-track for high-value protective applications and one exploratory program for lower-margin volume uses—while embedding recyclability metrics into supplier scorecards.

For investors and PE: prioritize targets with defensible IP, existing offtake channels into packaging or insulation markets, and proven pilot-to-scale pathways; apply scenario-based valuation that reflects regulatory timing risk.

Data-driven projection model calibrated to observed commercial rollouts and verified capacity announcements.

Operational templates and risk matrices translated into executable milestone plans—so teams can move from strategy to procurement, pilot, and scale without repeated rework.

Competitive diligence: focused profiles and playbooks for the leading technology developers, converters, and distributors—identifying where to partner and where to differentiate.

This briefing is a strategic trailer: it outlines the primary market forces, the commercial inflection points for 2026, and the practical decision frameworks that the full report expands into tactical deliverables. For the segment-level demand curves, regional allocation matrices, product-type economics, and the complete set of supplier diligence appendices, please consult the full Worldwide Wood Foam Market report. PW Consulting offers tailored briefings and scenario workshops to translate this intelligence into investment memos, procurement specifications, or M&A playbooks—bookable through our client services team.

In an ecosystem where regulation, sustainability, and supply reliability converge, 2026 will separate opportunistic pilots from durable commercial platforms. Use the right intelligence to make that distinction—our report gives you the model, the operational templates, and the strategic context to make 2026 the year you either secure a leadership position in wood-foam value chains or miss the contract cycles that follow.

For detailed analysis of this topic, please visit the official page:Worldwide Wood Foam Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com