One-Box Testers Market Driven by Growth in 5G, IoT, and Next-Generation Communication Technologies

Drinks |

2026-06-24 06:18:31

PW Consulting's latest industry study on the Worldwide Metal Facade Cladding Market provides a forward-looking intelligence package designed to inform boardroom decisions throughout 2026. Using 2025 as the analytical base year, our model projects the global market to grow at a compound annual growth rate (CAGR) of 5.42% across the 2026–2032 forecast window. In monetary terms, the market reached approximately USD 24.6 billion in 2025 and is forecast to expand toward a mid-term horizon exceeding USD 35 billion by 2032. These headline metrics underwrite a structurally growing market driven by regulatory tightening, urbanization of high-rise building stock, and increasing demand for durable, low-maintenance building envelopes.

Worldwide Metal Facade Cladding Market

Senior executives, corporate strategy teams, and private equity sponsors face three immediate imperatives in 2026: (1) protect margins in an environment of volatile raw material pricing; (2) align product portfolios with accelerating energy-efficiency and fire-safety standards; and (3) position supply chains for resilience amid trade-policy and input-cost shifts. Our report translates market-scale forecasts into operational decision levers—pricing shock scenarios, procurement hedging templates, and go-to-market playbooks—so leaders can convert macro momentum into defensible, near-term commercial wins without overcommitting capital to low-return segments.

Worldwide Metal Facade Cladding Market

Raw material pressure and pricing transmission: The market is experiencing renewed input-cost volatility. Notably, a leading architectural sheet supplier announced a price increase on aluminum products effective January 1, 2026, and industry data registered a material uptick in aluminum sheet prices in North America in late 2025. These trends are uneven across suppliers and geographies, creating windows for price recovery for vertically integrated manufacturers and margin compression risks for downstream fabricators that lack passthrough mechanisms.

Worldwide Metal Facade Cladding Market

Regulatory acceleration toward energy and safety: Tighter building energy codes, reinforced by instruments such as LEED, BREEAM, and revisions to the EU Energy Performance of Buildings Directive (EPBD), are increasing the premium on high-performance cladding systems. At the same time, fire-safety concerns in high-rise construction continue to drive specification changes favoring non-combustible or enhanced fire-resistant metal solutions. These regulatory vectors are shifting procurement criteria from lowest initial cost to total lifecycle value.

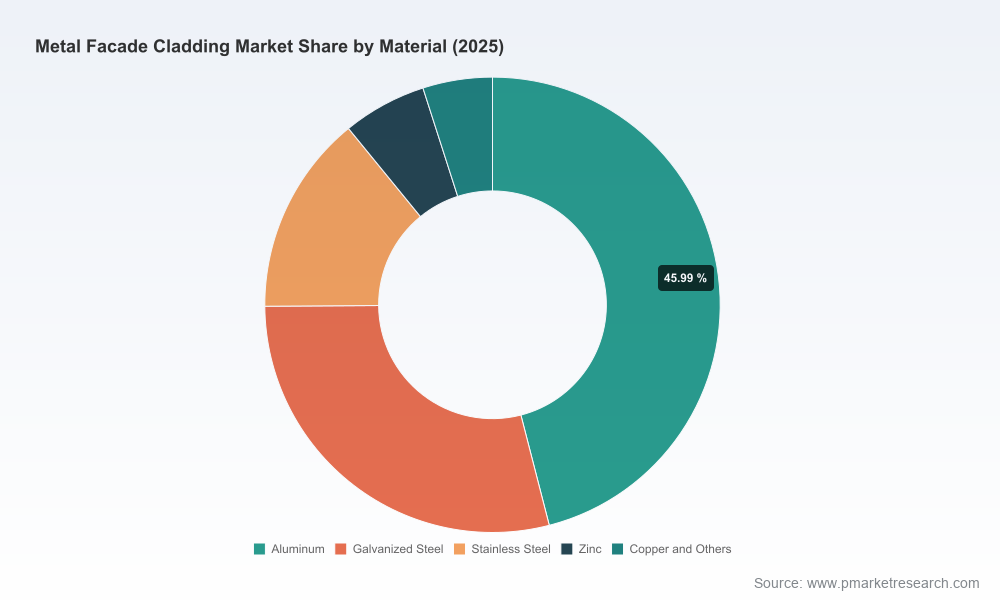

Product differentiation through performance and aesthetics: Metal facades remain a preferred route for combining architectural aesthetics, long service life, and low maintenance. Manufacturers with proprietary coatings, insulated panel systems, or composite material capabilities are increasingly able to command specification preference—provided they can validate performance in third-party testing and compliance frameworks.

Fragmented competitive environment: Market concentration remains low by industrial benchmarks, with the leading consolidated groups accounting for a modest share of global revenue. This fragmentation sustains opportunities for regional champions, specialty fabricators, and new entrants focused on niche applications (e.g., high-end architectural façades or rapid-install modular panels).

Event-driven innovation and visibility: Industry forums and exhibitions (e.g., METALCON and other trade events) continue to serve as accelerators for technology adoption and supply-chain partnerships; market participants should use 2026 trade events as targeted opportunities for product launches and specification engagement.

The market comprises a mix of multinational material producers, composite and panel specialists, and bespoke fabricators. Key corporate archetypes we profile include:

Kingspan Group — a leader in insulated metal panels and high-performance cladding systems, with explicit emphasis on energy efficiency and large-format applications; their offerings are positioned for commercial and industrial envelopes where thermal performance is a procurement priority.

Alucobond (3A Composites) — an established player in aluminum composite panels (ACP), focused on lightweight, customizable, and fire-tested solutions for contemporary architecture.

Arconic Corporation — a supplier of aluminum composite and solid metal cladding systems engineered for high-rise façades with advanced surface coatings and structural performance attributes.

Tata Steel Limited and BlueScope Steel — steel-based manufacturers offering pre-finished and coated steel systems that compete on durability, price, and large-volume supply capability, particularly in regions with steel-centric construction.

ALPOLIC (Mitsubishi Chemical), Alucoil, and Reynaers Aluminium — companies that bridge material innovation and architectural system integration, providing composite materials and curtain wall systems with emphasis on aesthetics and specification-led adoption.

Regional and specialist fabricators (e.g., PAC-CLAD, Zahner, Americlad) — these firms excel in architectural customization, rapid fabrication, and single-project execution for premium or complex installations.

For 2026 planning, the competitive implication is clear: scale and breadth favor multinational manufacturers in commoditized product lines, while agility and specialization remain potent advantages in high-end architectural and retrofit segments. The low three- and five-firm concentration metrics imply continued M&A runway for strategic consolidators seeking improved procurement leverage or expanded geographic reach.

Beyond headline forecasts, this report is an operational toolkit tailored for executives who need to act in 2026. Deliverables include:

Financial-grade market model with scenario toggles: run sensitivity analyses across raw-material price shocks, regional construction cycles, and regulatory adoption curves.

Procurement playbook: passthrough clauses, indexation templates, and hedging strategies for aluminum and coated steel inputs—designed to be integrated into supplier contracts by Q2 2026.

Product roadmap framework: prioritization matrix for investing in fire-resistance upgrades, thermal insulation enhancements, and coating innovations based on return-on-capability metrics.

Commercial go-to-market playbooks: specification engagement scripts for architects and contractors, margin-preservation pricing frameworks, and channel partnership models for accelerating adoption.

M&A screening and value-creation checklists: candidate profiles, synergies quantification templates, and integration milestones designed for strategic and financial buyers.

Regulatory tracker and compliance impact assessments: scenario maps showing likely specification changes from energy-code updates and fire-safety mandates and their impact on product acceptance.

Executive dashboards and data packs: downloadable time-series datasets, index-linked pricing histories, and a consolidated vendor intelligence matrix to support rapid due diligence.

Lock in procurement mechanisms that preserve gross margin: implement indexed contracts and conditional pass-through clauses for key inputs; deploy a short-term hedging strategy where feasible and focus spot-buy discipline on volatile inputs.

Prioritize product compliance upgrades that unlock specification premiums: accelerate testing and certification for fire-resistant and high U-value (thermal) systems to capture spec-driven demand as codes tighten.

Pursue targeted vertical integration or strategic alliances: secure upstream supply for key coated metals or partner with composite producers to mitigate input risk and control quality for high-value façade solutions.

Differentiate through systems and services: bundle design, prefabrication, and installation support to move away from pure commodity supply and capture lifecycle value for owners and developers.

Use M&A selectively to acquire capability or geographic footholds: in a fragmented market, bolt-on acquisitions can rapidly deliver scale, diversify product portfolios, and enhance procurement leverage—prioritize targets with accredited production and established architectural relationships.

Invest in digital sales and specification tools: deploy BIM-compatible product libraries, color/finish visualizers, and performance calculators to shorten specification cycles and increase share of architect-led projects.

Engage early on sustainability narratives: quantify whole-life carbon and maintenance savings and translate them into compelling commercial cases for building owners and portfolio managers focused on ESG performance.

Key upside scenarios include accelerated retrofit activity in mature markets and faster-than-expected adoption of high-performance envelope standards. Downside scenarios center on sustained input-cost spikes without commensurate passthrough mechanisms, or abrupt slowdowns in commercial construction volumes in select regions. Our report provides scenario runs with probability-weighted outcomes to support capital allocation and contingency planning.

This briefing highlights the strategic contours of the market and the actionable levers available to executives in 2026. The full PW Consulting report contains the granular datasets, scenario models, supplier scorecards, and integration playbooks required to operationalize these recommendations—along with a gated annex that discloses regional and application-level detail, supplier-by-product mapping, and downloadable financial models. We designed that level of granularity to support transaction diligence, procurement negotiations, and product development roadmaps; it is intentionally reserved for the full report to preserve commercial confidentiality and to ensure that subscribers and clients derive exclusive competitive advantage.

To schedule a briefing with our lead industry analysts or to access the complete dataset and model package, visit the PW Consulting report page and request the 2026 Strategic Briefing add-on. Use the insights within to convert the market’s structural growth—backed by a projected 5.42% CAGR—into defensible value creation across your organization.

For detailed analysis of this topic, please visit the official page:Worldwide Metal Facade Cladding Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com