Custom Sushi Boxes for Stylish Food Packaging

Other |

2026-04-14 10:34:54

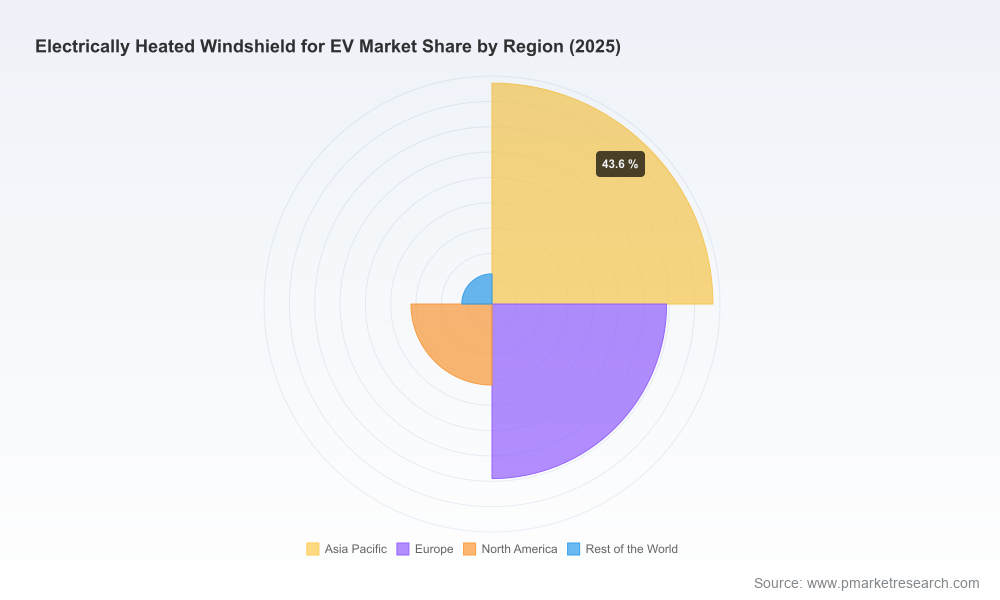

PW Consulting’s new market study on Electrically Heated Windshields for Electric Vehicles (EVs) distills seven years of historical performance and a clear, data-driven forecast to guide corporate strategy in 2026 and beyond. The market has moved from nascent OEM experiments into a commercially material technology, with aggregate market value growing from the low hundreds of millions in 2020 to roughly USD 1.2 billion in 2025, and a projected expansion—at a compound annual growth rate (CAGR) of approximately 14.12%—toward the multi-billion-dollar range by 2032. For OEMs, Tier 1 suppliers, materials providers and system integrators, the decision window opening in 2026 is less about if to invest and more about how and where to allocate capital, R&D and partnership resources to capture durable advantage.

Electrically Heated Windshield for EV Market

Electrification maturity: As EV architectures stabilize and 48-volt subsystems gain traction, electrically heated windshields move from niche option to mainstream thermal-management component. The technical case—reduced HVAC energy draw, faster defogging/defrosting and integration with ADAS—now aligns with fleet-level performance and warranty expectations.

Electrically Heated Windshield for EV Market

Cost-performance convergence: Recent advances in conductive coating, fine-wire embedding and pulsed electro-thermal approaches have shifted the tradeoffs between visible wire aesthetics, optical performance and energy consumption. 2026 is the year many programs will decide whether to adopt next-generation coatings, refine wire geometries, or license pulse-based systems.

Electrically Heated Windshield for EV Market

Value chain consolidation: Market concentration metrics indicate a consolidated supplier base where a small group of specialists control the majority of supply. This raises strategic questions around supplier risk, co-development agreements, and vertical integration for system-critical components like PVB interlayers and coated glass.

The PW Consulting study is structured for decision makers who need both high-level strategy and immediately deployable tools. Key deliverables include:

Market sizing & forecast model (2020–2032): Dynamic scenario layers allow users to test adoption curves tied to EV penetration, regional regulation timelines and power-architecture adoption (12V vs 48V vs HV).

Technology roadmap and comparative ROI: A rigorous, side-by-side evaluation of conductive invisible coatings, fine-wire heating, and pulsed electro-thermal deicing (PETD) approaches—covering optical performance, durable lifetime, energy draw, manufacturing complexity and cost-to-vehicle.

Supplier due-diligence templates: A matrix for sourcing decisions that factors capacity, IP ownership, testing credentials, ADAS compatibility and pricing power—designed to support RFPs and commercial negotiations.

Integration checklists for OEMs and Tier 1s: Practical engineering specifications for electrical interfacing (including 48V considerations), EMC and safety testing, camera and sensor window treatments, and calibration protocols for ADAS sensors behind heated glass.

Raw-material sensitivity and procurement playbook: Scenario analyses for PVB/PVA price volatility, preferred sourcing geographies, and hedging strategies to protect bill-of-materials exposure.

Regulatory and standards mapping: Actionable compliance pathways for automotive glazing standards (including optical clarity, impact resistance and electrical insulation), with recommended timing for type-approval milestones.

Go-to-market and product-launch playbooks: Pricing levers, warranty structures, and pilot-program templates to accelerate adoption with fleets, luxury and mainstream EV programs.

The competitive field combines traditional glass giants, vertically integrated glass manufacturers, specialist thermal startups and OEM-led innovation pilots. Our assessment highlights distinct strategic postures:

Established glass manufacturers (global incumbents): These players leverage scale, longstanding automotive certifications, and deep OEM relationships to embed heating functionality within existing product families. Their advantage lies in production capacity, proven lamination capabilities and program management—critical when integrating heating elements without compromising safety glazing standards.

Tier 1 and materials-focused specialists: Firms focused on conductive coatings and advanced interlayers can offer lower visual impact and better acoustic/thermal synergies. Their investments in coating stacks and proprietary conductive films make them attractive partners for OEMs prioritizing aesthetics and sensor compatibility.

Technology disrupters: Startups pioneering pulsed electro-thermal deicing demonstrate dramatic energy reductions and fast clearing times. These approaches decouple heating performance from continuous power draw, presenting an attractive option for range-conscious EV platforms and commercial vehicles with frequent start-stop winter cycles.

Our competitor dossiers synthesize product performance, IP posture, recent test outcomes and partnership activity—enabling procurement teams to shortlist suppliers based on product fit, lead times and integration complexity rather than brand alone.

Pulsed electro-thermal deicing (PETD) progress: Public testing shows PETD systems clearing windshields in roughly one minute using single-digit percentages of the energy of HVAC-based defrost cycles. For EV programs where every watt-hour matters, this changes the calculus for thermal management tradeoffs and battery sizing.

48-volt demonstrations: OEM-led 48V metal-coated heated glass showcases faster frost clearance at lower impact to the high-voltage battery, translating into clearer pathways for adoption in mass-market vehicle architectures that embrace multi-voltage electrical systems.

Raw-material dynamics: PVB interlayers and upstream PVA feedstock have experienced price and availability variability. These fluctuations directly affect manufacturing economics and favor suppliers with diversified procurement and backward integration strategies.

Standards & ADAS convergence: Regulatory and safety glazing standards remain non-negotiable. Heated windshields must now satisfy optical clarity and electrical safety while supporting camera and sensor calibration—making third-party validation and early-stage system-level testing mandatory for program timelines.

Adopt a bifurcated sourcing strategy: Secure a capacity partner from the incumbent glass base for program stability while engaging a technology specialist or PETD provider for pilot programs that target energy optimization and sensor-friendly solutions.

Invest in electrical-architecture alignment: Programs adopting 48V subsystems should fast-track thermal integration studies now; delays will create costly retrofits and slower time-to-market for winterized EV derivatives.

Prioritize ADAS-friendly heating solutions: Optical uniformity and minimal sensor distortion are mission-critical. Insist on camera/sensor calibration data and lifetime optical testing as part of supplier contracts.

Lock in raw-material strategies: Build optionality around PVB sourcing and consider pre-competitive initiatives to stabilize input supply across key programs.

Design warranty and diagnostic features: Because any heating element failure impacts safety and customer satisfaction, define clear warranty metrics and over-the-air diagnostic pathways for heating-system faults.

This report translates technical complexity into financial and operational choices. Boards and executive teams can use our forecast scenarios and supplier scorecards to set capital allocation, partnership and M&A priorities for 2026. Whether the goal is to secure supply for a global EV platform, to license low-energy heating technology, or to acquire upstream materials capability, our study provides the risk-adjusted framework and the negotiation playbooks necessary to execute quickly and defensibly.

The executive brief above highlights core trends and recommended actions while intentionally omitting detailed regional and application segment breakdowns to preserve the report’s strategic value. The full PW Consulting study includes granular regional forecasts, technology-specific unit economics, supplier benchmarking tables and downloadable models to run custom scenarios aligned to your fleet profile and program timelines.

For procurement teams, R&D leaders and corporate strategists preparing program approvals in 2026, this is the moment to move from exploratory pilots to binding supplier commitments and architecture-level decisions. Visit our report page to access the full dataset and the proprietary models that underpin the analysis—so your team can convert insight into market-leading execution.

For detailed analysis of this topic, please visit the official page:Electrically Heated Windshield for EV Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com