Worldwide Topical Dispenser Market — Strategic Preview for 2026 Decision-Makers

Executive summary

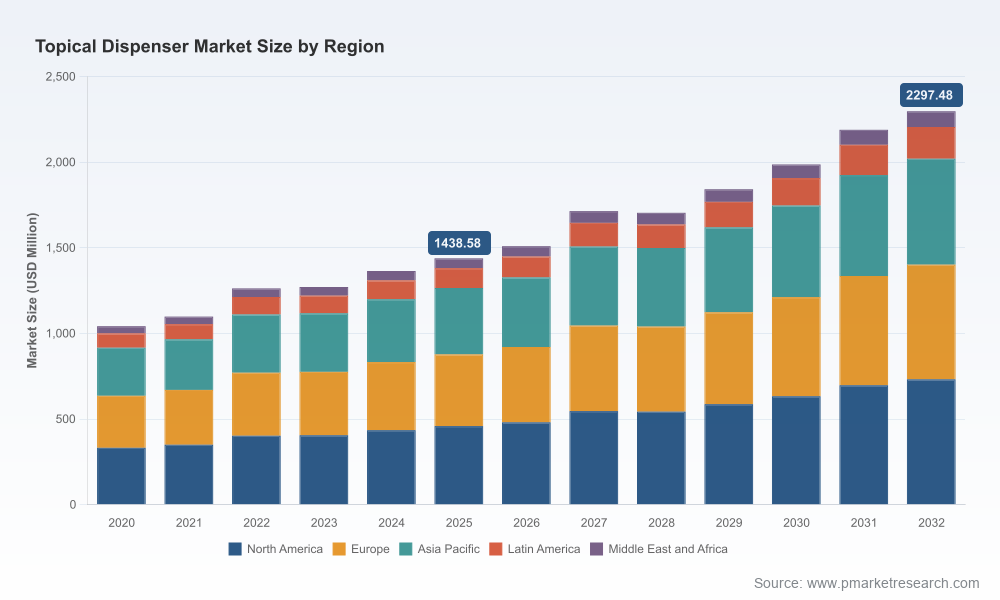

As healthcare delivery moves closer to the patient and compounding pharmacy workflows scale, topical dispensers have become a strategic product category at the intersection of drug-device engineering, regulatory risk management, and patient adherence economics. PW Consulting’s new market study — covering the historical period 2020–2025 and providing a granular forecast through 2032 — shows that the global topical dispenser market has established a resilient growth trajectory. Total market value expanded from just over USD 1.0 billion at the start of the decade to approximately USD 1.44 billion in our base year (2025). Under our central scenario, the market is expected to grow to roughly USD 2.30 billion by 2032, representing a compound annual growth rate (CAGR) of 6.92% across the 2026–2032 forecast window.

Worldwide Topical Dispenser Market

Why this matters to executives planning for 2026

2026 is a make-or-break inflection year for companies operating in or adjacent to topical dispensers. Three converging forces drive this urgency:

Worldwide Topical Dispenser Market

- Regulatory clarity is tightening for device-drug combination products, and manufacturers that can demonstrate design controls, dose uniformity, and ISO 13485-aligned quality systems will avoid costly rework and speed time-to-market.

- Payer and provider procurement behavior is shifting toward measurable outcomes: devices that demonstrably reduce dosing error, contamination risk, and waste win formulary and purchasing preference.

- Consolidation and specialization among suppliers are accelerating. Our concentration metrics indicate a market that is neither fully fragmented nor dominated by a single cluster — a landscape that rewards focused M&A and partnership strategies.

Market snapshot (high-level)

Key macro takeaways from the study:

Worldwide Topical Dispenser Market

- Robust historic growth from 2020–2025 established a base market exceeding USD 1.4 billion in 2025.

- Under our baseline forecast, the market expands at a 6.92% CAGR through 2032, reaching approximately USD 2.30 billion.

- Market concentration is moderate: the largest three firms account for roughly 38.5% of value, and the top five about 52.1%, indicating meaningful room for competitive disruption, niche leadership, and consolidation plays.

Dynamics and drivers: where the growth is coming from (strategic view)

Our analysis identifies four durable drivers shaping demand and supplier strategies through 2026 and beyond:

- Precision dosing and compounding efficiency. Metered-dose mechanisms and dial-click designs that ensure dose uniformity are increasingly important for compounding pharmacies and prescribers concerned with therapeutic consistency and liability. Independent evaluations cited in product literature continue to show performance differences between metered-dose applicators and traditional airless pumps, and procurement teams are starting to demand third-party dose-uniformity evidence.

- Clinical and patient-centric imperatives. Products that reduce contamination risk (via airless or sealed reservoirs), improve adherence (clear dosing feedback), and support specialty topical biologics and advanced formulations are capturing higher willingness-to-pay among providers and patients.

- Regulation and quality infrastructure. Topical adhesives and dispenser devices that claim clinical indications face device classifications and premarket pathways — for example, certain topical skin adhesives are regulated as Class II devices requiring 510(k) clearance. ISO 13485 compliance is effectively table stakes for suppliers pursuing institutional channels or regulated indications.

- Reimbursement friction points. Not all topical therapeutics or their applicators fall neatly into existing benefit categories. Our regulatory and reimbursement briefing notes, including the latest payer positions, find that some topical products do not qualify for surgical dressing benefits under current Medicare policy — a nuance that materially affects provider adoption economics for certain use cases.

Competitive landscape — capability maps and implications

We mapped the competitive field by capability rather than by static market share alone, because strategic advantage in topical dispensers derives from product-system integration, regulatory track record, and manufacturing scale. Representative players profiled in the study include:

- DoseLogix (Cordica Medical / TEAM Technologies) — Atlanta, GA. A focused innovator in metered dosing topical applicators (Topi-CLICK family) tailored to pharmacy compounding ergonomics. Recent product activity includes the May 2025 launch of the Topi-CLICK UnoDose optimized for EMP machine compounding, improving both pharmacist workflow and patient dosing consistency.

- Aptar Pharma — global operations headquartered with significant U.S. presence. A leader in semi-solid airless dispensing designs emphasizing product protection and hygiene; strong channel access in pharmaceutical OEM supply.

- Medisca — Montreal with U.S. operations. A compounding-focused supplier of click-dosing and topical dispensers supporting sterile and non-sterile workflows; a bridge between pharmacy customers and device manufacturers.

- SpecializedRx Products and Lucas Packaging Group — U.S.-based specialists offering metered pump dispensers and pen-style dosing devices designed for compounding and retail skin-care segments.

- Porex Corporation and HTI Plastics — component and contract-manufacturing specialists. Porex supplies porous plastics used in reservoirs and wicks; HTI brings ISO 13485-certified injection molding and contract manufacturing capacity, critical for firms needing captive quality systems without building internal tooling for complex polymer assemblies.

- Silgan Dispensing and Health Care Logistics (HCL) — packaging and distribution players with scale in healthcare dispensing solutions, able to support global logistics and regulatory documentation for institutional sales.

Collectively, this mix of innovators, contract manufacturers, and system integrators creates three distinct pathways for market entrants and incumbents: (1) product-led differentiation through dosing accuracy and hygiene, (2) manufacturing-led cost and quality advantage, and (3) channel-led scale via partnerships with compounding pharmacies and pharmaceutical OEMs.

Regulatory & reimbursement considerations (practical checklist)

Manufacturers and investors must internalize a short list of compliance and reimbursement realities before allocating capital or launching product lines:

- Device classification matters. Some topical adhesives and applicators fall under Class II device controls and require 510(k) premarket notification to demonstrate substantial equivalence. Recent clearances in 2025 reaffirm the FDA’s active engagement in this product class.

- Quality system requirements. ISO 13485-aligned processes are essential for suppliers targeting regulated indications or institutional buyers; contract manufacturers should be vetted for certification and design control maturity.

- Dose-uniformity evidence. Clinical and laboratory performance data differentiating metered/dial mechanisms from traditional pumps translate directly into procurement leverage and labeling claims.

- Payer nuances. Some topical therapeutics and their applicators may be excluded from surgical dressing coverage under current Medicare rules, affecting hospital and clinic purchasing economics.

Strategic playbook for 2026

For each stakeholder cohort — OEMs, contract manufacturers, private equity, and compounding pharmacy networks — our report translates macro forecasts and competitive mapping into actionable options:

- OEMs: Invest selectively in metered-dose and click-dial intellectual property, secure ISO 13485-certified manufacturing partnerships, and build clinical/technical dossiers to support premium pricing and 510(k)-ready claims.

- Contract manufacturers: Differentiate through regulatory documentation services, rapid prototyping for polymer assemblies, and scalable clean-room molding to capture spillover demand as OEMs outsource risk.

- Private equity and strategic buyers: Target roll-ups that combine niche dosing technology with distribution reach — our concentration analysis suggests acquisition multiples will be highest for assets that bring both differentiated IP and validated payer pathways.

- Compounding pharmacies and retail chains: Prioritize supply agreements backed by independent dose-uniformity data and streamline in-container EMP compounding compatibility to reduce labor costs and dosing errors.

What’s inside the full PW Consulting report (operationally focused)

The full study is designed as a practical playbook for 2026 planning. Highlights include:

- Market model and scenario analyses (base, conservative, upside) covering 2026–2032 with sensitivity to raw-material inflation, regulatory timelines, and compounding automation adoption rates.

- Competitive capability maps and a vendor selection framework to match needs (e.g., sterile-compounding vs. retail skincare)

- Diligence checklists for ISO 13485, 510(k) readiness, and lab-based dose-uniformity testing protocols

- Go-to-market playbooks for targeting pharmacies, hospital formularies, and consumer channels, including pricing levers and contracting terms

- M&A screening model that scores targets on IP defensibility, manufacturing quality, and channel reach

- Supplementary regulatory and reimbursement briefs (including recent Medicare guidance and device classification summaries) and a timeline of relevant clearances through 2025

In keeping with our “trailer” approach, this press release intentionally presents high-level outcomes and strategic implications while withholding the detailed segment-level tables and proprietary vendor scoring that appear in the full report. These segment and subsegment datasets are a central value proposition of the paid study and are available only in the published report.

Final recommendations for executives

As you shape budgets and product roadmaps for 2026, prioritize three concrete actions:

- Lock in manufacturing options that are ISO 13485-certified and can produce validated dose-uniformity fixtures.

- Commission or acquire third-party dose-uniformity testing for any claimed dosing technology — this is increasingly a de-risking requirement for purchasers and regulators.

- Create a short list of M&A or partnership targets that combine dosing IP with established distribution in compounding or institutional channels.

Accessing the full analysis

PW Consulting’s full Worldwide Topical Dispenser Market report contains the complete data tables, supplier scorecards, and downloadable models needed to operationalize the strategies summarized here. For procurement teams, product leaders, and investors preparing 2026 plans, the report is a compact, action-oriented resource. To request executive briefings or obtain the full dataset and vendor scoring, visit our website or contact PW Consulting’s industry practice leads.

Note: This release references public regulatory and industry sources (including recent device clearances and independent dose-uniformity literature) and selected company disclosures through 2025. Detailed segment-level metrics and proprietary scoring are intentionally withheld from this preview to preserve the report’s core subscriber value.

For detailed analysis of this topic, please visit the official page:Worldwide Topical Dispenser Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com