Anti-Viral Therapeutics Market Intelligence Report: Future Growth Trends and Competitive Outlook by 2031

Health |

2026-05-21 14:11:10

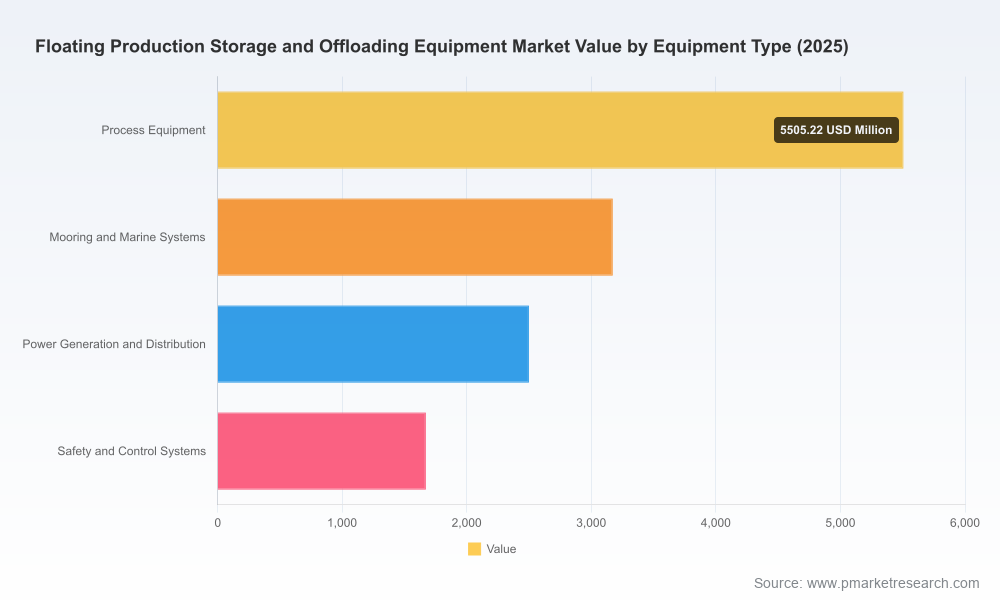

PW Consulting’s latest Worldwide Floating Production Storage and Offloading Equipment Market report (base year 2025, historical 2020–2025, forecast 2026–2032) delivers a decisive lens for executives, investors and project teams who must make capital, contract and supply-chain choices in 2026. The global market for FPSO equipment grew from roughly USD 9.0 billion in 2020 to USD 12.85 billion in 2025 and, at a compound annual growth rate (CAGR) of 7.34%, is forecast to exceed USD 21.1 billion by 2032. These headline dynamics—backed by project wins, operator strategies and supply-chain constraints—create a narrow window in 2026 where timing, partner selection and procurement strategy materially influence project economics and competitive positioning.

Worldwide Floating Production Storage and Offloading Equipment Market

Actionable timing: Our report maps the 2026–2032 tender and delivery cadence for long‑lead items and major equipment packages, enabling CFOs and procurement heads to avoid schedule-driven cost escalation.

Worldwide Floating Production Storage and Offloading Equipment Market

Capital planning precision: We translate the market’s macro trajectory into realistic CAPEX phasing and break‑even thresholds under multiple oil-price scenarios—vital for sanction decisions and portfolio prioritisation.

Worldwide Floating Production Storage and Offloading Equipment Market

Contract model optimization: With lease‑and‑operate arrangements capturing increasing share of awards (notably expanding from the prior five‑year window), the report evaluates the trade-offs between operator CAPEX reduction and long‑term operating cost exposure.

Supply‑chain resilience playbook: The analysis includes yard capacity stress-testing, raw material exposure (in the context of elevated Brent prices), and pragmatic mitigation steps for contractors and operators.

Several structural forces are reshaping FPSO equipment markets in ways that will determine winners and losers in 2026:

Volume and velocity: Following a rebound in awards and project activity, the equipment market is expanding steadily. The projected mid‑term expansion implies continued demand for deepwater and ultra‑deepwater topsides, mooring systems and integrated power solutions.

Operator strategy shift: Turnkey lease‑and‑operate contracts have become the dominant procurement model in the most active basins. This reduces upfront CAPEX for charterers but shifts lifecycle responsibility—and execution risk—to fewer, vertically integrated suppliers.

Regulatory and local content pressure: Pre‑salt programs in Brazil and similar jurisdictional policies typically raise project budgets and complexity while creating sizeable local jobs and supplier opportunities. Effective local‑content planning has moved from “nice‑to‑have” to a precondition for competitive bids.

Decarbonisation and electrification: Major operators are embedding all‑electric topside concepts and emission‑reduction requirements into FIDs, forcing equipment suppliers to accelerate electrification, digital monitoring and energy‑efficiency product lines.

Raw material and price volatility: Elevated oil prices and intermittent supply disruptions have dual effects—improving project economics while increasing input costs and putting pressure on procurement timelines.

The market shows moderate concentration: the top three vendors account for a meaningful share of revenues, and the top five control just over half of market revenue—signalling both scale advantages and persistent opportunities for specialist mid‑tier players. Our competitive review synthesises company strategy, asset footprints and recent developments to highlight capability gaps and bid advantages.

SBM Offshore N.V. (Amsterdam) — Strength: standardized hull platforms and integrated lease/operate models. Recent contractual momentum and a deepwater backlog make SBM a primary counterparty for large lease‑based awards.

MODEC, Inc. (Tokyo) — Strength: EPCI capability for ultra‑deepwater and harsh environments. MODEC’s Guyana wins underscore their tactical fit for large operator programmes seeking turnkey execution.

BW Offshore Limited (Oslo) — Strength: conversion expertise and hybrid newbuild/conversion strategies. BW’s progress on Bay du Nord and related activities highlight the commercial flexibility that operators value for marginal and complex fields.

Yinson & Bumi Armada (Kuala Lumpur) — Strengths: regional agility and growing presence in Brazil and Asia; both are scaling charter fleets and pursuing selective newbuild programmes to capture lease opportunities.

Bluewater, Saipem, TechnipFMC — Strengths: technology niches (turrets, subsea integration, EPCI integration) that make them preferred partners for complex hook‑ups and integrated solutions.

Keppel, Samsung Heavy, HD Hyundai — Strengths: yard capacity and large‑hull fabrication capabilities essential to meeting surges in hull demand, but subject to berth availability and steel supply cycles.

Petrobras & ExxonMobil — As charterers and strategic demand drivers, their contracting choices (e.g., Petrobras’s recent P‑series programme and operator decarbonisation directives, ExxonMobil’s Guyana activity) set the procurement tempo.

Project acceleration: Multiple high‑visibility FIDs and contract awards early in 2025–2026 have compressed the delivery runway for large FPSO programmes, elevating the importance of long‑lead procurement and supplier coordination.

Notable awards and commissioning milestones have both validated demand and highlighted execution risk—operators are moving from FEED to full procurement simultaneously in several basins.

Local content rules and decarbonisation targets are materially affecting tender evaluation criteria and lifecycle cost modelling; the firms that combine compliance capability with cost competitiveness are winning larger, integrated packages.

PW Consulting’s deliverable is structured to support 2026 decisions across corporate, project and procurement teams without requiring readers to mine raw datasets for every judgment call. Key components include:

Market sizing and scenario forecasts (2026–2032) with sensitivity runs tied to oil‑price, capex inflation and local content stressors.

Tender and long‑lead equipment calendar mapped against yard capacity and supplier lead times to flag procurement pinch‑points.

Contract model decision trees comparing lease/operate vs. build/own outcomes over 10–year horizon with NPV, break‑even and contingent liability visualisations.

Supplier scorecards and procurement playbooks—benchmarks for technical capability, execution reliability, local content delivery and commercial flexibility.

Risk matrices covering raw‑material exposure, regulatory change, currency and project delivery; recommended hedges and contracting clauses are included.

Technology and decarbonisation assessment—electric topsides readiness, power‑distribution strategies and emissions reporting implications for financing.

Front‑load long‑lead procurement where possible. With fabrication slots tightening and prices sensitive to material swings, early placement of major equipment avoids tiered premium payments and schedule slippage.

Prioritise integrated partners with demonstrable execution track records in the target basin and with verifiable local‑content delivery plans; the cost of rework or non‑compliance is often greater than the marginal supplier premium.

Model deal structures under both lease and ownership frameworks. Given the rising share of lease‑and‑operate awards, operators should quantify the optionality and contingent liabilities inherent in each path before committing.

Embed decarbonisation requirements into procurement specifications early to avoid retrofit costs and financing constraints later in the asset life.

Use scenario‑based hedging for key inputs and contractually allocate material escalation risk where feasible; incorporate performance‑linked milestone payments to better align contractor incentives with project schedules.

For CFOs, the report’s CAPEX phasing and break‑even sensitivities enable disciplined sanction decisions and capital markets messaging. For procurement and project teams, the long‑lead mapping and supplier scorecards reduce execution risk and bid exposure. For investors and M&A teams, the competitive concentration metrics and strategic positioning of top suppliers illuminate acquisition targets and partnership rationales.

The FPSO equipment market is moving from a recovery phase into a structurally higher activity band. The combination of elevated commodity prices, operator sanctioning activity, evolving contract modalities and regulatory demands creates a year where prompt, well‑structured decisions will capture outsized value and mitigate execution downside. PW Consulting’s report packages the market intelligence, procurement playbooks and competitive diagnostics that executive teams need to make those decisions with confidence.

Access the full report for granular procurement calendars, supplier heatmaps, and downloadable decision tools that are intentionally excluded from this preview.

Contact PW Consulting’s FPSO practice to schedule a tailored executive briefing and a scenario workshop for 2026 planning.

For detailed analysis of this topic, please visit the official page:Worldwide Floating Production Storage and Offloading Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com