Global Styrene Butadiene Rubber (SBR) Market Growing at 6.0% CAGR Through 2034

Other |

2026-07-07 12:41:00

PW Consulting’s latest market intelligence brief, the Worldwide Cosmetic Grade Retinol Market report (base year 2025), delivers an actionable strategic playbook for executive teams planning 2026 initiatives and multi-year resource allocation. Built on an empirical time series (2020–2025) and forward-looking scenarios to 2032, our forecast quantifies a structurally growing market — underpinned by a 6.92% compound annual growth rate through the forecast window — and outlines the commercial, regulatory, and technological vectors that will determine winners and laggards in the retinol value chain.

Worldwide Cosmetic Grade Retinol Market

Timing matters: 2026 will be a reset year for many organizations as regulators, ingredient suppliers, and brand owners digest recent rule changes and reprice risk in formulation and supply. Our report positions senior leaders to act before the market fully reprices.

Worldwide Cosmetic Grade Retinol Market

Opportunity vs. constraint: While consumer demand for clinically effective anti-aging and corrective skincare remains robust, regulatory and labeling constraints are forcing rapid reformulation and messages that materially affect product positioning, shelf assortments, and margin construction. The report quantifies the pace of change and maps tactical levers available to manufacturers and finished-goods brands.

Worldwide Cosmetic Grade Retinol Market

Data-driven prioritization: The report translates aggregate market momentum into priority areas for investment — R&D, manufacturing capacity, supplier partnerships, and route-to-market experiments — with financial projections calibrated to the 2025 market baseline and our 2026–2032 trajectory.

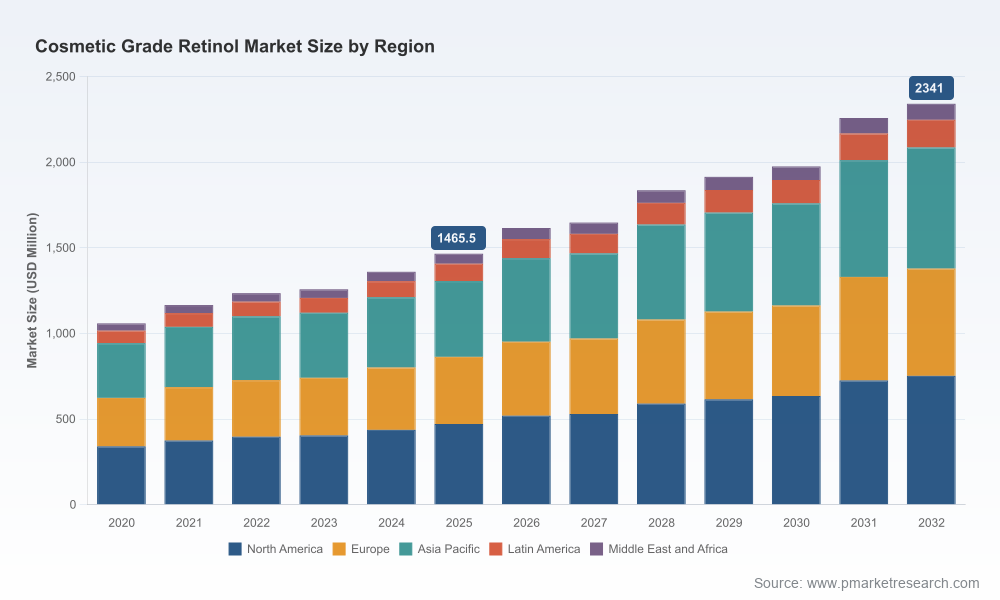

Using 2025 as the analytical anchor, our market system estimates the cosmetic grade retinol market at a mid-single-billion USD annual revenue level in that year (USD, revenue in Million units). From that base, the market is projected to continue expanding at a compound annual growth rate of approximately 6.9% through the end of our forecast period. Near-term demand drivers include sustained consumer preference for clinically validated anti-aging and acne interventions, while medium-term expansion is supported by formulation innovations (stabilized retinol, encapsulation systems, and hybrid retinoid chemistries) and broader penetration into personal care categories beyond face serums.

Market concentration remains meaningfully mid-range: the top three players collectively control a significant but not overwhelming share of global supply, and the top five approach a clear majority position. This structure leaves room for both scalers (global chemical and specialty ingredient houses) and focused innovators (specialty encapsulation providers and regional API producers) to shape competitive outcomes.

Regulatory tightening in critical markets is materially influencing reformulation timelines and labeling strategies. Recent European Commission measures impose explicit limits on retinol and certain esters in cosmetic products and introduce mandatory labeling language about vitamin A content and cumulative daily exposure. These measures have staggered implementation dates that create a defined window for product relaunches, compliant new product introductions, and inventory management.

In the United States, incremental enforcement and compliance expectations under MoCRA — including facility registration, product listing, and forthcoming GMP rules — are elevating operational requirements for both formulators and ingredient suppliers. Brands that delay compliance are increasingly exposed to market access and reputational risk.

Implication for strategy: successful 2026 programs will be those that treat regulatory change as a product-development and go-to-market opportunity — accelerating launches of stabilized, lower-dose, or alternative retinoid systems accompanied by clear labeling and risk communications — rather than as a mere cost of doing business.

The market is shaped by a blend of global chemical majors, specialty formulators, and regional bulk suppliers. Our competitive chapter provides company-level profiles, strategic posture analysis, and scenario-mapped moves for market entry, expansion, or exit. Representative players covered in depth include:

BASF SE (Ludwigshafen, Germany — https://www.basf.com): A global leader that supplies cosmetic-grade retinol and stabilized formulations. BASF’s product strategy emphasizes stability and clean-beauty alignment — exemplified by the launch of a stabilized, BHA/BHT-free retinol grade that addresses both performance and label-conscious positioning.

DSM-Firmenich (Heerlen, Netherlands — https://www.dsm.com): A major supplier of vitamin A derivatives that leans into sustainability and novel dosage forms. Their R&D pipeline and sustainability commitments make them a logical partner for brands seeking traceability and lower-carbon ingredient stories.

Evonik Industries AG (Essen, Germany — https://www.evonik.com): Focused on advanced encapsulated and stabilized retinol actives using proprietary delivery technologies. Encapsulation reduces irritation potential and improves shelf stability — two features that are becoming commercial table stakes.

Croda International Plc (Snaith, United Kingdom — https://www.croda.com): Positions bio-based and sustainable cosmetic ingredients, offering differentiation to brand partners pursuing circularity and renewables-based sourcing.

Regional and bulk suppliers: Laboratories and manufacturers across Europe and China supply high-purity retinol APIs and cost-competitive intermediates that underpin large-scale formulation programs and private-label manufacturing. Their role in global sourcing strategies is indispensable, especially for volume-sensitive categories.

Recent product-level innovation (for example, BASF’s stabilized retinol grade introduced in mid-2023) and proprietary encapsulation technologies (notable from Evonik and other specialty houses) are shifting the basis of competition from basic commodity supply to validated functional performance and supply transparency. Our strategic benchmarks explain how to evaluate supplier claims, verify performance under regulatory constraints, and structure long-term supply agreements that preserve margin and continuity.

Proprietary market model: annualized revenue projections (2020–2032) with base-year reconciliation and scenario toggles for alternative regulatory and demand shocks.

Regulatory timeline and impact matrix: implementation dates, labeling requirements, and recommended compliance checklists for product portfolios, prioritized by commercial exposure.

Supplier risk and resilience toolkit: dual-sourcing templates, qualification checklists, and inventory optimization heuristics for high-volatility feedstocks.

Formulation and R&D playbook: technical summaries of stabilized retinol technologies, encapsulation options, and low-irritation retinoid alternatives — with suggested pilot protocols and comparative performance indicators.

Commercial archetypes and GTM playbooks: retailer and DTC channel strategies that align with dose limits, label language, and consumer safety messaging.

Competitive matrix and M&A scan: strategic fits for vertical integration, bolt-on acquisitions, and partnership opportunities mapped to market concentration metrics and technological competencies.

Prioritize stabilized and encapsulated retinol lines in near-term product roadmaps to preserve efficacy claims while reducing reformulation churn.

Accelerate supplier diversification and qualify at least two independent sources for critical ingredients to mitigate regional supply disruption and price volatility.

Embed regulatory scenario planning into product pipeline gating criteria: require compliance sign-off earlier in development cycles and include label-change contingencies in launch budgets.

Invest selectively in clinical validation and differentiating delivery mechanisms that can command premium pricing in a constrained-dose environment.

Explore strategic partnerships with encapsulation specialists and sustainability-oriented ingredient houses to combine performance claims with credible green credentials.

Adopt an active SKU rationalization program to de-risk inventories that will face near-term reformulation requirements; reallocate working capital to high-return formulary upgrades.

Our report is designed as an execution companion, not a high-level narrative. We combine granular supply-side intelligence, validated pricing scenarios, and a regulatory operations roadmap so that teams can translate strategic intent into 90–180 day action plans. The model and playbooks are delivery-oriented: procurement teams receive contract negotiation templates; R&D gets pilot designs and comparative matrices; commercial leaders get assortment and messaging frameworks tailored to varying dose and label constraints.

This release is intentionally a strategic preview. Core segmentation tables, regional and application splits, supplier-level price curves, and our full scenario model are available in the complete report package. That proprietary content includes the granular subsegment numbers and supplier sourcing maps that commercial teams will use to finalize 2026 budgets and supplier contracts. For organizations that prefer embedded support, we offer tailored workshops and implementation sprints to convert the report’s recommendations into operational milestones.

To request the full report, dataset access, or a bespoke briefing tailored to your organization’s exposure to cosmetic grade retinol, please visit our website or contact PW Consulting’s market analytics team. The window to operationalize a compliant, differentiated retinol strategy is narrow — the firms that move decisively in early 2026 will capture outsized share and margin expansion as markets adjust.

For detailed analysis of this topic, please visit the official page:Worldwide Cosmetic Grade Retinol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com