Poly(Dicyclopentadiene) (PDCPD) Reaction Injection Molded (RIM) Parts Market to Reach USD 718.4 Million by 2034

Networking |

2026-07-01 11:19:12

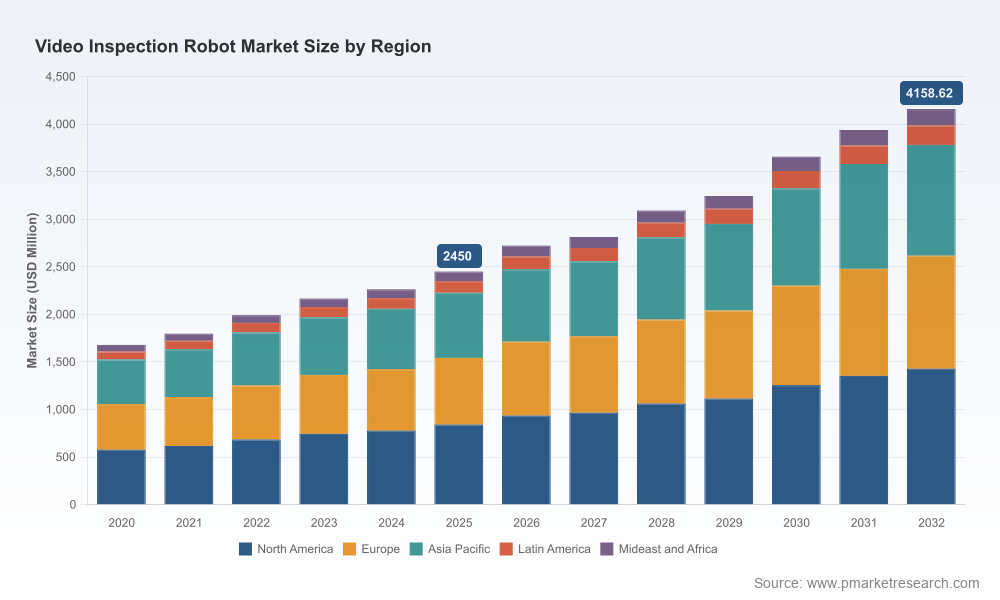

PW Consulting’s latest market research on the Video Inspection Robot Market provides boardrooms, corporate strategy teams, and investment committees with a focused, decision-ready intelligence pack for 2026. Anchored on a 2025 base year, our market model projects continued expansion at a compound annual growth rate (CAGR) of 7.85% across the 2026–2032 forecast horizon. The global market footprint reached roughly USD 2,450 million in 2025 and is modeled to progress materially through the decade, reflecting both cyclical infrastructure spending and durable technology adoption curves.

Video Inspection Robot Market

Capital allocation precision: Procurement and capex cycles for utilities, oil & gas operators, and municipal agencies are entering a phase where robotics and remote visual inspection (RVI) technologies shift from pilot to scale. Our intelligence translates market momentum into timing recommendations for equipment acquisition vs. service contracting.

Video Inspection Robot Market

Technology risk management: Video inspection robots are no longer single-function cameras on wheels. Integrations with AI-assisted defect recognition, 3D laser profiling, and explosion-proof certifications change total cost of ownership, warranty exposure, and operator skill requirements.

Video Inspection Robot Market

Supply chain and regulatory exposure: Geopolitical shifts and component supply disruptions are compressing lead times and elevating input costs. Executives need a playbook that links procurement strategy to compliance and localization decisions.

M&A and partnership timing: The market’s growth profile and fragmentation create windows for bolt-on acquisitions, strategic alliances with sensor specialists, and channel consolidation—each requiring finely timed execution.

Transparent market sizing and forecasting methodology with scenario sensitivity across macroeconomic and regulation-driven outcomes.

Go-to-market playbooks for OEMs, system integrators, and service providers, including pricing levers, rental vs. purchase economics, and recurring service revenue models.

Procurement and deployment checklists for infrastructure owners—covering safety certifications, interoperability requirements, data portability, and training curricula.

Vendor decision matrices and vendor risk profiles that synthesize tech differentiators, service capability, and aftermarket strength (note: granular segment-level tables and proprietary vendor scoring are reserved for the full report).

Supply chain stress tests and mitigation playbooks focused on high-precision sensors and optical components—detailing inventory hedging, dual-sourcing, and nearshoring options.

Technology roadmaps and an investment prioritization framework that connects feature adoption (AI, 3D profiling, wireless telemetry) to real-world ROI across key use cases.

Regulatory impact scenarios and compliance pathways that anticipate inspection requirements, certification needs, and tariff contingency planning.

Accelerating intelligence at the edge: AI-assisted defect recognition has moved from lab demos to field deployments, enabling rapid triage and reducing human review costs. Vendors reporting commercialized AI pipelines are already influencing procurement specs.

Enhanced sensing and 3D analytics: Laser profiling and panoramic video are shifting inspection outcomes from qualitative observation to quantitative asset condition measurement—making predictive maintenance viable for many asset classes.

Operational safety and certification: Explosion-proof variants and certifications (e.g., ATEX/IECEx) are opening industrial and offshore markets that previously relied on more manual inspection methods; certified product deployments are now entering commercial operations.

Supply chain and regulatory headwinds: Since 2025, investigations and tariff measures targeting robotics-related imports, together with ongoing shortages in high-precision sensors and optical components, are increasing production lead times and unit costs—creating a near-term premium for proven inventory and supplier resilience strategies.

Fragmented competition with pockets of specialization: The market is characterized by many regional and niche specialists; top-tier OEMs excel at integrated systems and service contracts, while smaller players focus on compact, entry-level, or highly specialized vehicles for confined-space and underwater environments.

Envirosight LLC (Randolph, NJ, USA): Concentrating on sewer and pipeline robotics with high-definition video platforms and moving into AI-assisted defect recognition. Their focus is on integrated analytics that lower municipal operating costs.

Deep Trekker Inc. (Kitchener, ON, Canada): Known for robust pipe crawler and underwater ROV solutions—their value proposition centers on durability and ease of deployment for confined-space inspections.

Wuhan Easy-Sight Technology Co., Ltd. (Wuhan, China): Offers long-range pipeline CCTV solutions; they compete on cost-competitive HD inspection systems and increasingly on extended detection capabilities.

IBAK Helmut Hunger GmbH & Co. KG (Kiel, Germany): Emphasizing modular robots with panoramic video and laser profiling, targeting operators who require high-fidelity documentation and engineering-grade outputs.

CUES Inc. (Orlando, FL, USA): Tracks toward integrated truck-mounted and crawler systems for municipal markets, leveraging service models and fleet-level maintenance economics.

RedZone Robotics (Pittsburgh, PA, USA): Positions on autonomy for large-diameter pipe inspections—reducing operator burden and accelerating large-network coverage.

Mini-Cam Ltd. (United Kingdom): Focused on compact systems for drains and small-diameter pipelines where maneuverability and quick deployment drive purchasing decisions.

iPEK International GmbH (Germany): Delivers highly engineered robotic CCTV systems for precision inspection use cases and forensic-level documentation.

Waygate Technologies (Baker Hughes) (USA/Germany): Leveraging industrial heritage to introduce explosion-proof and certified inspection robots suited to heavy industry and offshore installations.

Inspector Systems (Germany): Specializes in modular video and laser inspection platforms adaptable across a wide range of pipe diameters and service requirements.

Notable recent market moves that influence near-term strategy: Envirosight’s 2025 launch of an AI-assisted ROVVER X HD platform, IBAK’s introduction of panoramic 3D laser profiling late in 2025, Baker Hughes’ early-2026 deployment of an explosion-proof robot in offshore facilities, and multiple entrants moving wireless CCTV crawlers into the market. These events underscore three tactical realities: differentiation is migrating from hardware specs to integrated analytics, certifications unlock new industrial demand pools, and speed-to-market for technological upgrades is a competitive lever.

Revisit procurement specifications: Insert requirements for modularity, software APIs, and field-upgradeability so hardware investments are protected as analytics evolve.

Prioritize certification in bid evaluations: For industrial and offshore exposure, require ATEX/IECEx or equivalent certifications as de facto procurement pre-conditions.

Diversify critical component sourcing: Implement dual-sourcing for optical sensors and key electronics; consider nearshoring partners to reduce tariff and logistics risk.

Accelerate pilot-to-scale pathways: Run short, measurable pilots tied to KPIs (defect detection rate, time-to-inspect, and cost-per-meter) to validate vendor claims before fleet rollouts.

Embed analytics and data governance: Treat inspection video and sensor data as an asset—invest in data pipelines, labeling workflows, and model lifecycle management.

Model service-first economics: For asset owners, compare total cost of ownership against managed inspection services, paying attention to frequency of inspection and data-processing costs.

Pursue targeted alliances and acquisitions: OEMs and system integrators should consider acquiring sensor specialists or software analytics teams to accelerate capabilities rather than building in isolation.

Plan for tariff and regulation scenarios: Develop rapid-response procurement playbooks that can be activated if tariffs or import restrictions materialize further.

Due diligence and vendor selection: We provide tailored RFP architecture, side-by-side TCO models, and on-site capability validation protocols.

Integration and deployment playbooks: From pilot design to large-scale fleet rollout, we create stepwise implementation plans that lock in performance targets and ROI triggers.

Supply chain resilience planning: Our experts run component risk assessments, supplier diversification roadmaps, and inventory optimization scenarios aligned to your tolerance for lead-time and cost volatility.

M&A and partnership advisory: We help identify strategic targets, build valuation models for capability-led acquisitions, and structure commercial partnerships to accelerate product roadmaps.

Regulatory and compliance roadmaps: We audit certification exposure, prepare compliance dossiers, and build contingency plans for tariff and trade-policy shifts.

PW Consulting’s Video Inspection Robot Market study is designed as a strategic instrument: it exposes the macro trajectory, distills vendor and technology shifts, and supplies the operational playbooks required to convert opportunity into measurable value. While this briefing highlights the most consequential themes for 2026 decision-making, the full report contains the granular scenario models, vendor scoring matrices, and segment-level forecasts that senior executives and investment teams require to move from strategy to execution. For organizations committed to shaping their position in this expanding market, the time to act—and to align procurement, technology, and M&A strategies—is now.

For detailed analysis of this topic, please visit the official page:Video Inspection Robot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com