North America Optical Encryption Market Outlook Driven by Cybersecurity and Fiber Network Expansion

Technology |

2026-07-10 15:08:15

PW Consulting’s latest market study on the worldwide non-invasive bilirubin meter market offers a forward-looking resource designed to inform strategic decisions in 2026. The global market reached approximately USD 234.6 Million in our base year (2025) and is forecast to expand at a compound annual growth rate (CAGR) of roughly 5.78% through the 2026–2032 forecasting window, reaching an estimated USD 347.5 Million by 2032. This release is a decision-grade briefing: it surfaces the commercial, regulatory and technology forces that will determine winners and losers, while preserving the detailed segment-level model and proprietary scenarios for full-report subscribers.

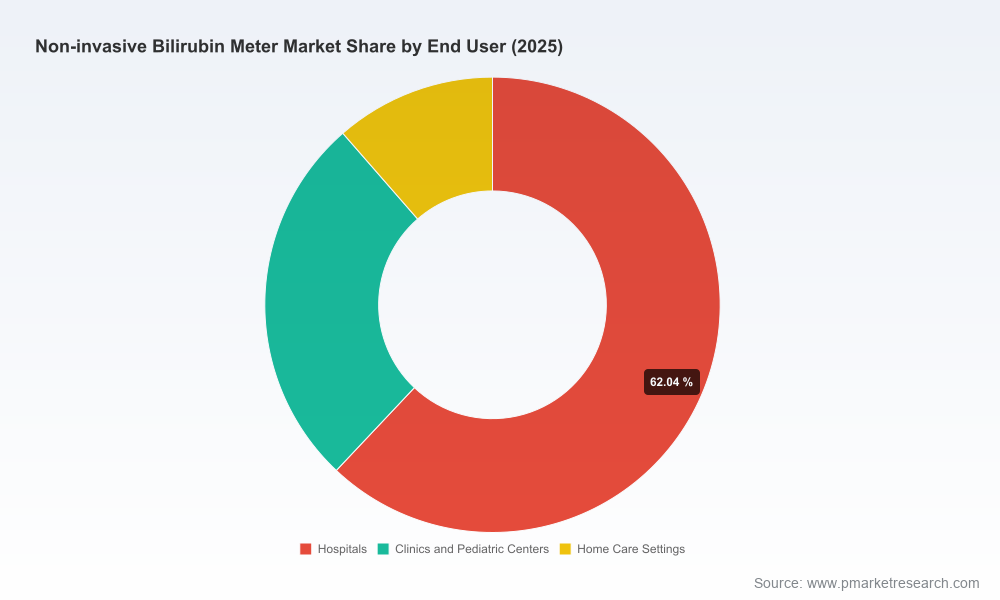

Worldwide Non-invasive Bilirubin Meter Market

Clinical economics are shifting: non-invasive bilirubin meters remove friction from neonatal jaundice screening and reduce the frequency of invasive blood draws, changing clinical workflows and long-term cost profiles in both inpatient and outpatient settings.

Worldwide Non-invasive Bilirubin Meter Market

Regulatory differentiation is real and actionable: devices with clear regulatory advantage are shortening sales cycles into high-acuity markets and commanding premium positioning with hospital procurement teams.

Worldwide Non-invasive Bilirubin Meter Market

Digital convergence is accelerating new business models: partnerships that combine optical meters with smartphone-based analytics or telehealth platforms are raising the strategic bar for incumbents and entrants alike.

Measured, steady growth but rising expectations. The market’s mid-single-digit CAGR signals predictable expansion rather than explosive disruption. That predictability favors disciplined commercial plays — targeted geographic expansion, selective clinical studies, and reimbursement engagement — over frothy scale-at-all-cost approaches.

Clinical guidelines and reimbursement studies are reinforcing adoption. Non-invasive transcutaneous bilirubin measurement is increasingly recognized by clinical authorities as an objective screening tool that complements serum testing, and evidence indicates downstream reductions in hospital readmissions for phototherapy when screening pathways are optimized. For purchasers, this translates into an easier value case when negotiating capital budgets with payers and hospital finance teams.

Regulatory clearance creates distribution leverage. Devices that secure robust regulatory clearances for use in younger neonates or broader clinical indications obtain preferential access to tertiary referral centers and large neonatal networks. Regulatory positioning is therefore both a market-entry barrier and a strategic asset for partnerships with distributors and system integrators.

Product form-factor and clinical workflow alignment matter. Portability, speed of measurement, ease of sterilization, and integration into electronic medical records are decisive procurement criteria. Buyers reward solutions that lower operational friction and total cost of ownership, including devices that minimize consumables and staff time.

Consolidation pressure in supplier markets. The vendor landscape is dominated by a relatively small group of global and regional suppliers. This concentration creates acquisition opportunities for strategic entrants seeking rapid scale in target geographies and also raises the stakes on manufacturing reliability and supply-chain redundancy.

Our review of incumbent and emerging suppliers shows three repeatable strategic moves that separate the leaders from followers: regulatory first-mover advantage, integration partnerships that extend clinical value, and disciplined product-platform roadmaps.

Regulatory leadership: Vendors that have secured high-quality regulatory clearances for neonatal use are winning procurement dialogues in major hospital systems. This regulatory moat shortens the sales cycle and de-risks adoption in conservative clinical environments.

Strategic partnerships and digital adjacencies: Collaborations that layer optical screening with analytics or smartphone-enabled triage have moved from pilots to scaled rollouts. These alliances create stickiness with end users and open new commercial channels (e.g., home-care monitoring, telemedicine-enabled follow-up).

Global footprint plus localized go-to-market: Manufacturers with a blend of global brand recognition and locally adapted distribution strategies are able to capture institutional contracts while also addressing community and home-care segments with appropriate pricing and service models.

Representative company signals in the current landscape:

Technology incumbents with a long product lineage continue to leverage clinical trust and distribution networks to defend core accounts.

Regional manufacturers are competing on cost and channel partnerships to expand reach into community clinics and home-care channels.

New cross-sector alliances — for example between optical meter manufacturers and smartphone analytics firms — are emerging as a strategic focal point. Recent collaboration activity in 2024 highlights how combining sensor hardware with software-enabled triage can accelerate adoption in both hospitals and community settings.

Device clearance and indicated patient populations are procurement differentiators. Regulatory approvals that explicitly permit screening in younger gestational ages unlock access to neonatal units with stricter clinical protocols.

Clinical guidance alignment is non-negotiable. Devices that map clearly to established guidelines and peer-reviewed evidence are easier to integrate into newborn-care pathways and quality improvement initiatives.

Payer economics favor screening pathways that demonstrably reduce invasive testing, shorten LOS, or lower readmission rates; early engagement with payers and health economics evidence generation will accelerate institutional uptake.

For device manufacturers — prioritize regulatory and evidence milestones. Secure targeted clearances, invest in comparative clinical studies that quantify reductions in invasive testing and readmissions, and publish health-economic models that procurement teams can operationalize.

For commercial leaders — build a two-track GTM: pursue institutional hospital contracts with clear ROI narratives while piloting lower-cost configurations and service bundles for clinics and home care. Leverage digital partnerships to create bundled offerings that increase recurring revenue.

For investors and M&A teams — look for targets that combine a defensible regulatory position with scalable distribution and product modularity. Opportunities exist to consolidate regional vendors with complementary channel strengths and to roll up software-enabled services that increase lifetime customer value.

For health systems — accelerate procurement cycles by foregrounding total cost of care benefits (reduced blood draws, fewer readmissions, streamlined staff workflows) and insist on interoperability with EMR systems to maximize operational gains.

The full report is structured to move beyond high-level forecasts into operationally useful intelligence for 2026 strategy. Subscribers receive:

Robust market sizing and scenario-driven forecasts across a 2026–2032 horizon, including sensitivity analysis for regulatory and reimbursement inflection points.

Competitive benchmarking that profiles product portfolios, regulatory status, route-to-market, and supply-chain characteristics for leading vendors.

Clinical and payer impact assessments with modeled ROI templates that procurement teams can adapt for business-case submissions.

Go-to-market playbooks tailored to different entry strategies: direct sales into tertiary centers, distributor-led expansion, and digital partnership models for community and home-care uptake.

M&A and partnership screens which identify priority acquisition targets and integration risks, plus valuation sensitivity tied to commercialization milestones.

Regulatory roadmap guidance and evidence generation plans designed to minimize time-to-adoption across target markets.

Set 12–18 month milestone goals focused on regulatory or clinical evidence rather than only geographic coverage. Achieving a single, strategically chosen clearance or a pivotal clinical partnership can deliver outsized returns on commercial investment.

Make interoperability and data services a line-item in product development and commercial negotiations; buyers are increasingly valuing connected workflows over standalone hardware.

Run acquisition screens against both market share expansion and capabilities acquisition (e.g., software analytics or distribution networks), and stress-test valuations against regulatory delay scenarios.

For health systems and payers, use the supplied ROI templates to pilot risk-sharing procurement arrangements that align incentives around reduced re-admissions and minimized invasive testing.

This briefing is a strategic primer — it surfaces the macro growth trajectory, the regulatory and clinical contours, and pragmatic plays for 2026. PW Consulting’s full report contains the detailed segment models, vendor-level scorecards, and downloadable buyer templates necessary to convert insight into executable plans. For teams preparing budgets, investor diligence, or market-entry strategies in 2026, the report delivers the empirical foundation and operational templates to accelerate confident decision-making.

Contact PW Consulting to access the comprehensive dataset and the practitioner’s annex that includes playbooks, model files and scenario workbooks tailored for corporate strategy, sales operations, and M&A diligence.

For detailed analysis of this topic, please visit the official page:Worldwide Non-invasive Bilirubin Meter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com