Worldwide Pipe Flanges Market — Strategic Briefing for 2026 Decision‑Makers

Executive summary

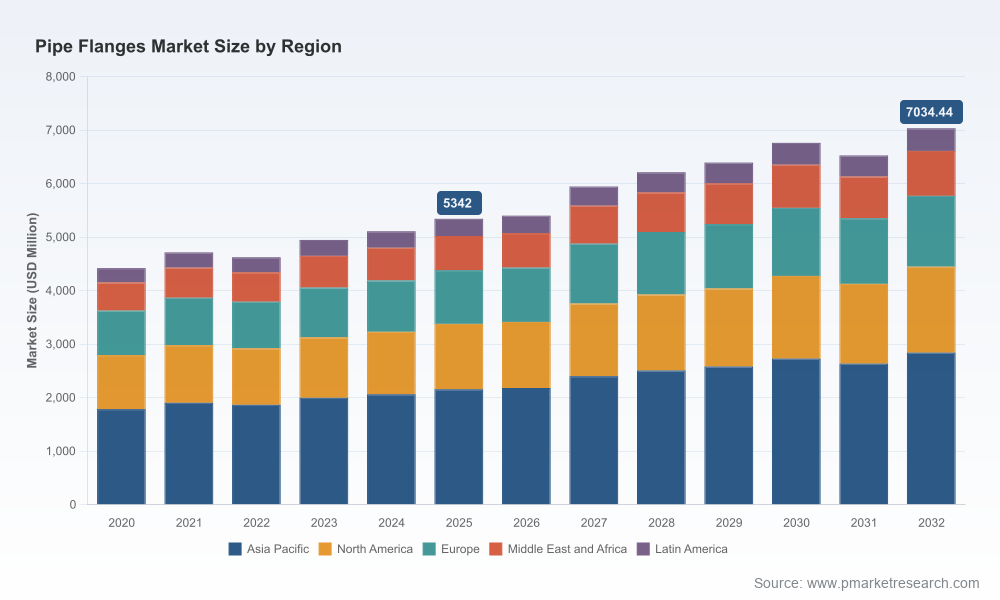

As global industrial systems continue to evolve, the pipe flanges market is entering a phase where regulatory rigor, material cost dynamics, and targeted engineering specialization will determine winners and laggards. Our latest PW Consulting report — the Worldwide Pipe Flanges Market (base year 2025, forecast 2026–2032) — shows a market that reached roughly USD 5.34 billion in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of approximately 4.01% across the 2026–2032 horizon, reaching just over USD 7.03 billion by 2032. These headline metrics hide a far more nuanced landscape: a fragmented supplier base, differentiated technology and process capabilities, and accelerating compliance requirements driven by the 2025 ASME updates and near‑term raw material volatility.

Worldwide Pipe Flanges Market

Why this matters for corporate strategy in 2026

For executives and investors planning capital allocation, procurement strategies, or M&A activity in 2026, three strategic truths derived from our analysis are immediate and actionable:

Worldwide Pipe Flanges Market

- Market expansion will be steady but uneven — sufficient to justify targeted investment but not broadscale capacity builds. The mid‑single-digit CAGR implies demand growth, while pockets of higher tolerance for premium, certified products will reward focused capability.

- Regulatory and standards evolution (notably ASME B16.5-2025) will raise the bar for certification, testing, and material traceability — creating both compliance cost pressure and differentiation opportunities for suppliers that can demonstrate superior process controls.

- Raw material trends remain a lever of competitive advantage. Early‑2026 stabilization of global steel prices, coupled with spikes in stainless steel cost indicators, changes margin dynamics across material classes and encourages both hedging and product substitution strategies.

What the PW Consulting report delivers (practical contents)

Designed as an executive toolset, the report combines forward-looking market modeling with practical playbooks that procurement, engineering, and corporate development teams can use immediately. Highlights include:

Worldwide Pipe Flanges Market

- Top‑line market sizing and validated forecast model (2026–2032) with scenario options driven by raw material and regulatory sensitivity levers.

- Segment frameworks by region, material, flange type, and end‑use — with demand drivers, margin archetypes, and supplier coverage maps (note: this briefing intentionally omits detailed segment tables; the full report contains granular splits and downloadable datasets).

- Supply chain risk maps and recommended mitigation actions, including inventory buffers, alternate sourcing routes, and long‑lead procurement playbooks.

- Regulatory compliance matrix centered on ASME B16.5-2025 implications: material choices, pressure‑temperature re‑ratings, testing protocols, and marking/traceability requirements.

- Commercial playbooks — pricing strategies, aftermarket pathways, and specification‑level positioning for premium versus commodity segments.

- Actionable M&A target shortlist criteria and vendor scorecards for due diligence, from technical capacity through quality systems and export capability.

Market dynamics: raw materials, standards, and cost pressure

Two external forces dominate the near term: raw material price behavior and standards evolution.

- Raw materials: After the turbulence of 2024–2025, U.S. steel markets showed signs of stabilization in early 2026, with benchmark mill prices settling in the low‑to‑mid $800s per short ton. At the same time, stainless steel cost indicators — exemplified by the U.S. Producer Price Index for Steel Pipe and Tube, Stainless Steel reaching 149.563 in March 2026 (base 1982=100) — underscore continuing cost differentials and volatility for corrosion‑resistant alloys. Corporates that adopt dynamic procurement, strategic hedging, or modular substitution strategies (e.g., lining systems, hybrids) will protect margins and win tenders.

- Standards and compliance: The release of ASME B16.5-2025 is a watershed for flange manufacturers and specifiers. The revision updates pressure‑temperature ratings, expands allowable materials, and clarifies normative language (revising the definitions of "may", "shall", and "should"), while adding explicit minimum temperature appendices and revised variables for testing and marking. The net effect: increased technical documentation, more rigorous testing, and potential rework for legacy product lines. Forward‑looking product roadmaps should embed these requirements to avoid specification obsolescence and to capture premium pricing for “ASME‑aligned” components.

Competitive landscape — fragmentation, specialization, and regional champions

The pipe flanges market remains fragmented: the top three firms account for only a low‑teens share of global revenue (CR3 ≈ 16.4%), while the five largest reach under a quarter of market sales (CR5 ≈ 22.85%). This structure creates an environment where regional champions, specialized engineering houses, and integrated steel players coexist.

Key strategic archetypes and representative firms include:

- Fast‑turnaround specialists focused on ANSI/API standards and custom solutions — exemplified by Texas Flange and Federal Flange (both Houston‑based) — which compete on responsiveness, large‑diameter capability, and inventory depth for petrochemical and oil & gas projects.

- Engineering‑led manufacturers with multi‑standard portfolios (AWWA, ASME, DIN) and expansion joint expertise, such as API International, which appeal to municipal waterworks and process markets requiring standardized interchangeability and engineered joints.

- Forging and high‑performance flange producers (e.g., Maass Flange Corporation, Metalfar S.p.A., Flanschenwerk Bebitz) competing on metallurgy, fatigue life, and precision tolerances for power generation and demanding industrial applications.

- Global integrated suppliers and distributors — Allied International Group, Vallourec, Nippon Steel — who combine upstream metallurgical capability with global distribution and aftermarket networks, thereby reducing supply chain friction for multinational EPCs.

- Large Chinese manufacturers (e.g., Longan Flange, Hebei Shengtian Pipe‑Fitting Group) that combine scale with competitive pricing, increasingly investing in quality certifications and export capabilities to move up the value curve.

- Precision and specialty suppliers such as Swagelok and Core Pipe Products, which target high‑purity, high‑precision markets (lab, semiconductor, specialty chemicals) with premium pricing and strict quality systems.

Strategic implications: scale alone no longer guarantees wins — technical certifications, test capacity (pressure/temperature), material traceability, and the ability to meet ASME‑2025 requirements are decisive. Firms that can pair regional service with documented quality systems and rapid compliance adaptation command price premiums.

Recent events shaping 2026 strategy

- ASME B16.5-2025 (May 2025): Suppliers and buyers must update procurement specifications and testing protocols to align with revised pressure‑temperature ratings and material lists. We expect a near‑term wave of specification audits by EPCs and owner‑operators.

- Industry trade engagement (TUBE Düsseldorf, April 2026): Major players including Allied International Group and Arrow Pipes leveraged TUBE 2026 to showcase new fitting technologies and supply chain partnerships — indicative of a renewed emphasis on platform partnerships and product ecosystem plays.

- Material price signals (early 2026): Stabilization of steel prices and continued movement in stainless steel indices will influence margin trajectories in 2026. Firms with disciplined procurement and contract indexation will be advantaged.

Strategic recommendations — three priorities for 2026

Based on scenario modeling and company‑level assessments, PW Consulting advises the following priorities for executives operating in or adjacent to the pipe flanges market:

- Embed ASME‑2025 compliance into product lifecycles now. Update specifications, test regimens, and documentation workflows to preclude downstream rework costs. Consider third‑party verification and visible certification as a price differentiation tool.

- Adopt a differentiated procurement strategy. For commodity carbon steel work, pursue long‑term frame agreements with regional producers to secure volume and price. For alloy and stainless applications, implement multi‑tier sourcing and hedging mechanisms tied to steel price indices to protect margins.

- Pursue bolt‑on M&A or JV targets that add testing capacity, high‑grade forging, or strategic geographic footprints. Given low market concentration, selective acquisitions of certified, high‑margin specialists or distributors can yield faster customer access than greenfield expansion.

How to use the full report

The summary above highlights the strategic lens we apply to the pipe flanges market. The full PW Consulting report includes:

- Downloadable datasets and interactive forecasting models (base 2025, forecast 2026–2032) with scenario toggles for steel price, ASME adoption pace, and regional demand rotation.

- Detailed segment-level demand and revenue breakdowns by region, material, flange type, and end‑use — complete with buyer specification matrices and tender timelines.

- Company scorecards and acquisition candidate shortlists with qualitative risk flags and quantified synergies estimates.

To preserve the usefulness of this briefing as a strategic primer, we have deliberately withheld the granular segment tables and downloadable spreadsheets that underpin our modeling. These are available on the report landing page for teams that require the numerical foundations for procurement negotiations, capex planning, or M&A diligence.

Closing—where PW Consulting adds value

PW Consulting’s approach is pragmatic: we translate market forecasts into executable options. For stakeholders evaluating capital deployment, procurement contracts, or strategic partnerships in 2026, the critical questions are not whether the global market will grow — it will — but where to place bets that convert modest demand growth into outsized margins. The interplay of tightened ASME requirements, material cost dynamics, and continued supplier fragmentation creates both risk and opportunity. Firms that move early to certify, secure flexible supply, and align product portfolios with the new compliance baseline will not only protect revenue — they will capture the premium end of the market.

Next steps

Access the full Worldwide Pipe Flanges Market report to obtain the granular segment tables, downloadable model, and our prioritized M&A target list. For bespoke advisory — including supply‑chain stress tests, procurement renegotiation playbooks, or carve‑out valuation — PW Consulting’s industry team is available for executive workshops and tailored diligence engagements.

For detailed analysis of this topic, please visit the official page:Worldwide Pipe Flanges Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com