The Rise of Twin Screw Pump Market Industry Trends and Innovations

Other |

2026-06-25 09:33:30

PW Consulting's latest market study on the Worldwide Aluminium Sulfate Market (base year 2025, forecast period 2026–2032) equips executives with a decision-grade view of industry dynamics they must navigate in 2026. The market reached approximately USD 1,422.5 Million in 2025 and exhibits a steady compound annual growth rate (CAGR) of 3.8% over the forecast horizon. Under the central-case projection the market grows to roughly USD 1,846.9 Million by 2032, while historical performance between 2020 and 2025 shows cyclical movement driven by raw-material swings and end-market demand variability (notable datapoints: ~USD 1,180.5M in 2020, ~USD 1,321.9M in 2022, ~USD 1,277.7M in 2023, and ~USD 1,360.4M in 2024).

Worldwide Aluminium Sulfate Market

Actionable foresight for procurement and sourcing: identify when and how to hedge alumina hydrate and sulfuric acid exposure to protect margins.

Worldwide Aluminium Sulfate Market

Capex prioritization and brownfield/greenfield siting choices informed by regional demand resilience and trade-policy risk.

Worldwide Aluminium Sulfate Market

M&A and partnership playbook calibrated to a market with moderate concentration (CR3 ~32.4%; CR5 ~46.8%), where well-timed consolidations and strategic bolt-ons can materially improve scale and route-to-market.

Commercial and product strategies tailored for municipal water operators, pulp & paper buyers, and industrial specialty users where value capture increasingly depends on service, technical support, and formulation sophistication.

Forecast models (2026–2032) with scenario layers (base, downside, upside) and sensitivity to raw-material price paths and trade barriers.

Supply-chain heat maps and supplier scorecards: production footprints, logistics cost buckets, lead-time analytics, and quality differentials.

Commercial playbooks: contract templates, pricing tactics for municipal tenders, and account-mix optimisation for industrial channels.

Cost-to-serve and margin decompositions by product grade (technical, industrial, specialty) with breakpoint analyses to support SKU rationalisation.

Regulatory and trade-risk checklists including duty scenarios, labelling/compliance matrices and recommendations for customs classification and dispute readiness.

M&A screening tools: quantitative filters and qualitative assessment templates to shortlist targets and evaluate synergies (procurement, channel, technology).

Operational playbooks: maintenance, yield improvement, and environmental control levers that reduce variable cost per ton and improve product consistency.

The aluminium sulfate industry is being pulled by both demand-side and supply-side forces. On the supply side, feedstock volatility is a primary margin lever. Alumina hydrate, a principal feedstock, averaged roughly USD 385/metric ton in 2023 amid supply-chain pressures, while sulfuric acid saw notable price appreciation (roughly USD 150–180/metric ton FOB China in Q4 2023) linked to fertilizer sector demand. These inputs create a cost floor that distorts short-term pricing and can render spot-market purchases uneconomical without effective hedging.

On the demand side, municipal water treatment remains a durable backbone, supported by regulatory upgrades and urbanization in emerging markets. Industrial segments such as paper & pulp and textiles show differentiated growth profiles tied to regional industrial cycles and substitution dynamics. Geopolitical and trade-policy developments also matter: longstanding anti-dumping measures (e.g., duties on certain imports from China in markets such as the United States) materially alter competitive economics and create both risk and opportunity for non-Chinese producers and importers.

Regulatory settings have a pronounced influence on product acceptability and adoption. Notably, aluminium sulfate used in water treatment is classified as non-hazardous under the EU CLP framework for its intended applications — a factor that simplifies logistics and reduces compliance costs in European public tenders versus more complex classifications.

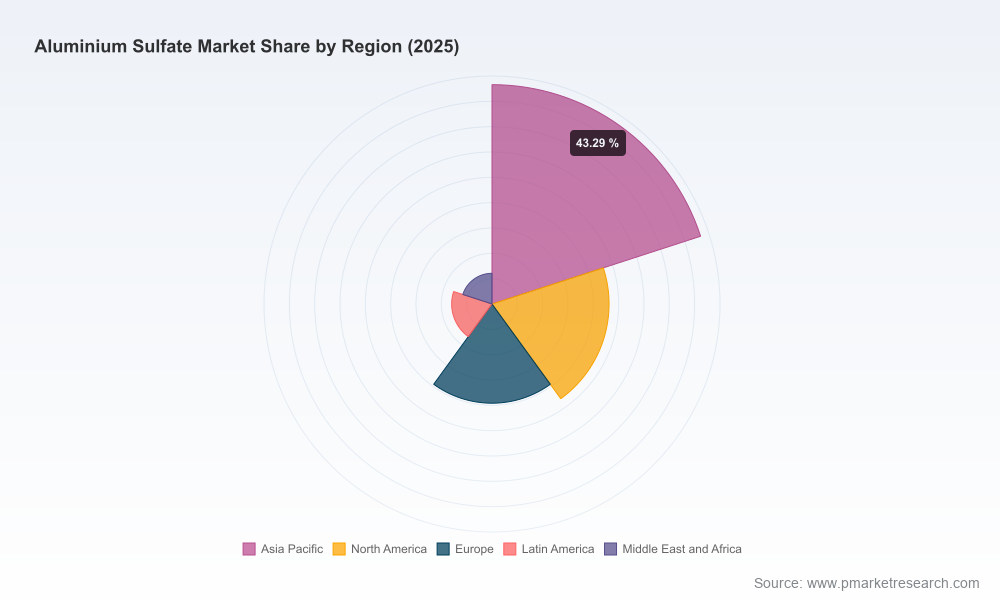

The market displays moderate concentration: the top three players account for roughly one-third of demand while the top five approach just under half of the market. This structure creates a competitive middle where specialist producers, regional champions, and global suppliers each have distinct strategic pathways.

Large integrated suppliers (examples include established North American and European chemical firms) emphasize reliability, technical services, and multi-site redundancy to capture institutional municipal contracts and long-term industrial relationships.

Regional and export-oriented manufacturers focus on cost-competitiveness and logistic optimization to serve nearby demand centers — particularly where trade barriers or freight economics favor local supply.

Specialty and technical-grade producers concentrate on higher-margin niches such as laboratory reagents, leather tanning, and textile processing where formulation and quality control command a premium.

Selected profiles exemplify these strategic archetypes: firms with deep municipal water-treatment expertise leverage product breadth (liquid and dry grades) and field-service capabilities to defend tenders; chemical distributors and logistics-focused groups exploit blended manufacturing/warehousing footprints to shorten lead times; and several large producers in Asia and Europe maintain export-oriented capacity but operate within a trade environment that includes antidumping duties and tariff asymmetries.

Procurement and raw-material risk management — establish multi-year supply contracts for alumina hydrate and sulfuric acid with indexed pricing collars, and create optionality via regional suppliers to guard against freight and duty shocks.

Near-shoring and inventory strategy — for companies with significant exposure to regulated municipal demand, evaluate near-shore blending terminals or satellite packaging to reduce lead-time risk and improve responsiveness to tenders.

Product and commercial differentiation — invest in technical service teams and co-created dosing trials with key water authorities to transition commodity relationships into long-term value contracts.

M&A and portfolio moves — prioritize bolt-on acquisitions that add distribution reach, specialty grades, or feedstock integration. With CR3/CR5 at moderate levels, well-executed consolidation can yield rapid accretion.

Trade and compliance playbook — maintain active monitoring of antidumping cases and tariff schedules. In jurisdictions with active duties, consider strategic alliances with compliant regional producers or pursue legal avenues for exclusions where appropriate.

Scenario planning — maintain three operational scenarios for 2026 planning: (1) soft demand with stable feedstock costs, (2) demand rebound paired with sulfuric-acid price inflation, and (3) trade-policy tightening that raises landed costs from specific geographies. Each scenario should map to clear contingency actions on pricing, inventory and capex.

This bulletin is a targeted preview intended to arm decision makers with the high-level context and immediate strategic implications for 2026. The full report contains the proprietary, granular datasets and tools you need to act — including region- and application-level demand curves, supplier capacity matrices, plant-level cost curves, and downloadable commercial templates. We intentionally limit the publication of detailed segment figures in this press release to preserve the actionable value that our institutional clients rely on; those details are available in the full report and interactive dashboards.

For procurement and operations teams: request the raw-material sensitivity module to run custom hedging and inventory scenarios tailored to your contract portfolio.

For corporate development: use our M&A screening pack to identify targets that match your strategic criteria and perform rapid valuation stress-tests under the three stated scenarios.

For regulatory and trade teams: obtain the country-level duty tracker and compliance checklist to assess exposure and mitigation options before issuing 2026 bids.

PW Consulting combines chemical-industry technical depth with transaction-grade commercial analysis. If you are formulating budgets, negotiating major supply agreements, or evaluating strategic M&A in 2026, our Worldwide Aluminium Sulfate Market report provides the rigorous, decision-ready intelligence you need. For an executive briefing and access to the full dataset and tools, please follow the link to the full report or contact our advisory team for a tailored session.

For detailed analysis of this topic, please visit the official page:Worldwide Aluminium Sulfate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com