Worldwide Dairy-Free Infant Formulas Market: Strategic Intelligence to Guide 2026 Decisions

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I am pleased to present the executive overview of our new market research report on the Worldwide Dairy-Free Infant Formulas market. This sector has moved rapidly from niche to strategic priority for infant nutrition manufacturers, ingredient suppliers, private-label players and retailers. For executive teams setting 2026 budgets, pipeline priorities, regulatory engagement plans and M&A screening criteria, this report is designed to be the operational playbook that turns macro momentum into executable decisions.

Worldwide Dairy-Free Infant Formulas Market

Key market metrics that matter for 2026 planning

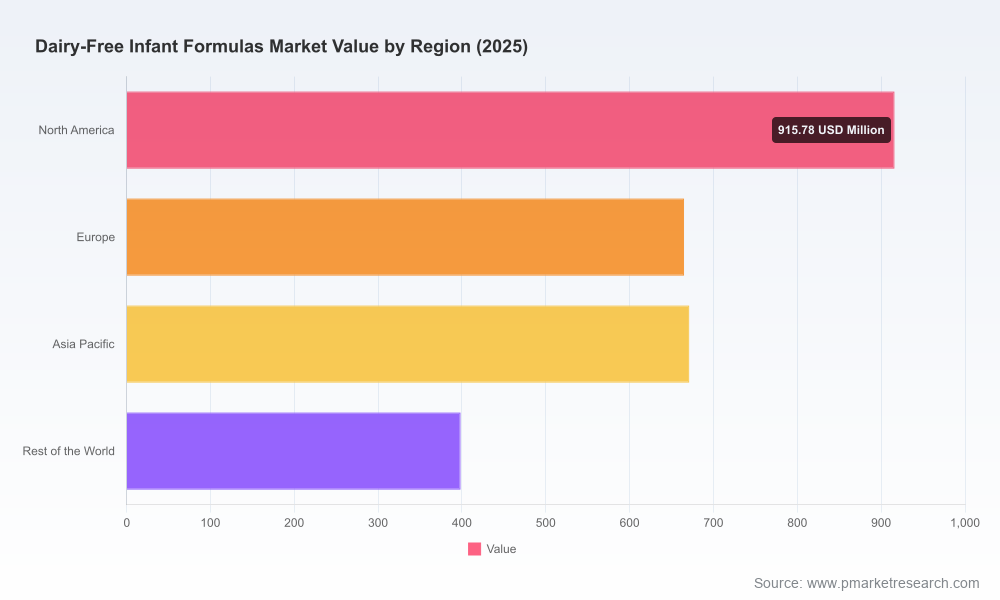

Our base-year assessment (2025) places the market at approximately USD 2.65 billion. After a steady recovery and expansion from the early 2020s, we forecast the sector to grow at a compound annual growth rate (CAGR) of 6.85% through the 2026–2032 period, reaching roughly USD 4.21 billion by 2032 under our base-case assumptions. These headline metrics encapsulate durable demand drivers — rising consumer interest in plant-based nutrition, well-documented allergy and intolerance use cases, and innovation in protein technologies — while also reflecting ongoing regulatory and supply-chain volatility that will shape winners and laggards in the coming 18–36 months.

Worldwide Dairy-Free Infant Formulas Market

Market concentration is material: the top three incumbent groups capture a majority share, and the top five exert a strong influence on pricing, raw-material sourcing and distribution agreements. This concentration creates tactical advantages for established brands but also opens rapid-entry windows for well-capitalized challengers and specialty innovators who combine novel formulations with rigorous regulatory validation.

Worldwide Dairy-Free Infant Formulas Market

What the PW Consulting report delivers — deeply practical, immediately usable

- Proven market-sizing methodology and sensitivity analyses that translate macro forecasts into quarterly revenue run-rates and SKU-level acceptance curves — enabling marketing and finance teams to stress-test 2026 P&Ls.

- Segment-level framework (by geography, product type and distribution channel) that connects consumer demand signals to SKU assortment recommendations — note: full segment tables and proprietary splits are included in the report to preserve competitive value.

- Regulatory impact map and a tactic-by-tactic playbook for label claims, nutrient statements and protein-quality pathways (including how to operationalize the PER rat bioassay guidance for novel plant proteins).

- Supply-chain and raw-material scenario planning, with emphasis on soy supply dynamics, alternative plant proteins, ARA/DHA sourcing risk and private-label manufacturing options.

- Competitive benchmark dossiers on leading incumbents and challengers — product portfolios, recent investments, supply partnerships, route-to-market strategies and M&A capacity.

- Actionable go-to-market models for three commercial archetypes (Global Incumbent, Regional Challenger, and Specialty Brand) with 12–24 month implementation roadmaps.

- M&A and partnership heatmaps identifying the most attractive acquisition profiles, integration risks and expected accretion timelines.

- Customer and clinician perception insights derived from a bespoke survey of caregivers, pediatric dietitians and retail buyers — directly informing packaging, pricing and omnichannel offers.

Competitive landscape — incumbents, insurgents and strategic responses

The competitive field mixes multinational nutrition giants, established private-label manufacturers and fast-growing specialty brands. Legacy players continue to leverage scale across ingredient sourcing, global regulatory teams and extensive retail networks; their role in maintaining supply continuity and category trust is significant. At the same time, small and mid-sized innovators are capturing attention with clean-label, whole-food plant formulations and differentiated sourcing stories.

- Global nutrition leaders are optimizing portfolio mixes to cover clinically justified, dairy-free use cases while defending core milk-based businesses. Expect continued investment in R&D and clinical validation to maintain shelf and clinician recommendation share.

- Specialty entrants are fast-following regulatory pathways—particularly those tied to protein-quality validation—to commercialize non-soy, plant-based formulas. Regulatory advances around Protein Efficiency Ratio (PER) pathways are materially shortening time-to-market for some of these entrants.

- Retailers and private-label manufacturers see this category as both margin opportunity and traffic driver; their capability to scale private-label dairy-free SKUs can meaningfully change price dynamics in key markets.

Our company dossiers cover the full spectrum: multinational groups with legacy brands, challengers focused on almond/buckwheat/tapioca blends, organic specialists, and private-label manufacturers. For decision-makers weighing partnerships, supplier contracts or acquisition targets, the report offers comparative scorecards that synthesize regulatory readiness, manufacturing footprint and commercial traction.

Recent industry events that will determine 2026 outcomes

- Regulatory momentum: U.S. regulatory initiatives have accelerated. FDA guidance updates on labeling and allergen declarations approved in late 2024–2025 and the Operation Stork Speed initiative are redefining the pathway for plant-based infant formulas. Publicly available U.S. appropriations language further incentivizes expedited review pathways for non-soy, plant-based formulas. These developments change the calculus for clinical development spend, labeling strategy and market-entry sequencing.

- Safety and supplier risk: A major recall event tied to an ingredient supplier highlighted vulnerabilities in specialized lipid supplies and underscored the need for multi-sourcing, enhanced supplier audits and expanded in-house testing capabilities. Manufacturers and retailers must recalibrate vendor approval and continuity plans accordingly.

- Regulatory validation for novel proteins: The formalization of PER-related guidance has created a credible scientific route for some plant-protein innovators to substantiate protein quality claims in infant nutrition. This is a transformative enabler for brands using non-soy plant sources.

Strategic imperatives for 2026 — prioritized actions

- Regulatory-first product design: Treat regulatory engagement as a product development pillar. Invest in protein-quality studies early and align labeling language with current FDA guidance to avoid rework and recall risk. For challengers with novel proteins, secure pre-submission meetings and document a clear PER validation roadmap.

- Supply-chain resilience and ingredient diversification: Move from single-supplier dependencies to multi-sourcing for critical lipids and protein isolates. Build redundancy in ARA/DHA sourcing and consider near-shore manufacturing to reduce transport and recall exposure.

- Channel and pricing segmentation: Develop differentiated packaging and price points for pharmacy, mass and online channels. Use e-commerce to test new SKUs and rapid-iterate formulations with caregiver feedback before national rollouts.

- Clinical and clinician engagement: Fund small, high-quality clinical or feeding tolerance studies and pediatric dietitian outreach to build clinician trust. Clinical differentiation buys shelf-space and formulary inclusion in hospital systems where applicable.

- M&A and partnership opportunism: With market concentration significant at the top, there is room for strategic bolt-on acquisitions — particularly to acquire manufacturing capacity, clinical data, or alternative-protein IP. Private-label and co-manufacturing deals can accelerate scale economically.

- Quality assurance as market differentiator: Elevate quality-testing transparency (batch testing availability, third-party certifications) as a brand trust lever following recent category recalls.

M&A, investment and go-to-market playbook

For CFOs and corporate development teams, this is an inflection point. The expansion trajectory and concentration metrics create an environment where well-timed acquisitions can deliver rapid accretion—especially for buyers who can integrate manufacturing capacity and regulatory expertise. For investors considering specialty brands, focus on firms with documented supply paths, completed PER/protein-quality work or contractual retail access.

Commercial teams should prioritize four capability builds: (1) regulatory and clinical program management, (2) scalable manufacturing (co-manufacturing contracts with validated quality systems), (3) omnichannel retail execution, and (4) consumer trust through transparent ingredient narratives and third-party testing. Our report provides an implementation timeline and cost estimates to operationalize these capabilities within a 12–24 month horizon.

Risk framework and mitigation checklist

- Ingredient contamination and single-source failure — implement multi-sourcing and third-party screening; maintain strategic safety stock for critical lipids.

- Labeling and claims violations — standardize label review workflows and legal signoffs tied to FDA guidance.

- Regulatory delay — stage product launches with conditional channel prioritization: markets with clearer guidance first, others later.

- Price competition from private label — protect margin via formulation differentiation, branded clinical claims and retailer co-marketing.

How PW Consulting supports your 2026 agenda

This report is crafted to be both a strategic compass and an implementation guide. It avoids superficial market commentary and instead provides the tactical blueprints that commercial, regulatory and operations leaders need to execute in 2026. For teams preparing board decks, investment committees or go-to-market launches, our scenario models, supplier heatmaps and regulatory playbooks convert macro opportunity into measurable KPIs and project plans.

To preserve the competitive value of our analysis, we have intentionally withheld certain proprietary segment-level data from this press overview. The full report contains complete regional and channel splits, SKU-level demand curves, company scorecards and downloadable Excel models designed for immediate integration into planning systems. Access to the full dataset and an executive briefing can be arranged through PW Consulting’s report portal.

Contact PW Consulting to schedule a tailored 60-minute briefing where we will walk through the forecast sensitivities, the supplier risk matrix and a customized 12-month implementation roadmap aligned to your organization’s strategic profile.

For detailed analysis of this topic, please visit the official page:Worldwide Dairy-Free Infant Formulas Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com