Worldwide Paper Direct Dyes Market — Strategic Outlook for 2026

PW Consulting’s new Worldwide Paper Direct Dyes Market report (base year 2025, forecast 2026–2032) is designed as a decision-grade intelligence asset for executives preparing budgets, sourcing strategies, product roadmaps and M&A screens in 2026. The market has moved from roughly USD 442 million in 2020 to USD 545.6 million in 2025 and is projected to advance at a compound annual growth rate (CAGR) of about 4.5% through 2032, reaching an estimated USD 742.5 million. That steady expansion belies important inflection points — regulatory tightening, raw-material volatility and differentiated supplier strategies — that will determine winners and losers in the coming 18–36 months.

Worldwide Paper Direct Dyes Market

Market snapshot: what the top-line tells you

The direct-dyes segment for paper demonstrates resilient, mid-single-digit growth driven by packaging-grade paper demand, tissue/towel substitution cycles, and continued emphasis on on-machine coloration to improve cost-in-use versus post-production colorants. The market’s overall growth trajectory is stable enough to support incremental investment, but the underlying dynamics are heterogeneous — regions, process routes (wet-end vs. size-press), and end-use regulatory regimes matter. Market concentration is moderate: the top three suppliers account for under a third of revenue (CR3 ≈ 28.5%) and the top five approach just over 40% (CR5 ≈ 41.1%), indicating room for both niche specialists and larger chemical companies to expand through targeted moves.

Worldwide Paper Direct Dyes Market

What the report delivers — practical, transaction-ready content

- Proprietary market model (USD Million base year 2025) with historical series and bottom-up forecast scenarios through 2032, including sensitivity to pulp prices and regulatory shock events.

- Guided segmentation maps (by geography, product form and application) and commercial sizing — presented as actionable priorities rather than raw, granular tables for easy executive briefs.

- Supplier benchmark framework covering product breadth, regulatory dossiers, ESG credentials, price positioning and technical support capability.

- Regulatory-impact matrix identifying likely formulation constraints from recent EU and global developments, and a compliance roadmap for food-contact and ecolabel channels.

- Procurement playbook: price pass-through modeling, contract clauses for raw-material volatility, and dual-sourcing templates tailored to dye concentrates and powders.

- R&D prioritization and formulation-de-risking checklist (including PFAS alternatives, low-migration chemistries, and wastewater treatment compatibility).

- M&A and partnership screening tools — fit-for-purpose scorecards to identify bolt-on targets, toll-manufacturing partners, or regional distributors.

Why this matters for 2026 decisions — five strategic imperatives

- Secure supply under input-price uncertainty. Volatility in pulp and energy affects mill run-rates and dye demand elasticity. Procurement teams should use scenario models (included in the report) to stress-test supplier contracts for both powder and concentrated liquid platforms and lock in contingency capacity in low-cost geographies.

- Make regulatory compliance a market access play. The 2025 EU REACH revisions and tightened scrutiny of PFAS and endocrine disruptors mean certain dye chemistries face higher de-risking costs. For 2026, prioritise suppliers with up-to-date registrations, REACH dossiers, and documented conformance to standards such as FDA food-contact criteria and established ecolabels.

- Differentiate through sustainability credentials, not just price. Buyers and brand owners increasingly demand traceability, ZDHC/ MRSL conformance and low-impact wastewater profiles. Investment in validated lifecycle claims and factory-level treatment solutions yields commercial insulation and price premium opportunities in packaging and food-contact grades.

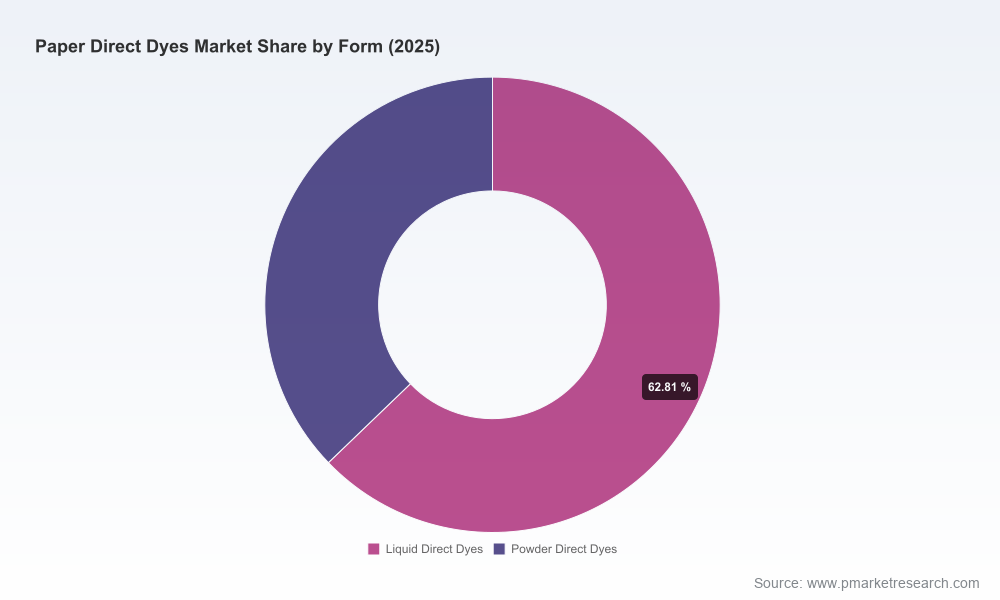

- Optimize product form mix across channels. Operational trade-offs between liquid concentrates (operational convenience, dilution control) and powder dyes (logistics efficiency) matter for capital planning. Our playbooks show when to prioritize on-site mixing capabilities, tolling agreements, or pre-diluted supply to accelerate time-to-market and reduce in-mill complexity.

- Pursue targeted consolidation and partnerships. The sector’s moderate concentration creates openings for regional champions, chemical majors and specialized formulators. The report’s M&A scorecards highlight subsegments and geographies where bolt-on acquisitions or technical partnerships unlock rapid scale with manageable integration risk.

Competitive dynamics — what to watch in 2026

The supplier landscape combines global chemical companies, dedicated colorant specialists, and regional producers. Leading players demonstrate distinct strategic archetypes:

Worldwide Paper Direct Dyes Market

- Solenis — a large paper-chemicals player that leverages an integrated portfolio (including Pergasol direct dyes) and public sustainability disclosures. Their recent price adjustments in certain regions and active trade-show engagement signal a market-facing approach that balances margin management with sustainability positioning.

- ChromaScape — focused on Americas markets with a flexible offering of powder and concentrated liquids; well-positioned to capture customers seeking reliable regional supply and technical service for diverse cellulose furnishes.

- Royce Global — notable for strength in anionic water-based systems and cationic basics for recycled and unbleached paper grades, offering a playbook for mills using high proportions of reclaimed fiber.

- Steiner-Axyntis — European technology and regulatory competence, with product claims emphasizing brightness, fiber affinity and on-site treatment compatibility, useful for packaging and high-value specialty grades.

- Archroma, BASF, DyStar — large chemical houses that provide scale, global registrations, and R&D capacity; their sustainability reporting and broad product portfolios make them default partners for multinational paper and packaging brands.

- Regional suppliers (Atul, Tiankun, Vipul) — cost-competitive producers with strong domestic market presence and flexible supply models; relevant for local sourcing and short lead-time requirements.

Recent moves — from Solenis’ sustainability reporting and price changes to DyStar’s integrated ESG disclosure — indicate the market is consolidating around verified environmental performance and reliable regulatory documentation as points of commercial differentiation. Buyers should validate supplier claims with third-party test data and insist on traceable compliance evidence during 2026 procurement cycles.

Regulatory and input risks shaping product strategy

New and evolving regulations require immediate attention. The 2025 REACH revisions introduce an “essential-use” framing for high-risk chemistries and broader restrictions that complicate legacy formulations. Food-contact standards (e.g., FDA 21 CFR sections relevant to paper and paperboard, BfR guidance and Ecolabel criteria) remain decisive gatekeepers for packaging applications. Meanwhile, widespread industry adoption of ZDHC MRSL, bluesign and similar frameworks raises the bar for supplier onboarding. For R&D and quality teams the implication is clear: prioritize low-migration, PFAS-free chemistries, and secure analytical/dossier evidence to avoid market access delays.

Action roadmap for 90 days, 6 months and 12 months

- 90 days: Undertake supply-risk mapping using our supplier-scorecard templates; commence audits of critical suppliers’ regulatory dossiers; flag any near-term price contracts for renegotiation or hedging.

- 6 months: Adapt technical specifications to prioritize low-risk chemistries; pilot on-site treatment compatibility tests; finalize strategic sourcing panels and secured capacity arrangements for peak seasons.

- 12 months: Execute M&A or JV moves where scorecards indicate clear bolt-on value; integrate sustainability claims into customer-facing contracts; roll out multi-supplier qualification for critical forms (powder vs. liquid) to reduce single-source exposure.

How PW Consulting’s report supports board-level decisions

This report is structured to bridge the gap between chemical technicality and commercial strategy. It translates macro forecasts (USD Million market sizing and 4.5% CAGR through 2032) into decision-ready inputs: contract clauses, procurement KPIs, M&A scorecards and an operational checklist for regulatory compliance. The analysis is intentionally non-prescriptive in micro-segmentation in public summaries: core subsegment metrics and supplier-level revenue breakdowns are contained in the full dataset and financial model to ensure clients can calibrate choices without oversharing competitive intelligence in open channels.

Next steps

For procurement leads, R&D heads, and corporate development teams preparing 2026 strategic plans, the report functions as a compact playbook — combining market sizing, supplier benchmarking, regulatory triage and execution templates. Access to the full dataset and model is recommended for any transaction, supplier renegotiation, or product reformulation workstream scheduled in 2026.

To review the complete dataset, supplier-level scorecards and scenario models, visit the PW Consulting report page for Worldwide Paper Direct Dyes Market — the full repository includes downloadable Excel models, supplier dossiers and a 36-slide board-ready summary designed to accelerate 2026 decision-making.

For detailed analysis of this topic, please visit the official page:Worldwide Paper Direct Dyes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com