Digital Calipers with LCD Display Market Overview: Key Drivers and Challenges

Other |

2026-04-20 06:53:09

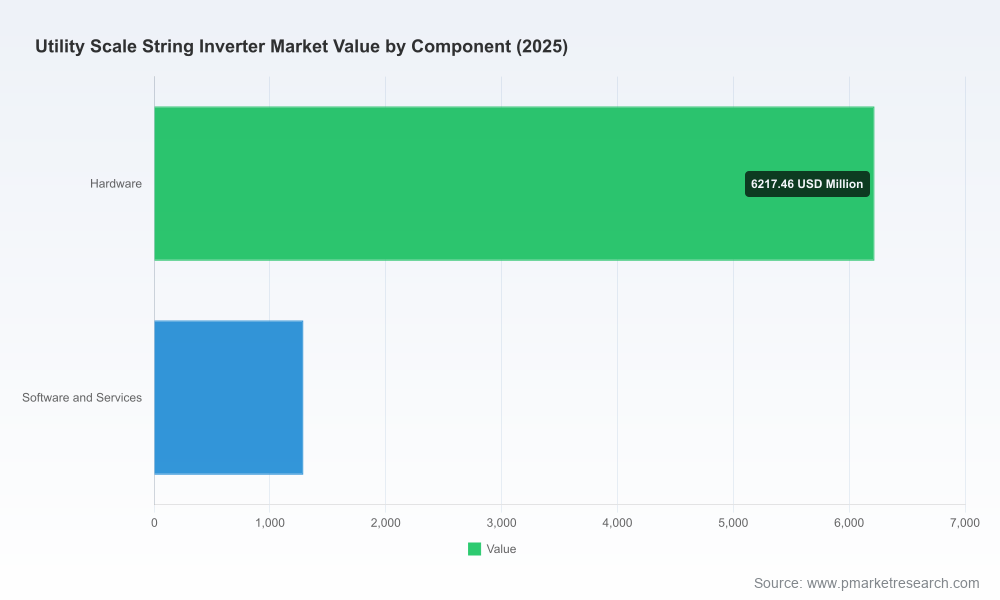

PW Consulting’s latest market intelligence, the Worldwide Utility Scale String Inverter Market report (base year 2025; historical 2020–2025; forecast 2026–2032), reframes how developers, EPCs, financiers and policy teams should approach utility-scale inverter procurement and technology strategy in 2026. The global market has grown from the lower billions in 2020 to an estimated USD 7.5 billion in 2025 and is forecast to expand at a compound annual growth rate of 8.74% across the 2026–2032 horizon. Market concentration remains meaningful — the top three and top five vendors together control a clear majority of the market — making supplier selection and negotiation strategy decisive factors in project economics and delivery risk.

Worldwide Utility Scale String Inverter Market

Policy timing and tax windows. Regulatory shifts enacted in 2025 and 2026 reconfigure the calendar for tax-driven project economics and create material execution deadlines for projects that intend to capture certain credits. Procurement timelines and equipment acceptance criteria must align with these windows to protect project value.

Worldwide Utility Scale String Inverter Market

Technology evolution is fast and consequential. String inverter architectures are rapidly adding grid-forming, AI-enabled diagnostics, and modular scales that blur the historical trade-offs between central and string topologies. Selecting the wrong vintage or architecture can lock a project into suboptimal grid compliance, longer commissioning or higher O&M risk.

Worldwide Utility Scale String Inverter Market

Supply-chain and cost pressure layers persist. Raw-material dynamics and labor inflation are increasing component and BOS line-item uncertainty. These cost pressures are asymmetric across regions and vendors — procurement strategy needs both hedging and staged contracting to preserve optionality.

Consolidation and vendor dominance matter. With a concentrated vendor landscape, counterparty risk and roadmap alignment are as important as headline pricing. Buyers must weigh device performance, service footprints and financial stability together.

At the macro level, utility-scale string inverters are no longer a niche: the segment has more than doubled in scale since 2020 and is on a steady trajectory toward mid-double-digit billion-dollar market size by the early 2030s. The 8.74% CAGR underpinning our forecast reflects continued utility-scale deployment, steady module power increases that favour high-current string architectures, and accelerating adoption of advanced inverter features demanded by modern grid codes.

For decision-makers in 2026, the implication is twofold: first, volume availability and product roadmaps will continue to mature, enabling more competitive total delivered cost of ownership; second, timing and specification discipline will determine whether projects capture first-mover advantages on new inverter features (e.g., grid-forming, advanced plant-level control) or pay premiums for late-stage retrofits.

Executive synthesis with actionable timelines: a two-page decision checklist tailored for developers, financiers, and asset owners summarizing procurement windows, preferred feature sets and contract guardrails for 2026.

Market sizing and forecast models: transparent assumptions for historical and forecast volumes, pricing drivers, and sensitivity scenarios (policy shock, commodity spike, accelerated decentralization).

Supplier scorecards: standardized, comparable performance matrices covering reliability metrics, grid-code compliance, warranty terms, service footprint, and financial strength — enabling objective shortlists for RFPs.

Product and technology deep dives: architecture-level comparison (modular block vs large string, grid-forming capability, ML/AI monitoring), production maturity, and upgrade pathway analysis for fielded systems.

Procurement playbooks and contractual templates: recommended specification language, acceptance test protocols (FAT/SAT), performance guarantee constructs, and O&M handover checklists to reduce commissioning and bankability friction.

Supply-chain risk heatmaps and mitigation options: component sourcing concentration, geo-risk overlays, and inventory strategies to de-risk multi-year build programs.

Financial impact tools: project-level TCO models, levelized cost sensitivity runs and a downloadable model with levers for inverter cost, downtime, degradation and service pricing.

The vendor ecosystem remains diverse, spanning global industrial players, specialized inverter manufacturers, and vertically integrated technology firms. Several vendor archetypes dominate strategic sourcing conversations:

Established global champions with broad product stacks and large manufacturing scale. These firms compete on high-efficiency designs, deep service networks and increasingly on software-enabled plant optimization. Their roadmaps emphasize grid-forming functionality and AI diagnostics to reduce site-level downtime.

Volume-focused Chinese manufacturers that combine rapid product iteration with aggressive price points and high shipment scale. Their offerings now include modular and high-current models tailored for modern high-power modules and dense layouts.

European and Japanese specialists focused on robustness, grid-integration expertise and compliance with stringent grid codes in mature markets. These vendors often bring conservative thermal and reliability margins that appeal to risk-averse banks.

New entrants and niche providers pushing high-voltage string topologies, advanced monitoring platforms and fully integrated PV+ESS solutions. Their differentiation levers are product-level efficiency and lifecycle service innovations.

Notable vendor developments in recent months underscore these trends: several major manufacturers launched or expanded high-capacity modular string platforms with grid-forming capability and AI-driven fault-detection; production capacity expansions in Europe were announced to capture growing demand for higher-capacity central and high-end string devices. These moves signal intensified competition on advanced features and localized manufacturing footprints — two variables that materially influence deal terms and lead times in 2026.

Align procurement with policy milestones. Map your pipeline against legislative and incentive deadlines. If tax-treatment or commissioning windows matter for project IRR, build contractual milestones and supplier SLAs that mirror those deadlines to avoid value erosion.

Prioritize technical specifications that matter to lenders and grid operators. Grid-forming capability, extended ambient-temperature performance and advanced fault-detection are increasingly minimum requirements in new tenders — include these as pass/fail criteria rather than optional add-ons.

Use staged purchase strategies to balance price and technology risk. Combine firm-price, near-term tranches with options for later-year volumes to capture potential deflation in component costs and new product vintages without sacrificing delivery certainty for early-stage projects.

Diversify supply partners by risk profile. Pair incumbent global manufacturers with a second-source vendor that offers complementary capabilities (e.g., superior digital services or local manufacturing) to mitigate single-point exposure.

Embed performance and upgrade pathways into contracts. Require firmware update rights, clear obsolescence policies and defined upgrade pricing for new grid-code requirements and digital features to protect long-term plant value.

Rethink O&M and digital ownership. Evaluate whether to buy maintenance-as-a-service or retain digital telemetry ownership for future merchant-market participation and AI-driven performance optimization; the right choice differs by asset risk appetite.

This report is designed as an executable intelligence asset, not purely an academic forecast. It couples robust market sizing with procurement-oriented tools and supplier due-diligence templates that materially shorten RFP timelines, clarify bankability questions and reduce negotiation cycles. Critically, the document separates headline macro views from transaction-ready annexes: buyers can move from strategic alignment to draft tender within days, using our templates and vendor scorecards.

Our public summary deliberately omits the granular regional and application-level splits, vendor shipment tables and price decks that most directly drive transaction decisions. Those detailed segmentations, scenario-runworkbooks and vendor-level shipment forecasts are available in the full report and downloadable models on the PW Consulting report page. For procurement teams, investors and policy advisors who need the underlying numbers to populate financial models or to run competitive tender simulations, the full dataset and model templates are the essential companion to this strategic briefing.

In a market where vendor roadmaps, policy timing and supply-chain pressure interact to reshape project economics, the 2026 decisions you make about inverter architecture, supplier mix and contractual safeguards will define profitability over a multi-decade asset life. PW Consulting’s Worldwide Utility Scale String Inverter Market report delivers the macro clarity, the competitive nuance and the operational tools to make those decisions with confidence.

For detailed analysis of this topic, please visit the official page:Worldwide Utility Scale String Inverter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com