The Foundational Role of Nigeria Telecom in Driving National Digital Transformation

Other |

2026-01-05 09:48:43

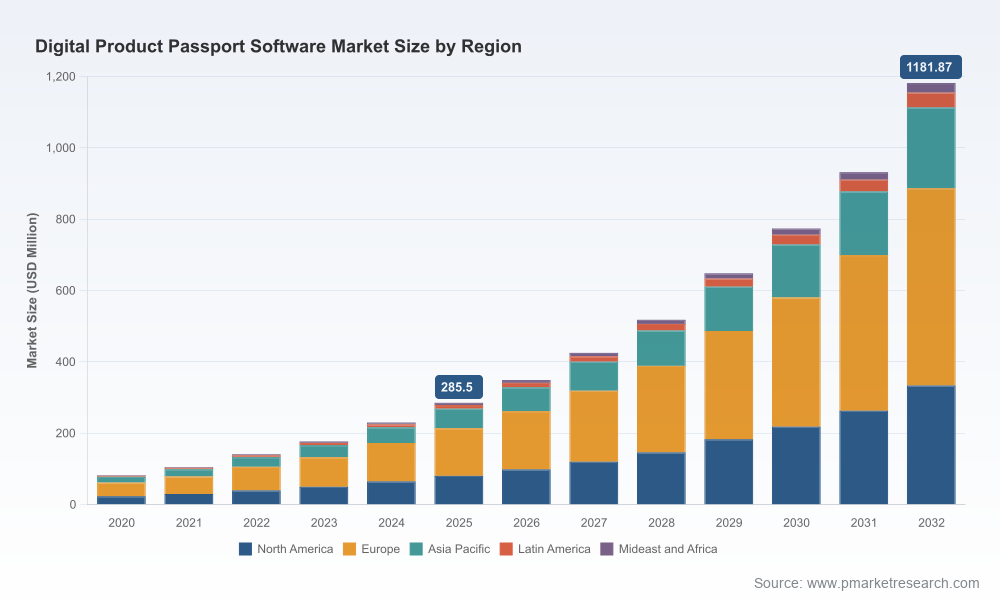

As regulatory timelines converge and procurement gates tighten in 2026, Digital Product Passport (DPP) software is moving from pilot projects to procurement line items. PW Consulting’s latest market research—Digital Product Passport Software Market (base year 2025; forecast period 2026–2032)—quantifies what leaders already feel: demand is accelerating. Between 2020 and 2025 the global market expanded rapidly, and our model projects continued high‑double‑digit annual growth through 2032 at a compound annual growth rate (CAGR) of 22.5%. The market crossed notable scale in 2025 and is forecast to further scale in 2026 and beyond, delivering new commercial and compliance imperatives for manufacturers, retailers, platforms, and service providers.

Digital Product Passport Software Market

Regulatory inflection: The operational roll‑out of central registries and sector‑specific mandates is turning DPPs into de facto market access enablers. The EU’s phased implementation plan, paired with registry operationalization in mid‑2026, elevates timing from “nice‑to‑have” to “required for market placement” for affected sectors.

Digital Product Passport Software Market

Procurement and public spending pressure: With sustainability criteria increasingly embedded into public procurement, companies without credible DPP strategies face exclusion risks and reputational exposure.

Digital Product Passport Software Market

Vendor landscape and ecosystem maturity: Vendors have moved from experimental feature sets to operational platforms addressing traceability, compliance, lifecycle data, and consumer interfaces—creating clearer vendor selection paths but also complexity in integration choices.

PW Consulting’s topline model shows the market moving from initial traction to commercial scale: discrete annual figures reflect one of the fastest‑growing SaaS/subscription‑adjacent sectors we track. With a 22.5% CAGR across the forecast window, buyers should anticipate both growing vendor choice and acceleration of product roadmaps—especially in capabilities tied to regulatory compliance, material traceability, and lifecycle analytics. The market concentration metrics point to a moderately fragmented field: incumbent and specialist providers capture meaningful shares, but a long tail of niche and regional players persists. That fragmentation creates both integration risk and competitive opportunity for platform consolidators, systems integrators, and data‑centric incumbents.

Compliance as a functional requirement: EU mandates and national enforcement mean DPP systems are now evaluated as compliance infrastructure—equivalent to safety or chemical compliance platforms. Non‑compliance risks include market access denial, regulatory fines, and procurement disqualification.

Data protection: DPP implementations that touch personal data must be designed against stringent privacy standards. GDPR‑aligned principles—data minimisation, explicit consent mechanics, and rapid breach notification—are non‑negotiable design constraints and procurement criteria.

Operational cost control: Cloud‑hosted DPP architectures deliver speed and scalability but introduce new cost and governance levers. Organizations that neglect cloud cost optimisation can see material overspend; conversely, disciplined cloud governance reduces TCO and improves scalability for enterprise footprints.

Registry integration and standards: Central registries and standards (e.g., GS1 Digital Link and emerging EU registry interfaces) are converging. Practical interoperability—APIs, common identifiers, and harmonised metadata models—will determine which platforms provide durable value versus tactical point solutions.

Our report is structured for practitioners who must decide this year. It bridges strategic framing and execution tools, and includes:

Decision frameworks to align DPP investments with product portfolios, channel strategies, and regulatory timelines—scoring templates for priority setting across product lines.

Procurement checklists and RFP language focused on compliance, data governance, API maturity, and total cost of ownership—templates you can insert directly into vendor selection processes.

Integration playbooks for common enterprise architectures, including ERP, PLM, WMS and aftermarket systems—detailed patterns for phased rollouts that minimise operational disruption.

Cost modelling modules that translate vendor commercial models (subscription, per‑SKU, transaction fees) and cloud operating models into five‑year TCO comparisons.

Risk assessment matrices for regulatory, data, and supplier risks—scenarios and mitigation actions timed to 2026 milestones.

The vendor ecosystem mixes vertical specialists, platform incumbents, and new entrants. PW Consulting’s qualitative assessment highlights differentiation vectors that matter to procurement committees: provenance and traceability fidelity, registry and standards support, lifecycle and resale marketplace integration, compliance data depth (chemical, safety, carbon), and enterprise integration capabilities.

Spherity (Cologne, Germany) brings a track record in battery passports and compliance workflows oriented to lifecycle management and secondary‑market integration—valuable when battery compliance timelines are operative.

Kezzler (Oslo, Norway) emphasises product identity and GS1 Digital Link support across multiple sectors, supporting projects that require broad traceability and consumer‑facing interfaces.

TrusTrace (Stockholm, Sweden) focuses on fashion and textiles with end‑to‑end supplier traceability and consumer verification experiences—particularly relevant ahead of textile registry enforcement.

Arianee (Paris, France) leverages blockchain paradigms for ownership tracking and consumer engagement in luxury goods—useful for brands where provenance drives value.

3E (3E Exchange, Carlsbad) integrates regulatory safety and chemical compliance data into passport outputs—critical for sectors where chemical reporting is mandatory.

Renoon (Netherlands) and iPoint‑systems (Reutlingen, Germany) offer platforms targeted at operational integration for fashion and product compliance workflows respectively—good fits for brands with heavy ERP/PLM dependencies.

Circularise (Netherlands) and Avery Dennison (atma.io) provide complementary approaches emphasizing material traceability and retail scale support—one leveraging blockchain for material transparency, the other combining tag/label hardware and platform services for high‑volume retail deployments.

Carbonfact (France/USA) brings automated, LCA‑driven passport generation—important where environmental impact data must be published at scale.

Recent market activity underscores movement from pilots to production: registry launches, industry pilots in textiles, and major systems integrator collaborations are all accelerating procurement timelines. Buyers should expect intensified vendor consolidation and deeper SI partnerships through 2026–2027.

Map mandatory exposure first. Use regulatory timelines to prioritise product families for DPP implementation—treat affected SKUs as critical compliance assets.

Require modular architectures. Procure platforms with clear API contracts and modular onboarding so pilots can evolve into enterprise rollouts without rip‑and‑replace risk.

Embed data governance from day one. Define data minimisation, consent flows, retention policies, and encryption standards upfront to avoid retrofits under privacy regimes.

Design for cost transparency. Include cloud cost benchmark clauses, rights to audit, and consumption caps in contracts to manage the operational spend trajectory.

Partner for lifecycle value. Evaluate vendors not only on compliance outputs but on aftermarket and circularity integrations that unlock resale, repair, and recycling revenue pathways.

Stress test vendor registry readiness. Demand proof points for registry connectivity and standards compliance; require timeline commitments and sandbox access prior to pilots.

Our report is designed as a working tool for procurement, sustainability, and product teams. It translates market growth dynamics and regulatory timing into executable procurement artifacts, cost models, and vendor evaluation frameworks. We surface where value will appear—compliance risk mitigation, new revenue from circular channels, and cost efficiencies from standardised data flows—and where governance must be strengthened to protect brand and market access.

For executives finalising 2026 budgets, the window to plan, pilot, and integrate DPP capability is now. PW Consulting’s full Digital Product Passport Software Market report includes the detailed vendor benchmarking, procurement templates, and integration playbooks that procurement and product teams need to move from pilot to production with confidence. To access the full dataset, vendor scorecards, and the downloadable RFP templates, visit our research portal and secure the toolkit designed for immediate deployment in 2026.

For detailed analysis of this topic, please visit the official page:Digital Product Passport Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com