Worldwide Slaked Lime Market — Strategic Outlook for 2026: PW Consulting Preview

Executive snapshot

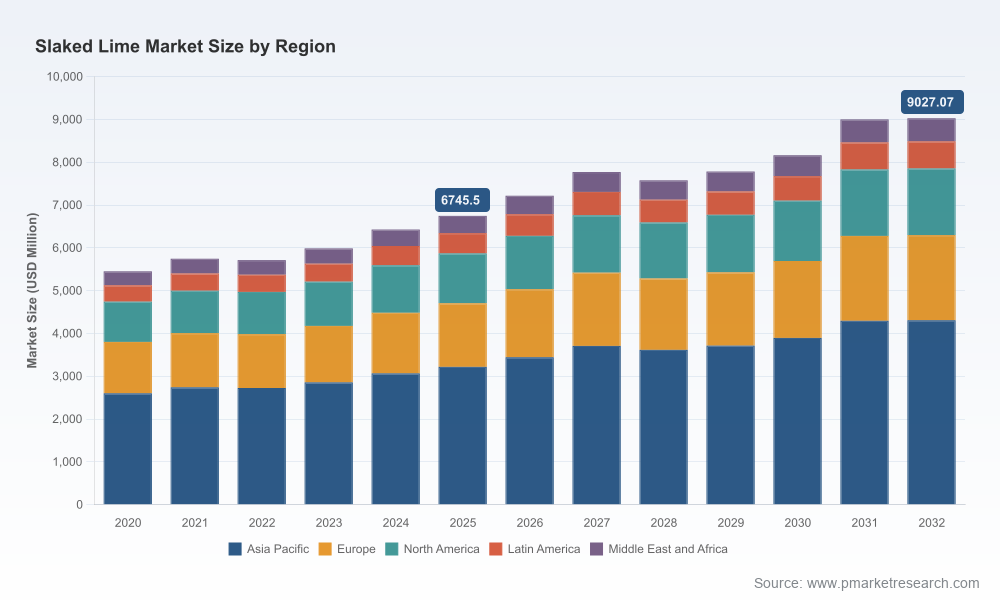

PW Consulting’s latest market research on the Worldwide Slaked Lime (hydrated lime) market equips corporate strategists, investors, and public-sector planners with a forward-looking intelligence package tailored to 2026 decision cycles. Built on a rigorous base-year of 2025 and a historical analysis covering 2020–2025, the study models supply, demand, and cost dynamics across the 2026–2032 forecast horizon. At the macro level, the global market is poised to grow from approximately USD 6,745.5 Million in 2025 toward the USD 9,000+ Million zone by the end of the forecast, reflecting a compound annual growth rate (CAGR) of roughly 4.25% across 2026–2032.

Worldwide Slaked Lime Market

Why this matters for 2026 decisions

- Timing: 2026 represents a strategic inflection point for capital allocation and contractual commitments — new kiln investments, long-term offtake agreements, and water/wastewater project procurements are being planned now.

- Risk-adjusted sizing: Our report translates headline growth into actionable capacity, inventory, and logistics scenarios that reconcile short-term supply shocks with multi-year demand trajectories.

- Competitive positioning: With the market exhibiting moderate concentration (CR3 ≈ 18.4%, CR5 ≈ 26.15%), opportunities exist for regional scale plays, niche specialty products, and service-based differentiation.

Market trajectory and headline metrics

Following a period of cyclical volatility in the early 2020s, the slaked lime market demonstrates steady expansion driven by regulatory-led environmental demand, continued urban infrastructure investment, and industrial process requirements. Our scenario suite maps a base-case pathway that delivers roughly 4.25% CAGR over 2026–2032, with upside tied to accelerated flue-gas desulfurization roll-outs and municipal water treatment modernizations, and downside exposed to sustained energy-price shocks and freight disruptions.

Worldwide Slaked Lime Market

These macro dynamics are underpinned by two structural realities: (1) slaked lime is a commoditized, energy- and logistics-sensitive product derived from quicklime (itself the calcined product of limestone); and (2) the manufacturing footprint is capital- and energy-intensive, which makes marginal cost curves sensitive to fuel costs and kiln technology choices. PW Consulting’s models quantify how variations in fuel price, kiln efficiency, and freight rates propagate to regional margin pressure points — critical inputs for 2026 procurement and CAPEX planning.

Worldwide Slaked Lime Market

Competitive landscape — what incumbents and challengers are doing

The market is served by a mix of multinational incumbents and regional specialists. Leading players such as Carmeuse and Lhoist bring global platforms and product breadth; North American leaders like Graymont, Mississippi Lime Company and United States Lime & Minerals are executing capacity and partnership plays to secure water and environmental customers; Northern European suppliers such as Nordkalk are emphasizing operational resilience in high-regulation markets. A long tail of national and regional producers rounds out supply, offering local service advantages and niche specialty grades.

- Expansion and capacity: Recent industry actions include commissioning of expanded hydrated lime facilities and brownfield capacity additions in early 2026, reflecting supplier responses to rising environmental and municipal demand.

- Partnerships and vertical alignment: Strategic long-term offtake arrangements between suppliers and major water authorities have been announced, locking in volumes and underpinning mid-scale investments in purification upgrades.

- Sustainability and modernization: Several producers have publicly committed to sustainable kiln projects and capacity consolidation to lower unit energy consumption and emissions intensity.

PW Consulting’s report provides company-level profiles and a comparative scorecard that evaluates strategic levers — production footprint, grade portfolio, energy efficiency, logistics exposure, and contract maturity. For 2026, these levers are the determinative variables for market share momentum and margin resilience.

Operational and supply-chain dynamics that will shape margins in 2026

Operators face a confluence of input pressures and demand catalysts. Key technical and cost facts driving our analysis:

- Raw material and production fundamentals: Slaked lime is produced by hydrating quicklime, which itself is made through limestone calcination. The availability and quality of limestone deposits remain a competitive advantage for low-cost production.

- Energy intensity: Lime kilns are energy-intensive. Industry benchmarks indicate fuel requirements in the range of roughly 4.5–10 MJ per kilogram of quicklime produced. This range translates into material margin sensitivity to natural gas and fuel oil price swings.

- Feedstock pricing snapshots: In Q1 2026, reported quicklime prices varied materially across markets (examples: ~USD 156/MT in China, ~USD 170/MT in the Netherlands, and ~USD 128/MT in the USA), illustrating regional cost dispersion drivers that affect export flows and competitiveness.

- Logistics and geopolitics: Early-2026 geopolitical frictions have pushed freight rates and surcharges 15–25%, increasing landed costs for cross-border shipments and altering vendor selection criteria for large municipal buyers.

- Regulatory demand pull: Stricter pollution control frameworks in major markets continue to underpin demand for hydrated lime in flue gas desulfurization and water/wastewater treatment projects.

Report contents — practical tools for 2026 implementation

PW Consulting’s full report blends strategic narrative with a suite of practitioner-ready deliverables designed to be used directly in corporate planning and procurement cycles. Highlights include:

- Market sizing and forecast engine: Transparent methodology with base-year calibration (2025), historical series (2020–2025), and probabilistic forecasts for 2026–2032, enabling stress-testing against bespoke scenarios.

- Supply and demand mapping: Plant-level sourcing maps, capacity utilization curves, and regional import-export balances to support sourcing and logistics decisions.

- Cost-to-serve and breakeven tables: Unit-cost models reflecting kiln efficiency tiers and fuel-price sensitivities, with downloadable Excel models for bespoke sensitivity analysis.

- Regulatory and project pipeline database: A curated tracker of water treatment and air pollution control projects by procurement timeline and funding status, matched to anticipated hydrated lime demand.

- Competitive scorecards and M&A radar: Comparative assessments of major producers and a shortlist of acquisition targets by strategic fit (scale, geography, product grade).

- Actionable playbooks: Tactical guidance for buyers (contract design, hedging strategies), suppliers (pricing logic, capacity investment sequencing), and investors (value-creation templates for brownfield upgrades and sustainability-linked refinancing).

Note: The report intentionally omits open distribution of granular regional and application split tables on the free preview. Detailed segment-level datapacks, including comprehensive regional and end-use demand breakdowns and cell-level revenue figures, are available in the full report package.

Strategic recommendations for 2026

- For producers: Prioritize efficiency retrofits and flexible fuel options for kilns to reduce operating-cost volatility. Target near-term capacity investments where long-term offtake agreements from municipal and industrial customers are already secured.

- For buyers (water authorities, environmental contractors): Lock in multi-year supply contracts with indexed pricing and clause protections for freight and energy pass-throughs. Consider geographically diversified sourcing to mitigate single-route disruptions.

- For investors and acquirers: Seek assets that offer both proximity to limestone reserves and potential for efficiency upgrades; small-to-mid brownfield acquisitions can deliver rapid EBITDA uplift through modernization and commercial integration.

- For policymakers and planners: Recognize the knock-on supply sensitivity caused by freight and energy markets; consider strategic stockpiles or flexible procurement windows for critical infrastructure projects.

How PW Consulting supports execution

Beyond the report, PW Consulting offers bespoke advisory services to convert insights into contracts, investments, and implementation programs: supplier due diligence and benchmarking, FEED-level input-cost modeling for kiln projects, offtake negotiation support, and regulatory impact assessments tuned to national jurisdictions. Our team pairs market-level forecasting with plant-level engineering economics to accelerate decision-making and de-risk 2026 commitments.

Next steps and where to find the full intelligence

This preview outlines the strategic contours that should guide slaked lime-related decisions in 2026. PW Consulting’s full Worldwide Slaked Lime Market report contains the proprietary data, downloadable models, and segment-level analytics necessary to finalize procurement strategies, investment memos, and operational plans. For access to the complete datapacks and bespoke advisory engagements, please visit our report page or contact our industry practice team.

For detailed analysis of this topic, please visit the official page:Worldwide Slaked Lime Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com