Worldwide Boiling Water Reactors Market: Strategic Outlook for 2026 Decision‑Making

As governments and utilities shift from short‑term energy security fixes to durable low‑carbon baseload strategies, boiling water reactor (BWR) technology is re‑emerging as a pragmatic option for decarbonization and grid resilience. PW Consulting’s new Worldwide Boiling Water Reactors Market research—anchored on a 2025 base year and spanning historical performance (2020–2025) with a detailed forecast to 2032—provides the market context, competitive intelligence, and near‑term playbooks that corporate decision‑makers need to act confidently in 2026.

Worldwide Boiling Water Reactors Market

Headline market trajectory and what it means for 2026

Our market model shows the BWR market recovering from near‑term volatility and resuming steady growth: after a mid‑cycle expansion to an estimated USD 3,340.0 million in 2025, the market is forecast to expand to roughly USD 3,673.95 million in 2026 and to reach approximately USD 4,495.8 million by 2032. The compound annual growth rate across the forecast period (2026–2032) is projected at 4.33%. These aggregate dynamics represent both opportunity and constraint—sufficient scale to sustain incumbent technology providers and specialist service firms, yet tight enough that strategic timing, partner selection, and regulatory positioning will determine winners in 2026.

Worldwide Boiling Water Reactors Market

Why this report matters to executives planning in 2026

- Timing capital deployment: The 2026 inflection point in our forecast suggests that near‑term projects—especially those leveraging simplified or modular BWR designs—will capture outsized value if financing, permitting, and supply‑chain arrangements are locked in this year.

- Selecting partners, not just vendors: The market is concentrated around a handful of global suppliers and JV structures. Understanding the commercial models and contractual norms of these players will make or break project economics when negotiating EPC, fuel supply, or long‑term service agreements.

- De‑risking fuel and material exposure: Raw material volatility (for example, U3O8 price dislocations observed in early 2024) and emerging trade restrictions are reshaping procurement strategies. This report translates spot‑price and policy signals into procurement hedging and inventory playbooks tailored to BWR lifecycles.

- Regulatory and design risk management: Revised international safety guidance and localized seismic design expectations are changing scope and contingency sizing for new builds and major modernizations. Our regulatory tracker and design sensitivity matrices are built to inform contingency reserves and schedule buffers for 2026 approvals and tenders.

Core insights you will only find in the full PW Consulting report

- Scenario‑based capex/opex models comparing traditional builds with simplified and small modular BWR options under multiple policy and commodity price environments.

- Supplier scorecards and negotiation playbooks that map contractual levers to perceived vendor strengths and delivery risks—designed for procurement officers and project finance teams.

- A regulatory roadmap with milestone windows for permitting and safety approvals across major nuclear jurisdictions, plus modeled impacts of recent international guidance changes on schedule and cost.

- Supply‑chain heatmaps that quantify exposure to critical inputs and identify low‑cost mitigation steps (localization, inventory strategies, and strategic stockpiles).

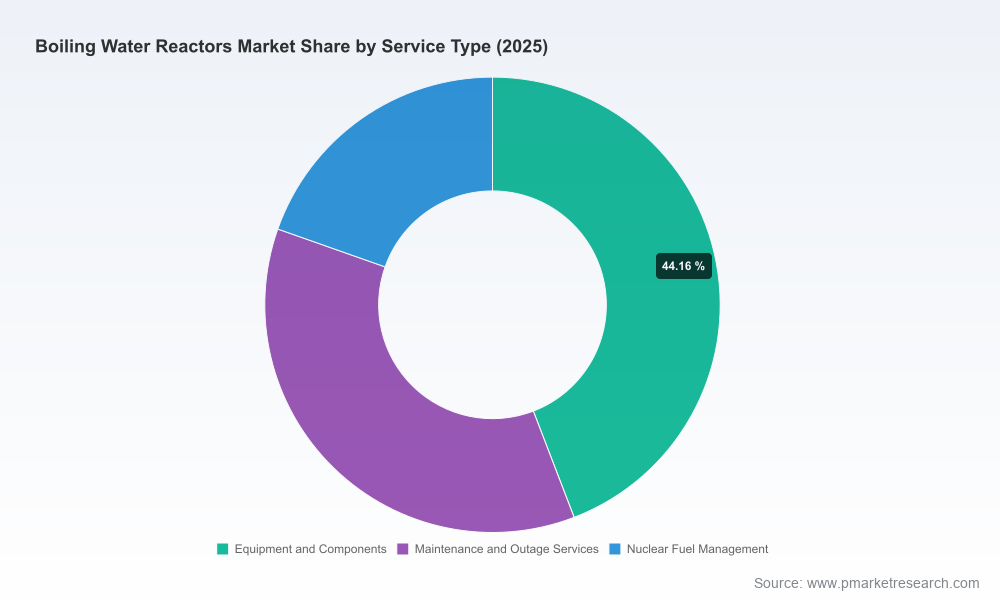

To preserve the strategic value of the dataset for subscribers and prospective clients we deliberately withhold detailed regional and application split tables from this release; the full report contains those granular breakouts and the underlying models.

Worldwide Boiling Water Reactors Market

Competitive landscape and 2026 tactical considerations

The market displays meaningful concentration among a small number of established players (our concentration analysis indicates that the top three firms account for a substantial majority of market share, and the top five approach near‑total share), which shapes the competitive dynamics for new entrants, EPC consortia, and investors seeking exposure to BWR technology.

- GE Hitachi Nuclear Energy (Wilmington, NC) — As the primary global supplier of BWR technology and the steward of the certified BWRX‑300 design, GEH has converted R&D momentum into visible project trailheads. Recent program milestones—early construction pours, regulatory design approvals in Canada, and site selections in the U.S.—underscore their near‑term commercial readiness. For 2026, GEH is a logical focal point for utilities and developers seeking modular deployments; our report maps realistic delivery timelines and sets expectations for licensing‑to‑commercial operation intervals.

- Hitachi‑GE Nuclear Energy, Ltd. (Tokyo) — With deep experience delivering Advanced BWRs (ABWRs) and an established engineering, procurement, and maintenance (EPCM) footprint, Hitachi‑GE remains a partner of choice for large baseload projects and fleet modernization. Our analysis highlights how their service and modernization offerings can be used to extend asset life or improve thermal efficiencies as part of phased decarbonization strategies.

- Toshiba Energy Systems & Solutions Corporation (Tokyo) — Toshiba’s ABWR heritage and its capabilities in fuel and modernization projects give it strength in markets pursuing full‑scale new builds and existing fleet upgrades. For 2026, Toshiba’s competitive position will depend on how quickly it converts engineering pipelines into bankable EPC proposals in markets with clear policy support.

Collectively, these incumbents create a high barrier to entry but also present partner opportunities for governments and utilities seeking proven supply chains. Our vendor benchmarking, included in the full report, quantifies these tradeoffs in procurement scorecards and bid‑evaluation matrices.

Regulatory, commodity and policy signals shaping 2026 choices

- Uranium and fuel supply volatility: Spot uranium price spikes and trade policy actions—such as prohibitions on certain imports and incentives for domestic supply development—have immediate procurement consequences. Our fuel‑supply scenario engine shows how different procurement mixes affect levelized cost of electricity for BWR projects across deployment timelines.

- Safety guidance and seismic design: Revisions to international safety guidance for seismic design create new baseline requirements for light water reactor projects. The practical effect is an increase in front‑end engineering scope for certain sites—an input our cost model translates into contingency and schedule buffers for 2026 bids.

- Policy incentives and public finance: Investment tax credits and similar mechanisms materially alter project IRRs. For example, tax credit programs that cover a portion of new nuclear capacity tilt the economics toward early starts; our policy sensitivity worksheets allow CFOs to simulate financing structures that capture these incentives while maintaining covenant compliance.

Actionable recommendations for 2026

- Lock modular options into procurement pipelines: For organizations with 2026‑2028 deployment windows, prioritize options that enable staged capital outlay (e.g., modular units or simplified BWR variants) and secure conditional supply agreements.

- Negotiate dual‑track fuel strategies: Combine medium‑term contracts with short‑term spot exposure and strategic stockpiles to balance cost and availability risk given recent uranium price volatility and evolving import restrictions.

- Use vendor scorecards in RFPs: Require evidence of recent licensing approvals, demonstrated manufacturing scale, and service‑level guarantees. Our sample RFP clauses and evaluation grid (in the full report) accelerate procurement timelines while protecting owner interests.

- Integrate regulatory scenarios into financial models: Build permit and seismic standard contingencies into schedule build‑ups and financing covenants to avoid downstream covenant breaches and refinancing exposures.

- Plan for consolidation and strategic partnerships: Given market concentration, consider alliances—equity, JV, or offtake—to gain access to intellectual property and delivery capacity without the cost and time of de novo capability building.

What’s inside the PW Consulting deliverable

The full Worldwide Boiling Water Reactors Market report package includes:

- Comprehensive market sizing and seven‑year forecasts (2026–2032) with downloadable models.

- Vendor profiles, capability matrices, and recent development timelines for major incumbents.

- Detailed, actionable sections: procurement playbooks, contract clauses, supply‑chain risk heatmaps, regulatory trackers, and CAPEX/OPEX benchmarking and sensitivity analyses.

- Scenario engines for commodity price shocks, policy changes, and technology adoption rates—enabling rapid run‑time simulations for boardroom decision sessions.

- Executive briefings and a one‑day workshop option with our senior analysts to convert insights into a 100‑day action plan for 2026.

Note: This press release intentionally omits the detailed regional and application split tables and core segment numeric breakdowns—to preserve their operational value for report subscribers and clients. The full dataset and interactive models are available through the PW Consulting report portal.

Next steps for leaders preparing 2026 programs

- Schedule a briefing with PW Consulting to walk through the model under your project assumptions; we can run bespoke scenarios within 48–72 hours.

- Use our vendor negotiation kit to harmonize terms across EPC and service contracts before issuing tenders in 2026.

- Engage early with regulators using the report’s permitting timeline as a baseline to compress approval windows where possible.

In 2026, timing and preparation will determine who captures value as BWR opportunities migrate from concept to construction. PW Consulting’s Worldwide Boiling Water Reactors Market report equips leadership teams with the forecasts, supplier intelligence, and execution playbooks necessary to convert policy momentum and technological maturity into bankable projects. For the full data, models, and an executive briefing, please visit the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Worldwide Boiling Water Reactors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com