Worldwide Rail Air Conditioning Market — Strategic Briefing for 2026 Decision Makers

By PW Consulting — Senior Strategic Advisor & Chief Industry Analyst

Worldwide Rail Air Conditioning Market

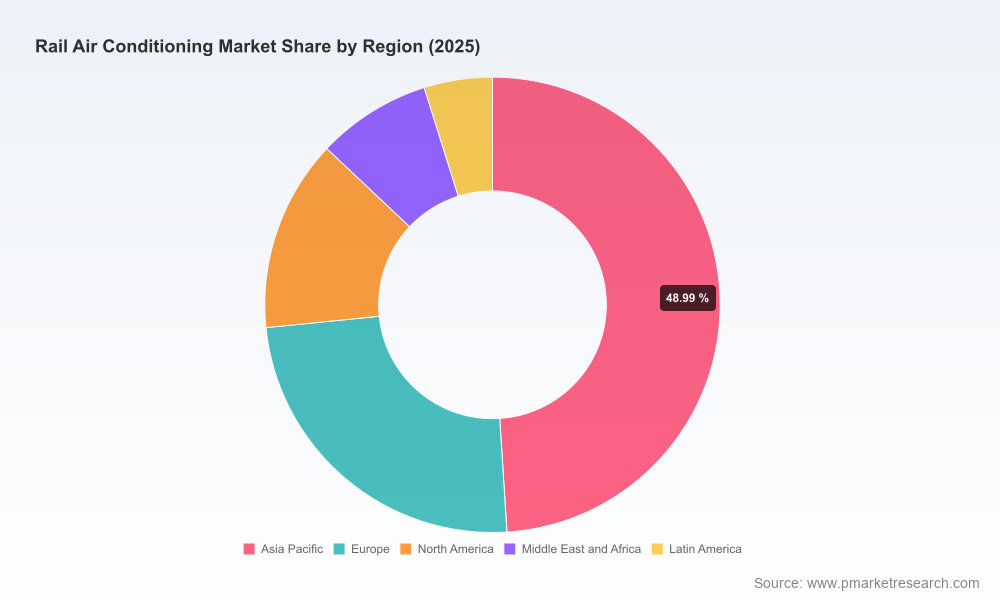

As rail operators, rolling-stock OEMs, component suppliers and investors set budgets and strategic priorities for 2026, a clear, executable view of the rail air conditioning (AC) market is essential. Our latest Worldwide Rail Air Conditioning Market study — anchored on a 2025 base year and projecting through 2032 — delivers that view. The market reached approximately USD 14,050 Million in 2025 and, under our base forecast, expands to more than USD 21,900 Million by 2032, reflecting a compounded annual growth rate (CAGR) of roughly 6.55% across the 2026–2032 period. This briefing distills the most consequential trends and the practical implications for leaders making planning, procurement, product and M&A decisions in 2026.

Worldwide Rail Air Conditioning Market

What this briefing delivers — and what the full report contains

- A concise, actionable executive framework that ties macro growth to immediate operational choices: fleet refresh timelines, retrofit prioritization, supplier selection and CAPEX phasing for 2026–2028.

- Scenario-ready intelligence: our forecast model, sensitivity runs (commodity shocks, refrigerant rollouts, certification timelines), and practical procurement levers that reduce unit cost and delivery risk.

- Supplier benchmarking and capability mapping across technology, certification, manufacturing footprint and aftermarket service — enabling targeted partner selection or M&A shortlist creation.

- Risk and opportunity playbooks for regulators, operators and suppliers — including compliance checklists, retrofit pathways and expected OPEX/energy-savings payback windows under common adoption scenarios.

- Note on disclosure: this briefing intentionally highlights strategic insight while withholding the granular segment and regional tables that drive our models. The full datasets, regional splits and application-level modelling are available in the complete report and online portal.

Macro dynamics that will shape 2026 choices

The mid-decade mandate for rail AC planning is defined by simultaneous pressures on cost, carbon and reliability. Growth in global rail investment, ongoing modal shifts toward electrified public transit, and accelerated fleet renewals are underpinning steady market expansion. Against this demand backdrop, three structural forces should inform every board-level discussion in 2026:

Worldwide Rail Air Conditioning Market

- Regulatory acceleration. EN 14750 continues to set stringent performance expectations for rail HVAC durability across extreme ambient ranges, and recent EU regulations mandate the use of low-global-warming-potential (GWP) refrigerants in new systems. These rules are not just compliance items — they materially affect unit design, validation timelines and supplier qualification.

- Commodity and labor pressure. The cost base for HVAC heat-exchangers is being reshaped by material swings (notably copper) and regional labor scarcity. In 2026, procurement strategies must explicitly incorporate raw-material pass-through mechanisms, hedging or localization options to protect margins.

- Technology shift toward system efficiency and modularity. Adoption of inverter-driven compressors, brushless DC motors and modular HVAC architectures is accelerating. These technologies promise meaningful life-cycle energy savings and easier integration into multi-voltage, multi-climate fleets but require reworked testing and warranty frameworks.

Competitive landscape — what leading suppliers are doing now

The market is served by a mix of global Tier-1 system integrators, specialized HVAC OEMs and regional suppliers. The current environment rewards companies that can combine energy-efficient technology, robust certification credentials and the supply-chain flexibility to support large fleet programs.

- Knorr-Bremse — As a long-established HVAC system provider, Knorr-Bremse’s recent roll-out of a next-generation metro HVAC platform that targets ~20% energy savings signals a strategic pivot to energy-first product positioning for urban transit customers. For buyers, this means higher expectations for baseline energy performance in RFQs and accelerated substitution of legacy units in metros.

- Faiveley Transport / Wabtec — With strengths in modular HVAC architectures and recent nominations on high-volume regional programs, this group is positioning modularity and rapid field serviceability as key differentiators for expanding urban and intercity fleets.

- Toshiba Carrier & Mitsubishi Electric — Japanese OEMs remain leaders in lightweight, inverter and low-power designs, often favored for high-speed and demanding climate operations. Their technology orientation favors premium OEM partnerships and export projects where reliability and weight savings matter.

- Hitachi, Alstom (ex-Bombardier) and Siemens Mobility — These systems integrators are integrating HVAC as part of broader rolling-stock offers, emphasizing energy recovery features, certification compliance and system-level warranties. Their scale advantage is increasingly relevant in large trainset procurements.

- Regional suppliers such as Guangzhou Metro AC Equipment and specialist players like STULZ and Aqua Group — These firms compete effectively on cost, speed-to-market and regional service networks, particularly in high-growth urban transit markets.

Strategic takeaway for 2026: procurement teams should treat supplier selection as a multi-dimensional decision in which energy performance, refrigerant roadmap, aftermarket capability and supply-chain resilience are scored alongside price and delivery. Expect deals to include tighter performance SLAs and acceptance testing tied to real-world energy and environmental metrics.

Technology and regulatory inflection points to monitor

- Low‑GWP refrigerant adoption — As regulators push Stage V-equivalent requirements, OEMs and operators must accelerate trials and validation of alternative refrigerants. Specification updates that mandate refrigerant transition timelines will affect procurement windows and unit lifecycle costs.

- Brushless DC motors & inverter control — These technologies are delivering measurable energy reductions and lower maintenance needs. Pilots completed in 2024–2025 demonstrate potential lifecycle OPEX improvements that materially shift total cost of ownership (TCO) math for fleets with high duty cycles.

- Certification and testing — New validation activities for major projects (e.g., high-speed corridors) emphasize the need for suppliers to maintain up-to-date EN 14750 and equivalent registrations, and for buyers to require proof through independent testing and factory acceptance protocols.

- Supply-chain concentration and raw material exposure — Short-term commodity shocks (copper price increases, for example) and skilled labor shortages in key manufacturing regions are likely to continue into 2026, pressuring lead times and margins unless mitigated through sourcing strategies.

How to translate market intelligence into 2026 actions — six priority moves

- Update procurement specifications to embed energy performance, refrigerant roadmap and maintenance metrics. Tie payments and acceptance to these KPIs to de-risk long-term OPEX.

- Run targeted retrofit pilots focused on brushless-DC and inverter packages for high-utilization fleets to build live OPEX data and refine payback assumptions before full-scale rollouts.

- Develop supply-contingency plans that address commodity volatility — consider long-term material contracts, component dual-sourcing and near-shore assembly for critical heat-exchanger elements.

- Prioritize suppliers with demonstrable certification and testing credentials for projects in regulated geographies; require factory and on-track validation evidence as part of nomination criteria.

- For investors and M&A teams: evaluate targets on the basis of product roadmap alignment (low-GWP readiness, inverter/EFM capability), aftermarket service revenues and regional service networks rather than on installed-unit counts alone.

- Embed scenario modelling in board-level planning: run downside scenarios that stress copper and labor cost increases, and upside scenarios that assume faster electrified fleet deployment — our forecast model (base 2025; 2026–2032 projection) is designed for these runs.

What PW Consulting’s report offers to decision-makers

The comprehensive report provides the proprietary forecast model, a supplier capability matrix, detailed regulatory timelines, and procurement playbooks tailored to operators, OEMs and suppliers. Our modelling is transparent and scenario-enabled, allowing your team to stress-test outcomes for CAPEX, retrofit timing and contract structure. Importantly, while this briefing highlights the strategic implications, the full report contains the segmentation tables, regional and application level breakdowns and downloadable datasets that underpin the numbers — access to those datasets is the most efficient way to adapt the analysis to your company’s unique fleet and supplier exposure.

Closing counsel for 2026

The market trajectory through 2032 is broadly constructive, driven by fleet renewals, urban transit expansion and an accelerating premium on energy-efficient designs. That creates both predictable growth and pockets of disruption. In 2026, corporate leaders should move from passive compliance to active strategy: update specs to enforce futureproof refrigerant and efficiency standards, lock in material and manufacturing resilience, and partner selectively with suppliers that can demonstrate both technology leadership and validation proof-points. For teams seeking executable next steps — from procurement scoring templates to sensitivity runs against copper and refrigerant timelines — our full Worldwide Rail Air Conditioning Market report supplies the underlying models and datasets that will materially reduce uncertainty and shorten decision cycles.

To obtain the full dataset, segmentation tables and supplier scorecards referenced in this briefing, visit the PW Consulting report portal for Worldwide Rail Air Conditioning Market (Base year 2025, Forecast 2026–2032).

For detailed analysis of this topic, please visit the official page:Worldwide Rail Air Conditioning Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com