U.S. Leather Luggage and Goods Industry Analysis: Consumer Demand, Key Players, and Competitive Landscape

Other |

2026-06-08 09:19:04

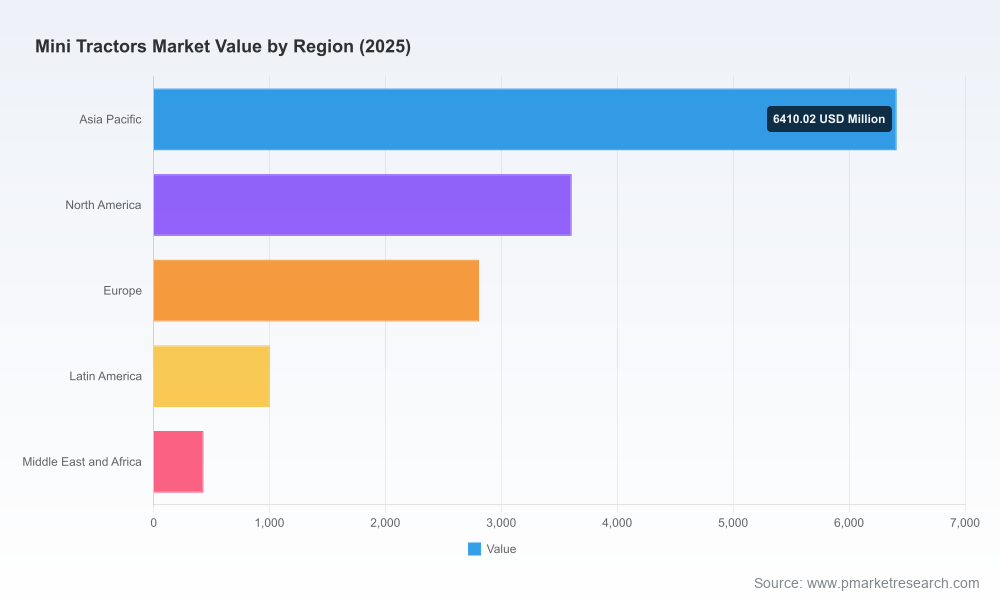

As agricultural mechanization accelerates on smallholdings, peri-urban farms and specialty applications, the mini/compact tractor sector is entering a critical inflection point. PW Consulting’s latest Worldwide Mini Tractors Market report (base year 2025, forecast 2026–2032) synthesizes quantitative forecasting with transaction-ready strategic guidance designed to shape boardroom decisions in 2026. The market reached roughly USD 14.3 billion in 2025 and is modeled to expand at a 5.5% compound annual growth rate through 2032, reaching just over USD 20.7 billion under the central case. While headline growth is constructive, the near-term trajectory includes pockets of stabilization before acceleration — a nuance that should drive cautious, opportunity-focused planning for next year.

Worldwide Mini Tractors Market

Timing: 2026 is the year many OEMs and suppliers will convert strategy into capital allocation — product launches, local assembly investments, and targeted M&A — and they need defensible scenarios rather than optimistic projections.

Worldwide Mini Tractors Market

Margin pressure and regulatory compliance: New emissions and component standards are compressing development windows and increasing bill-of-materials costs; companies that pre-position around these constraints will protect margin and time-to-market.

Worldwide Mini Tractors Market

Channel evolution: Financing and subsidy programs remain a decisive variable in smallholder adoption. Firms that align pricing, finance, and distribution models to local policy frameworks will win share faster.

Mechanization push among smallholders and specialty producers. Demand is being driven by productivity needs on small plots, orchards and peri-urban landscaping where mini tractors deliver outsized ROI. For executives, this implies a focus on modular platforms that can be localized for diverse use cases.

Regulatory tightening and engineering complexity. Emissions standards (e.g., EU Stage V) require advanced injection and after-treatment architectures, creating engineering cost inflation. Firms should be evaluating platform-level investments now to amortize clean-engine technology across multiple SKUs.

Raw material and trade volatility. High-strength steel and specialized alloys are key cost levers. Tariff regimes and Section 232/301 effects in major markets increase landed-cost risk. Actions include strategic sourcing, hedging and near-shore assembly options.

Public policy and subsidies. Continued credit schemes and subsidies in large developing markets materially change price elasticity and adoption curves; anticipating subsidy renewals and structuring channel-level finance products will be a competitive differentiator.

Product and service economics. Aftermarket parts, digital precision features and finance packages are the most reliable margin pools. Companies that move beyond hardware to bundled service models will enhance lifetime value.

The sector shows moderate concentration: the top-three incumbents capture roughly two-fifths of market volumes while the top-five approach a majority share. This structure creates a dual strategic opportunity — incumbents can leverage scale to push technology adoption, while nimble challengers can exploit local channels and targeted value propositions.

John Deere (Moline, Illinois) — leverages precision-ag integration across compact lines. For 2026, Deere’s strategic advantage will be systems-level integration (telemetry, guidance) that ties small-tractor productivity to farm-advisory services.

Kubota (Osaka) — remains an innovation and product-execution leader in compact series, as evidenced by recent premium compact launches that emphasize operator ergonomics and lifecycle reliability. Expect Kubota to push operator-focused features and broaden dealer service contracts.

Mahindra & Mahindra (Mumbai) — strong in price-sensitive segments and emerging markets. Mahindra’s playbook for 2026 centers on affordable local manufacturing, aggressive financing products and last-mile distribution in high-volume rural corridors.

South Korean OEMs (TYM, LS Tractor, Kioti/Daedong) — combine value-driven performance with competitive OEM partnerships. Their agility in platform supply and OEM agreements positions them to win segment share where cost-performance balance matters most.

Yanmar, CNH/New Holland, AGCO/Massey Ferguson — each is adapting legacy strengths (diesel efficiency, global manufacturing footprint, dealer networks) to compact applications. Recent product debuts and region-specific launches signal an intensified product-refresh cycle through 2026.

Smaller specialists (e.g., VST Tillers Tractors) — local market knowledge and targeted product introductions are enabling disruption in specific country markets; expect continued micro-consolidation and OEM licensing activity.

Recent product movements — Kubota’s Grand L70 unveiling, VST’s FENTM compact launch, Massey Ferguson’s MF 5M series debut and LS Mtron’s MT2 introductions — collectively indicate an industry pivot toward operator comfort, efficiency and variant proliferation. These launches are strategic signals: feature parity is narrowing, and differentiation is migrating to services, finance and supply chain economics.

Robust market-sizing and scenario modeling: base, upside and downside forecasts with sensitivity to subsidy continuity, steel pricing and tariff paths — enabling CFOs to stress-test investment cases.

Financial and margin playbooks: component cost curves, assembly economics, and aftermarket revenue models to quantify ROI by strategic option (local assembly vs. centralized manufacturing; SKU rationalization vs. breadth strategy).

Competitive benchmarking and strategic positioning: vendor profiles, capability matrices and go-to-market templates that accelerate due diligence for partnerships and M&A targets.

Channel and financing blueprints: structured dealer economics, captive finance design, and subsidy-aligned pricing templates proven in comparable markets.

Regulatory and technology roadmaps: an emissions-compliance timeline and recommended R&D prioritization for engine, transmission and after-treatment investments.

Supply-chain risk matrix: tariff scenarios, raw material exposure heatmaps and recommended mitigation playbooks (near-shore sourcing, dual-supplier strategies, contract hedges).

Investment and M&A opportunity list: prioritized targets and rationale that map to capability gaps (digital, local assembly, dealer reach, low-cost manufacturing).

Prioritize modular platforms that decouple emissions systems from core chassis and drivetrains — this reduces rework cost across regional variants and accelerates compliance rollout.

Implement a two-track market-entry playbook: (a) scale presence in subsidy-driven, high-volume markets via localized assembly and captive finance; (b) in mature markets, monetize digital services and premium feature packages to protect ASP.

Lock supply via strategic alloy contracts and two-tier sourcing for critical components. Use option contracts to dampen short-cycle price shocks for high-strength steel inputs.

Repurpose dealer networks into service hubs with KPIs tied to aftermarket attach rates. After-sales is the most defensible margin lever in mini-tractor economics.

Accelerate small-scale electrification pilots in controlled use-cases (landscaping, municipal fleets) to capture first-mover service and charging economics without heavy capital outlays.

Evaluate inorganic options strategically: buy to gain distribution and spare-parts density; partner or license to enter price-sensitive segments quickly.

Our report is built to be immediately operational for executive teams who must make 2026 commitments. We combine primary interviews, granular dealer-level economics, engineering cost inputs and policy scenario mapping to produce a playbook that is both defensible and implementable. The executive toolkit included with the report features board-ready slides, transaction checklists, and an interactive scenario model so teams can re-run assumptions against their own cost bases.

For leadership teams preparing 2026 budgets and strategic plans, the essential actions are clear: reassess platform investment timelines, harden supply-chain contingencies, and align go-to-market models to local policy environments. PW Consulting’s Worldwide Mini Tractors Market report provides the empirical foundations and executable templates to convert those actions into measurable outcomes. Access to the full dataset, regional breakdowns and vendor-level financials is available in the comprehensive report — contact PW Consulting or visit our report page to obtain full access and the accompanying strategy pack.

For detailed analysis of this topic, please visit the official page:Worldwide Mini Tractors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com