Worldwide Anti-blue Ray Myopia Lenses Market — Strategic Outlook for 2026 Decision‑Makers

Executive snapshot

PW Consulting’s new market study provides a focused, decision‑ready perspective on the worldwide anti‑blue ray myopia lenses market with base year 2025 and a forecast period spanning 2026–2032. The global market has grown from USD 2,896.6 Million in 2020 to USD 4,285.5 Million in 2025 and is projected to reach approximately USD 7,416.3 Million by 2032. The implied compound annual growth rate (CAGR) for the forecast period is 8.15% — a pace that demands strategic clarity from manufacturers, optical retail chains, clinical networks and investors as they set priorities for 2026.

Worldwide Anti-blue Ray Myopia Lenses Market

Market structure is neither atomized nor monopolistic: concentration metrics indicate a mid‑to‑high consolidation among incumbent leaders, with top‑three and top‑five groups controlling meaningful shares of global revenue. That structure, combined with rapidly evolving technology and regulatory validation, creates windows for both scale players and well‑positioned challengers to accelerate growth.

Worldwide Anti-blue Ray Myopia Lenses Market

Why this report matters to 2026 strategies

- Translate growth into profitable share: With a high single‑digit CAGR, growth alone won’t guarantee margins — this study isolates where premiumization, coating technologies and clinical evidence convert volume into value.

- De‑risk regulatory pathways: The regulatory landscape is shifting from permissive to evidence‑driven. Our report maps jurisdictional requirements and the operational changes needed to commercialize clinically oriented spectacle lenses.

- Align R&D to commercial levers: Technology choices (substrate absorption vs. coating systems; high‑index resins) have distinct tradeoffs in cost, yield and customer experience. We show the tradeoff curves for 2026 planning cycles.

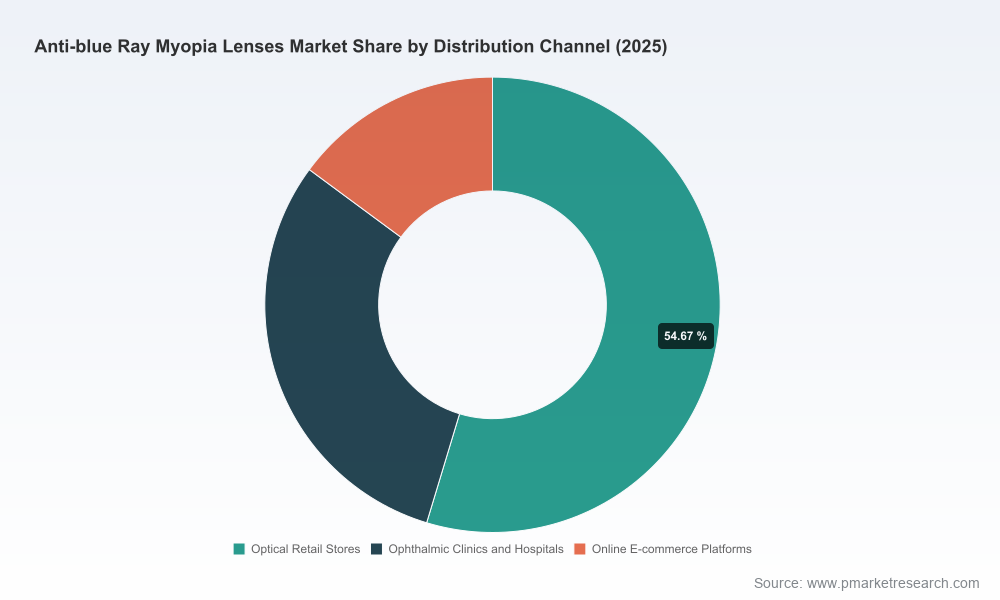

- Prioritize channel investments: E‑commerce, optical retail and clinical channels demand different commercialization playbooks; understanding where to invest marketing and inventory dollars is critical for 2026 rollout plans.

Report content — practical, operational, and executable

This study was designed as an executive‑to‑operator toolkit. Highlights include:

Worldwide Anti-blue Ray Myopia Lenses Market

- Robust market sizing and trend analysis (2020–2025 historical series + 2026–2032 forecast) with scenario variants for conservative, base and accelerated adoption.

- Demand‑driver taxonomy linking epidemiology, screen‑time behaviours and pediatric care protocols to near‑term purchasing patterns.

- Technology and material decision framework — including substrate absorption approaches (e.g., UV420) and coating architectures on modern high‑index resins — that quantifies optical performance, manufacturing yield and margin sensitivity.

- Competitive heatmaps and product positioning profiles for the leading global and regional suppliers, emphasizing regulatory status, clinical evidence and distribution strength.

- Go‑to‑market playbooks for three archetypal commercial models: premium clinic‑led, mass optical retail and direct‑to‑consumer e‑commerce, with key performance indicators and sample promotional funnels.

- Operational playbooks covering procurement, capacity planning, quality controls and backward integration options for lens substrates and coatings.

- Interactive financial models and scorecards for pricing, pack architecture (lens + coating + add‑ons), and channel economics.

Detailed segment tables, proprietary price ladders and downloadable Excel models are available in the full report (summary data retained here to preserve the “trailer” effect for strategic engagement).

Competitive landscape — core players and tactical moves to monitor

The field is defined by a mix of global incumbents with deep clinical programs and regional manufacturers competing on cost, supply flexibility and integrated feature sets.

- EssilorLuxottica (Essilor) — With Stellest and H.A.L.T. technology, Essilor has moved beyond product claims to regulatory validation: September 2025 FDA marketing authorization positioned Stellest as the first spectacle lens authorized to slow pediatric myopia progression. Continued product line investment (Stellest 2.0 with H.A.L.T. MAX) signals an offensive play to combine clinical labeling with premium optical features and anti‑blue options.

- HOYA Vision Care — HOYA’s MiYOSMART family, built around DIMS principles, has increased durability and user experience through recent coating upgrades (Smooth Touch Xtreme). HOYA’s playbook pairs clinically endorsed optics with manufacturing scale and coating IP to protect blue‑light filtering claims while improving real‑world serviceability.

- ZEISS — ZEISS leverages refractive design expertise through its MyoCare range, integrating advanced peripheral optics and blue‑light protection into comprehensive clinical programs and clinician education — an approach that strengthens channel trust among eye‑care professionals.

- Regional manufacturers and specialist suppliers — Several Asian producers have scaled product breadth across indices, photochromic and infrared cut options, and offer competitive price points for clinics and mass channels. These players are closing the gap on quality while using integrated supply chains and certification (CE / ISO) to enter export markets rapidly.

- Lens specialists and optics OEMs — Established optical OEMs and independents (including major camera/optical brands and niche lens specialists) are integrating blue‑light filtration into broader prescription portfolios, creating cross‑category competition based on brand trust and distribution relationships.

Industry dynamics shaping 2026 decisions

- Regulatory validation as a competitive moat: The FDA’s landmark authorization has changed the playing field — clinical data is now a commercial asset. Companies with rigorously documented outcomes will command price premia and clinician preference.

- Consumer behaviour and value perception: Continued increases in screen time among children and adolescents amplify demand for combined solutions that address progression and digital comfort. Buyers increasingly expect multi‑feature lenses rather than single‑attribute products.

- Material & technology convergence: Substrate absorption techniques (e.g., UV420) and durable coating systems are converging; the practical question for R&D is balancing optical clarity, long‑term durability and cost to serve.

- Channel bifurcation: Clinical channels prioritize evidence and service, optical retail leans on convenience and fit, and e‑commerce competes on speed and price. Hybrid models that coordinate clinic verification with digital fulfillment are emerging as the fastest route to scale.

Functional strategic implications — what to do in 2026

- R&D / Product: Prioritize portfolio modularity: a core myopia‑control optic plus a tiered set of blue‑light solutions (substrate, coating, hybrid). Allocate a portion of R&D to real‑world evidence capture to support claims and reimbursement discussions.

- Commercial: Reframe value communication from “blue light only” to combined outcomes (progression slowing + digital comfort). Invest in clinician education, patient adherence tools and aftercare bundles to extend lifetime value.

- Regulatory & clinical affairs: Prepare simplified registrational dossiers and post‑market surveillance plans. Regulatory wins translate quickly into retail and clinical adoption; plan coordinated launch campaigns across jurisdictions where approvals exist.

- Operations & supply chain: Secure multi‑tier suppliers for high‑index substrates and coating chemistries; real options for capacity expansion will be critical during adoption surges.

- M&A & partnerships: Look for complementary targets that provide clinical data assets, coating IP, or distribution access in under‑penetrated markets rather than trophy brands alone.

Scenarios and leading indicators

We recommend monitoring a compact set of leading indicators on a monthly cadence to inform course corrections:

- Regulatory approvals and published clinical readouts

- Clinical adoption rates and sell‑through in pediatric segments

- Channel conversion metrics (clinic‑to‑purchase, online cart conversion, return rates)

- Coating performance feedback and warranty claims

- Input cost indices for resin and coating chemistries and manufacturer capacity utilization

These signals distinguish transient marketing noise from durable shifts in adoption; the full report provides threshold values and alerting logic that can be operationalized within a 2026 war‑room.

How PW Consulting can support your 2026 plan

We work with senior teams to convert this market insight into executable plans: bespoke market models, competitor due diligence, regulatory submission roadmaps, channel go‑to‑market blueprints and acquisition target screens. Clients receive interactive financial templates, scenario dashboards and a prioritized implementation calendar tailored to their strategic ambitions.

This briefing is deliberately a preview: the full study contains the granular segmentation, price ladders, channel economics and downloadable models that decision‑makers need to finalize budgets and product roadmaps for 2026. To access the complete report and the interactive toolset, contact PW Consulting or visit our report landing page for licence options and executive briefings.

For detailed analysis of this topic, please visit the official page:Worldwide Anti-blue Ray Myopia Lenses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com