Worldwide Gas and Liquid Argon Market — Strategic Outlook for 2026 Decision‑Makers

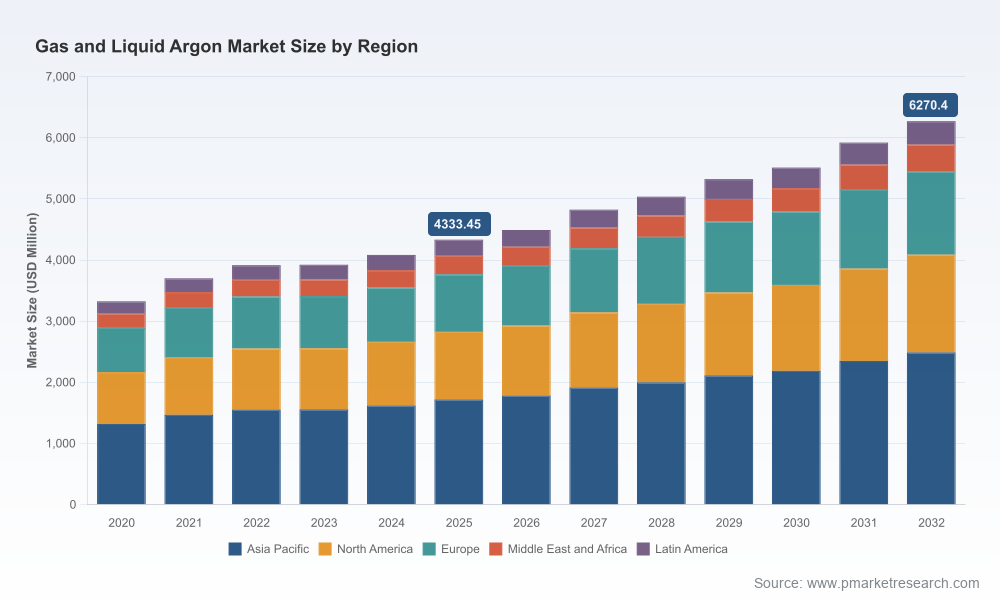

PW Consulting’s latest market intelligence release, Worldwide Gas and Liquid Argon Market (base year 2025, forecast 2026–2032), is built for executives who must convert market signals into immediate strategic action. Drawing on an expanded live dataset and scenario modelling, the report quantifies the argon value chain’s direction while delivering practical tools for procurement, capacity planning, and M&A positioning. At a high level, the market is projected to grow from a 2025 base of USD 4,333.45 Million to USD 6,270.40 Million by 2032, equivalent to a compound annual growth rate (CAGR) of 5.42% across the forecast window. This briefing highlights the report’s strategic value for decisions to be taken in 2026, while reserving the granular segment tables, regional splits and supplier scorecards for the full report.

Worldwide Gas and Liquid Argon Market

Macro trajectory and what it means for 2026

Between 2020 and 2025 the worldwide argon market expanded from USD 3,324.50 Million to USD 4,333.45 Million, a period marked by recovery from pandemic disruptions, renewed industrial investment, and the early effects of semiconductor-capacity expansion. Our forecast through 2032 projects continued, steady expansion to USD 6,270.40 Million led by industrial manufacturing, semiconductors, and energy transition applications.

Worldwide Gas and Liquid Argon Market

For 2026‑era decision-makers this trajectory implies three immediate imperatives:

Worldwide Gas and Liquid Argon Market

- Secure supply elasticity now: anticipated mid‑single-digit CAGR growth compounds demand pressures for bulk liquid and ultra‑high‑purity grades — an acute issue where production is constrained by ASU capacity.

- Recalibrate energy exposure: argon production remains electricity‑intensive; the air separation process accounts for the lion’s share of production cost. Our modelling indicates electricity accounts for approximately 70–80% of production cost, so energy price volatility can materially change delivered cost curves.

- Embed regulatory and logistics contingencies: new transport and refrigerant rules in major markets are reshaping cryogenic logistics and cost-to-serve models, and trade instruments remain a practical source of supply disruption risk.

Practical, decision‑ready contents of the report

We structured the report as an operational toolkit for 2026 execution. Highlights include:

- Executive dashboards — consolidated market sizing, growth scenarios, and key KPI trackers built for monthly board reporting.

- Scenario demand modelling — three demand trajectories (baseline, upside driven by electronics, downside driven by industrial slowdown) with embedded sensitivity to energy and capex shocks.

- ASU capacity and utilisation atlas — a mapped view of installed and announced air separation capacity, lead times for new ASUs, and utilisation sensitivity under each scenario.

- Procurement playbook — RFP templates, contractual clauses for cryogenic supply, LNG‑style take-or-pay risk matrices adapted to bulk liquid argon, and a negotiation checklist tailored to energy‑intensive suppliers.

- Supplier scorecards and concentration analysis — commercial and operational profiles for the top suppliers, supplier stability indices, and a CR analysis to inform market power considerations.

- CapEx and M&A filters — a prioritized list of target attributes and valuation overlays for buyers pursuing scale or regional diversification, plus greenfield vs. brownfield economics for ASU projects.

- Regulatory and logistics appendix — heatmaps of regulatory changes (including transport and refrigerant rules) and compliance checklists for cryogenic maritime transport.

Competitive landscape — who matters and why

The argon market is materially concentrated. Our CR3 and CR5 metrics confirm that the largest players control a significant share of market production and distribution (CR3 ≈ 52.45%, CR5 ≈ 68.12%). That concentration creates both risks and opportunities for buyers and investors.

- Linde plc — a global leader with extensive ASU networks and integrated supply chains. Linde’s recent capacity additions in Europe strengthen its liquid argon reach for electronics customers and bolster its ability to offer long‑term supply contracts to OEMs.

- Air Liquide — a major producer with strategic investments in rare‑gas capacity. Its targeted ASU investments aim to protect semiconductor and specialty markets where purity and reliability are premium attributes.

- Air Products — large-scale supply capability and recent ASU commissioning expand North American throughput. Such expansions change local balancing dynamics and can relieve spot tightness, with knock‑on effects on short‑term pricing.

- Messer, Iwatani, Yingde, Gulf Cryo, Norco — regional specialists that combine local market knowledge, transport logistics and flexible distribution models. Their role is pivotal in serving segment niches (metal fabrication, mining, regional electronics clusters) and in serving as acquisition targets for global consolidation plays.

Recent disclosed developments illustrate these dynamics: capacity expansions and ASU startups in multiple regions have already begun to shift supply elasticity. These moves matter for 2026 because announced projects materially change the near‑term balance between contracted and merchant volumes — and therefore the negotiating leverage for large buyers.

Regulatory, cost, and logistics headwinds to watch

- Energy cost exposure — industrial electricity prices have risen in critical markets (for example, US industrial electricity averaged approximately USD 0.072/kWh in late 2023), and energy represents the dominant cost in ASU‑based production. Hedging strategies and local renewable PPAs can materially alter unit economics.

- Transport and refrigerant rules — recent EU regulation restricting high‑GWP refrigerants for cryogenic transport increases compliance costs and creates switching costs in logistics providers’ fleets.

- Trade and tariff risk — tariffs remain a practical lever in North–South supply flows; import duties on industrial gases can raise landed cost and incentivize on‑shore capacity investments.

- Certification and safety compliance — premium‑grade argon destined for semiconductor fabs requires adherence to maritime and cryogenic transport codes (e.g., IGC Code compliance) which increase the technical bar for international suppliers.

Recommended 2026 actions by corporate role

- Procurement leaders: renegotiate long‑term contracts with clauses tied to energy indices, secure optionality via regional second‑sourcing, and deploy a 90‑day spot vs contract rebid cadence.

- Operations and supply planners: model ASU outage scenarios into production scheduling, validate cryogenic logistic partners against new refrigerant rules, and quantify time-to-fill for bulk liquid shortages.

- Strategy and corporate development: prioritize M&A targets that deliver immediate regional fill or premium‑grade capability; use our CapEx overlay to compare greenfield ASU payback against long‑term contract costs.

- Risk and compliance: implement an argon‑specific regulatory watchlist (tariffs, transport codes, refrigerant rules) and stress‑test supply chains under those regulatory outcomes.

How to use this report in your 2026 planning cycle

The report is intentionally designed as an operational companion for the 2026 planning calendar. Use it to inform Board and executive-level choices in three discrete workflows:

- Immediate procurement play — deploy the report’s RFP templates and supplier scorecards to rebid 12–18 month contracts in the first half of 2026.

- Short‑term CapEx decision — use the ASU economics module to compare build vs. buy options where tariffs or logistics make local production more attractive.

- M&A screening and integration planning — apply the target filters and post‑deal integration checklist to any strategic acquisition intended to secure premium‑purity supply or shorten delivery chains.

Closing and next steps — the trailer

PW Consulting’s Worldwide Gas and Liquid Argon Market report provides the analytical depth and practical toolset required to convert 2026 market movements into competitive advantage. This briefing has highlighted the strategic takeaways and actionable recommendations while reserving the granular regional and application splits, supplier financials, and proprietary demand tables for the full publication. Those datasets include modelled regional flows, application‑level demand curves, and supplier‑level scorecards that are indispensable when negotiating contracts or evaluating capital commitments.

For access to the full dataset, downloadable dashboards, and a hands‑on 90‑day procurement playbook, please consult the report page on the PW Consulting website or contact your PW Consulting engagement lead. In a market where energy dynamics, regulatory changes and a concentrated supplier base intersect, having the detailed numbers behind the narratives is the difference between a reactive purchase and a strategic supply advantage in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Gas and Liquid Argon Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com