Reels and Spools Market Trends and Growth Analysis

Other |

2026-05-20 07:26:07

As global industry leaders reset priorities for 2026, the industrial cleaning services market has become a strategic hinge between operational continuity, regulatory compliance, and sustainability outcomes. PW Consulting’s latest market study — built on a 2020–2025 historical base and a 2026–2032 forecasting horizon — shows a market that has expanded from the mid‑2020s into a robust multi‑billion dollar opportunity. The market was valued at approximately USD 72.0 billion in 2025 and is forecast to approach USD 104.4 billion by 2032, representing a compound annual growth rate of 5.45% over the forecast period. This release summarizes the strategic takeaways that executives, procurement leaders, and investors must consider in 2026, while preserving the granular segmentation and proprietary scenario outputs for subscribers and report purchasers.

Worldwide Industrial Cleaning Services Market

Operational risk is now commercial risk: cleaning programs are tightly coupled to uptime, product quality, and regulatory certification across heavy industry, food & beverage, pharmaceuticals, and energy.

Worldwide Industrial Cleaning Services Market

Cost pressure meets compliance mandates: wage inflation, chemical price volatility and new safety protocols create a complex cost‑to‑quality tradeoff that cannot be managed through incremental supplier negotiation alone.

Worldwide Industrial Cleaning Services Market

Consolidation and capability shifts are accelerating: the market remains fragmented, and leading global providers are supplementing traditional offerings with digital, sustainable and compliance‑centric services — creating both M&A and partnership opportunities.

The market’s trajectory since 2020 demonstrates resilient demand for outsourced and specialist cleaning services. From a mid‑2020s base of roughly USD 55–72 billion (2020 vs 2025), the sector is projected to grow to an order of magnitude north of USD 100 billion by 2032 under the baseline scenario. The mid‑single digit CAGR (5.45% across the forecast horizon) masks important secular drivers: accelerated spend on hygiene and contamination control in regulated industries, rising maintenance outsourcing in logistics and manufacturing, and invention of higher‑value service lines such as dry‑ice blasting or specialty tank services.

For corporate decision‑makers, the key implication is that growth is not homogeneous. While headline expansion creates topline opportunity, margin pressure from labor and input cost increases means service mix and contract architecture will determine winner‑takes‑most outcomes at the site level.

Labor dynamics: Skilled industrial cleaning labor remains tight. In the US the hourly wage for industrial cleaners averaged around USD 18.50 in 2024, and industry studies project a meaningful shortage of qualified personnel approaching 2026. Wage inflation and recruitment scarcity require firms to reconfigure operating models — from training academies to hybrid human‑automation crews.

Regulatory intensity: Updated standards and chemical handling rules (for example, new EU mandates and revised OSHA protocols) are translating into higher compliance minimums for cleaning agents, process verification, and powered‑equipment procedures. Non‑compliance risks extend beyond fines to production stoppages and customer claim exposure.

Raw material and input price shocks: Supply disruptions in surfactants and specialty chemistries have driven chemical price increases in recent cycles, pressuring both suppliers and end‑users to rethink procurement strategies and substitution plans.

Sustainability and corporate procurement: Major customers now include sustainability clauses and validated emissions or chemical‑use reporting in contracts. Service providers that can prove lower environmental impact and circular chemical programs are winning premium relationships.

The sector is characterized by a mix of global integrated players, regional specialists, and a long tail of local providers. Global firms highlighted in the report — including ABM Industries, Sodexo, Aramark, ISS Facility Services, Compass Group, Dussmann Group, Kuehne+Nagel, GDI Integrated Facility Services, OCS Group, and Atalian Global Services — illustrate three strategic archetypes in the market:

Scale integrators building cross‑service offers: These firms leverage footprint and contract scale to bundle cleaning with broader facility services, logistics, or workplace solutions, enabling negotiated margins on multi‑site, multi‑service deals.

Capability specialists: Organizations that focus on technical cleaning (tank cleaning, dry‑ice blasting, chemical decontamination) command higher ASPs and maintain differentiation through certification and specialized equipment.

Regional champions and service aggregators: Local players bring deep client relationships and responsiveness; they are attractive consolidation targets for buyers looking for granular coverage or bolt‑on capabilities.

Recent competitive moves underscore these dynamics: ABM’s multi‑year manufacturing contract wins, ISS’s automotive partnership to raise cleaning protocols, Sodexo’s launch of sustainable cleaning programs in Asia‑Pacific, and Aramark’s ISO 14001 recertification for North American operations. Collectively these developments point to three active strategies: deepen sector specialization, validate sustainability credentials, and pursue targeted partnerships rather than broad horizontal expansion alone.

This study is purposely designed as a strategy workbench. Subscribers receive traditional market sizing and forecasting plus a suite of pragmatic deliverables tailored to 2026 decision cycles:

Methodology and data appendices that explain assumptions behind sizing and scenarios (including sensitivity to wage and chemical cost shocks).

Competitive profiles and a thematic M&A heatmap identifying high‑value target archetypes (by capability and geography) and integration risk checklists.

Service‑level benchmarking tools and unit‑cost models (labor, consumables, equipment), ready for client‑specific input to produce site‑level margin simulations.

Regulatory compliance matrix and an implementation checklist that maps jurisdictional requirements to operational controls and audit evidence.

Commercial playbooks: outcome‑based contract templates, SLA construction, and tender evaluation scorecards to help procurement teams reframe pricing and risk sharing.

Digital and sustainability adoption roadmaps, including KPIs for chemical reduction, emissions accounting, and digital inspection rollouts.

Redesign workforce and service delivery for resilience: Invest in modular staffing (core certified teams + flexible local crews), create accredited in‑house training pipelines, and pilot automation (robotic scrubbing, remote inspection) on high‑frequency sites to protect margin. Use the report’s unit‑cost model to stress‑test staffing scenarios under wage and shortage assumptions.

Shift commercial models from input pricing to outcome pricing: Where quality and contamination control are mission‑critical, negotiate outcome‑based contracts tied to cleanliness validation metrics and uptime. Incorporate service bundles (cleaning + monitoring + rapid response) to capture more value per site.

Make sustainability a competitive moat: Standardize greener chemistries, deploy circular packaging and dosing systems, and pursue recognized certifications to meet customer procurement thresholds. The report includes a supplier compliance checklist and ESG metric set for commercial use.

C‑suite and strategy teams: Use market scenarios and M&A heatmaps to prioritize geographies and capability bets for 12–36 month horizons.

Procurement and operations: Adopt the tender templates, supplier scorecards and unit‑cost models to renegotiate contracts and pilot new service frames.

Private equity and corporate development: Apply the diligence checklists and consolidation playbook to size roll‑up economics and post‑deal integration risks.

Service providers: Benchmark offerings, test premium pricing for sustainability and technical services, and design training programs to mitigate labor scarcity.

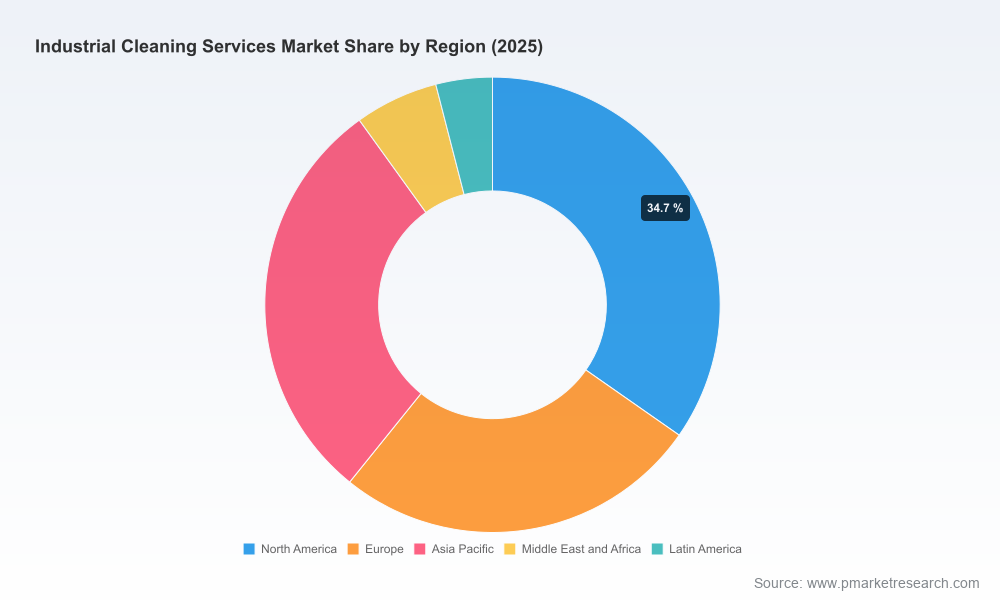

To respect the strategy workbench nature of the study, this briefing highlights the macro trajectory, dynamics and actionable recommendations while withholding granular split tables and proprietary scenario sheets — including detailed regional, service‑type and vertical revenue splits and the full set of downloadable financial models. These elements are core to the report experience and are provided to subscribing clients to enable tailor‑made site, bid and M&A modelling.

For 2026 planning cycles, PW Consulting recommends engaging the full report and its Excel workbooks to run bespoke scenarios against your portfolio of sites and supplier contracts. The report’s models will enable teams to quantify tradeoffs between wage inflation, chemical price risk and automation capex — and to convert those insights into procurement decisions and investment cases.

If your organization is preparing budgets, evaluating target acquisitions, or redesigning supplier contracts in 2026, this study is designed to be immediately operational. Visit the PW Consulting report page to obtain the complete dataset, downloadable models, and supplier checklists that underpin the recommendations summarized here.

For detailed analysis of this topic, please visit the official page:Worldwide Industrial Cleaning Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com