Worldwide Exterior Solar Shading Systems Market — Strategic Briefing for 2026 Decision-Makers

PW Consulting’s latest market research — the Worldwide Exterior Solar Shading Systems Market report (base year 2025) — is designed as a tactical briefing for executive teams preparing strategy, investment, and procurement decisions in 2026. This release synthesizes market-scale metrics, competitive dynamics, material and regulatory shocks, and actionable playbooks that business leaders need to convert growing demand for solar shading into margin-accretive growth. Below we highlight the report’s core strategic takeaways while preserving detailed segment-level forecasts and proprietary model outputs for readers who access the full report.

Worldwide Exterior Solar Shading Systems Market

Macro view: market size, trajectory and what it implies for 2026

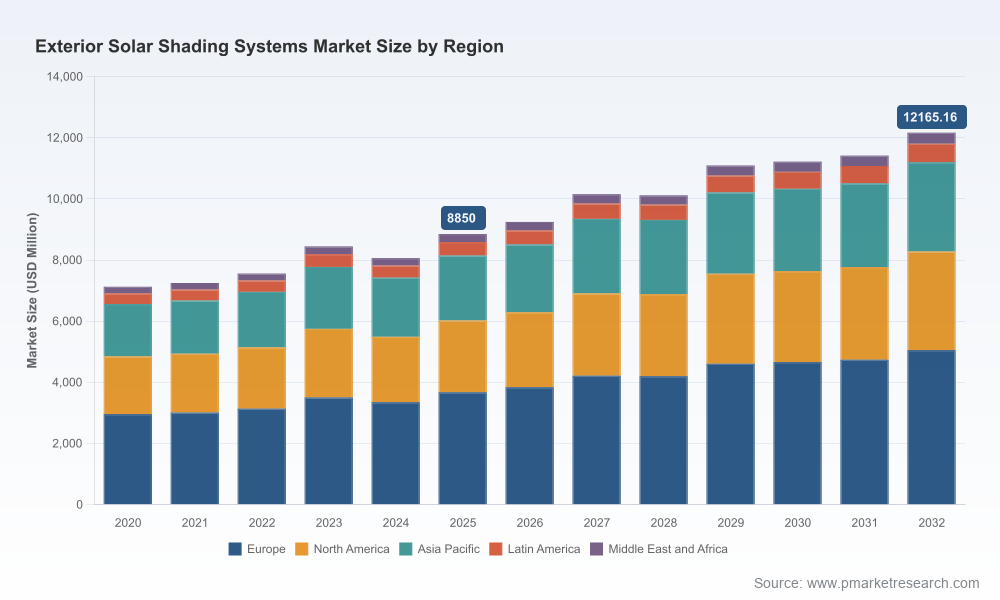

The exterior solar shading market has demonstrated resilient growth through the early 2020s and reached an estimated global revenue base of approximately USD 8.85 billion in 2025. PW Consulting’s forward-looking model projects a compound annual growth rate of 4.65% over the 2026–2032 forecast horizon, reflecting steady expansion driven by retrofit activity, new construction energy regulations, and heightened demand for building electrification and occupant comfort solutions. The market is expected to move into the mid-to-high single digit billions by the end of the forecast period, creating meaningful scale opportunities for manufacturers who can align product performance, digital controls and sustainability credentials.

Worldwide Exterior Solar Shading Systems Market

Why 2026 is a tipping point for corporate strategy

- Regulatory acceleration: National and supra‑national building energy codes are increasingly prescribing external shading as a primary means to control solar heat gain and reduce cooling loads. Examples include updated UK building regulations addressing overheating and energy conservation, and new EU trade and carbon policies that change material sourcing economics.

- Raw-material volatility: Aluminium — a core input for many extruded profiles and louvers — experienced significant price escalation and ongoing supply constraints in recent periods. This dynamic is reshaping cost curves, contracting strategies and total-cost-of-ownership discussions with clients.

- Technology convergence: Advances in motorization, IoT controls, and integrated glazing/shading systems are shifting customer expectations from commodity shading elements to system-level solutions that deliver energy savings, occupant comfort and measurable whole-building performance.

- Commercial opportunity mix: While new build activity remains important, a growing retrofit market driven by stricter energy standards, corporate ESG targets and incentives creates a lower‑risk, faster‑payback revenue stream for providers that can offer modular, low‑disruption solutions.

Competitive landscape — how leading firms are positioning

The market remains fragmented: the largest brand clusters account for a modest share of global revenues, leaving substantial room for regional specialists, systems integrators and adjacent building-products firms to expand. This fragmentation is reflected in relatively low top‑company concentration ratios, reinforcing that scale plus specialized capabilities will determine winners over the next five years.

Worldwide Exterior Solar Shading Systems Market

Key incumbent profiles and strategic implications:

- Hunter Douglas Inc. (Netherlands): A global leader with deep product breadth and design integration capabilities. Their strength is in combining architectural aesthetics with energy performance — a model that competitors should study when targeting premium commercial and high-end residential segments.

- WAREMA Renkhoff SE (Germany): Focuses on high-quality mechanical systems and advanced automation. Their approach highlights the commercial payoff of investing in robust control platforms and service ecosystems.

- Lutron Electronics Co. Inc. (USA): Dominant in integrated controls and smart-building interfaces. Lutron’s playbook is instructive for shading manufacturers pursuing deeper integration with BMS and energy management systems.

- Kawneer (Arconic Corporation) (USA): Brings aluminum architecture and façade expertise; effective vertical integration across façade and shading components strengthens bids for high-performance building envelopes.

- Somfy Systems Inc. (France): Leader in motorization and control modules — an essential partner for OEMs seeking rapid product electrification.

- Regional and specialized players (e.g., Duco, Griesser, Levolux, Renson, Markilux): These firms demonstrate how geographic focus, engineering differentiation and customer service models sustain higher margins where local codes and architectural practices vary.

For manufacturers and investors, two competitive imperatives arise: (1) scale to manage input-price volatility and global clients, and (2) upgrade systems capabilities (motorization, sensors, software) to capture recurring revenue from service and control contracts.

Signals from recent product, M&A and industry activity

- Product innovations — such as synchronized shading ranges, AI‑driven dynamic shades and rollable screens with integrated solar foils — point to a near-term product cycle emphasizing performance, autonomy and energy harvesting.

- M&A activity, patent acquisitions and targeted buyouts of niche technology (e.g., micro‑structure glazing IP) indicate that firms are securing capabilities rather than building them from scratch; owners of core patents will command strategic optionality.

- Trade shows and industry fora scheduled through 2026+ are already serving as launchpads for integrated facade-plus-control concepts; these venues accelerate specification cycles among architects and large corporate building operators.

What PW Consulting’s report delivers to 2026 decision-makers (practical contents)

Our study is organized to support operational decisions from procurement to product development and investor due diligence. Key deliverables include:

- Proprietary market model and revenue forecast (2026–2032) with multiple scenarios to stress-test pricing, aluminium cost and regulation shocks.

- Quantified demand drivers and adoption pathways for new-build versus retrofit markets, with payback matrices and sensitivity analyses for typical building archetypes.

- Supply‑chain risk map and mitigation playbook: supplier concentration, nearshoring options, alloy substitution levers and hedging strategies.

- Competitive benchmarking and vendor scorecards evaluating product breadth, control-platform maturity, geographic reach and service economics.

- Technology roadmap with timelines for motorization, IoT interoperability, sensor-driven automation and integrated solar-harvesting shading systems.

- Regulatory mapping and compliance checklists for key markets, showing where product specifications must change to remain eligible for incentives and certifications.

- Commercial rollout toolkit — go‑to‑market playbooks for OEMs, installers and distributors (pricing, channel incentives, retrofit installation protocols).

- Investment case templates and ROI calculators to support M&A or capex decisions under varying aluminium-price and carbon‑policy scenarios.

These elements are purpose-built to convert market intelligence into executable sprints in 90–180 day cycles.

Recommended 2026 priorities — six strategic moves with immediate impact

- Hedge raw-material exposure and localize high-risk extrusions: Given recent aluminium price escalation and LME volatility, firms should combine purchasing hedges with targeted regional extrusion capacity to stabilize lead times and protect margin.

- Monetize controls and services: Convert one‑time hardware sales into recurring revenue via subscription models for controls, remote diagnostics and performance guarantees. Integration partnerships with leading controls companies reduce time-to-market.

- Productize retrofit simplicity: Develop modular kits and fast-installation protocols for existing façades to capture the growing retrofit share, which often features rapid payback for end-clients and lower procurement friction.

- Embed sustainability into the value proposition: Certify recycled-aluminium content, disclose lifecycle carbon and align product labeling to regional carbon mechanisms; this reduces procurement friction for large institutional customers and improves tender outcomes.

- Prioritize strategic alliances and micro‑M&A: Acquire IP for differentiated glazing or micro‑structure technologies, or partner with motor/control specialists to accelerate system capability without large internal R&D investments.

- Operationalize scenario planning: Run commercial and procurement scenarios that explicitly include carbon border adjustments, material-cost shocks and accelerated regulation — use them to size buffer inventories and conditional capacity ramp plans.

How to apply the report across organizational functions

Our report is structured to be directly operational for:

- Product and R&D leaders: Use the technology roadmap and patent landscape to prioritize feature sets and partnerships.

- Commercial and BD teams: Deploy the buyer personas, payback calculators and retrofit playbooks to shorten sales cycles and increase close rates.

- Procurement and supply-chain teams: Implement the risk map and hedging strategies to reduce margin erosion and ensure fabricational continuity.

- CFOs and corporate development: Leverage scenario-based valuations and vendor scorecards to inform M&A and capex prioritization.

- Sustainability and compliance teams: Apply the regulatory mapping to ensure product compliance and to qualify for energy-efficiency incentives and green procurement lists.

Next steps — where this briefing leaves you and how to get the full playbook

This briefing surfaces the strategic inflection points that will shape winners and laggards in the exterior solar shading market during 2026 and beyond. For teams that need the full segmentation matrices, granular regional and application forecasts, vendor-level financial proxies, and downloadable scenario models, PW Consulting’s full report includes a complete data package and an advisory workshop option to translate findings into a 100-day execution plan.

We recommend scheduling a tailored briefing with the PW Consulting strategy team to run a live scenario session against your product roadmap or procurement pipeline. The full report will provide the detailed slices and sensitive segmentation datapoints that inform precise commercial and operational moves — data we intentionally reserve for the complete publication to protect model integrity and ensure clients receive the actionable artifacts required for immediate deployment.

PW Consulting remains available to support strategic planning, procurement redesign, M&A diligence, and product commercialization for companies seeking to capitalize on the market’s structural growth while managing the material, regulatory and technological headwinds that will define 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Exterior Solar Shading Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com